| Years | Rebalancing | Metrics | Matrices | MinVar | Right-tail weighted | Hurst exponent weighted | Right-tail-Hurst weighted |

|---|---|---|---|---|---|---|---|

| 2 | No rebalancing | Log-return pdfs, fractal dimensions, tail risks, CVaR |

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

| 2 | Rebalanced quarterly | Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

||

| 5 | No rebalancing | Log-return pdfs, fractal dimensions, tail risks, CVaR |

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

| 5 | Rebalanced quarterly | Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

||

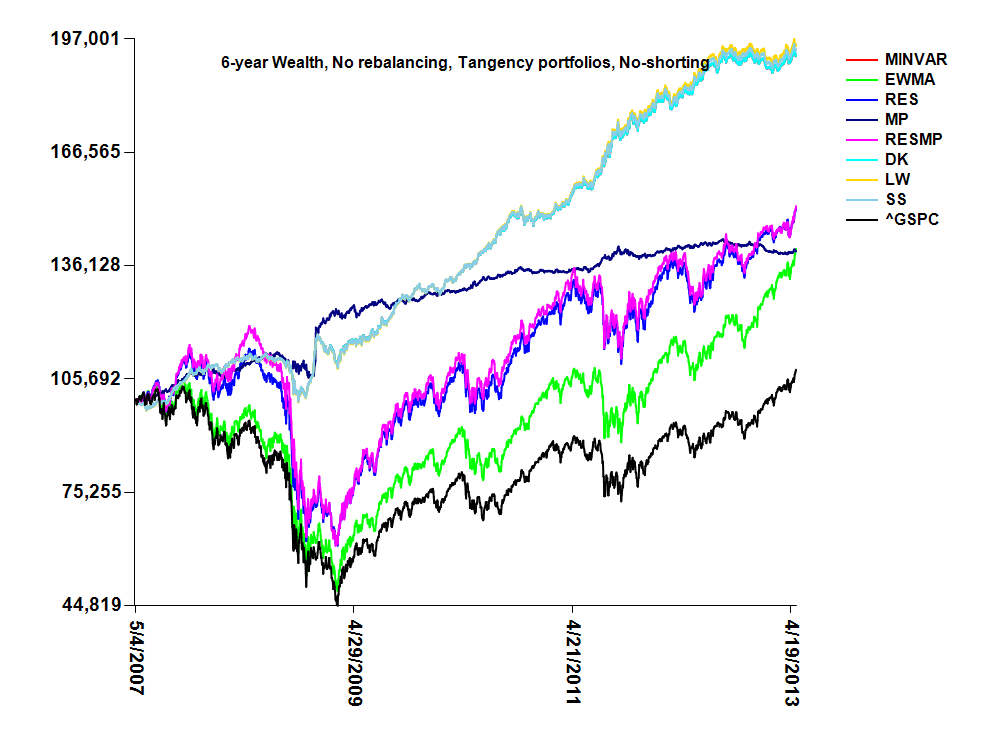

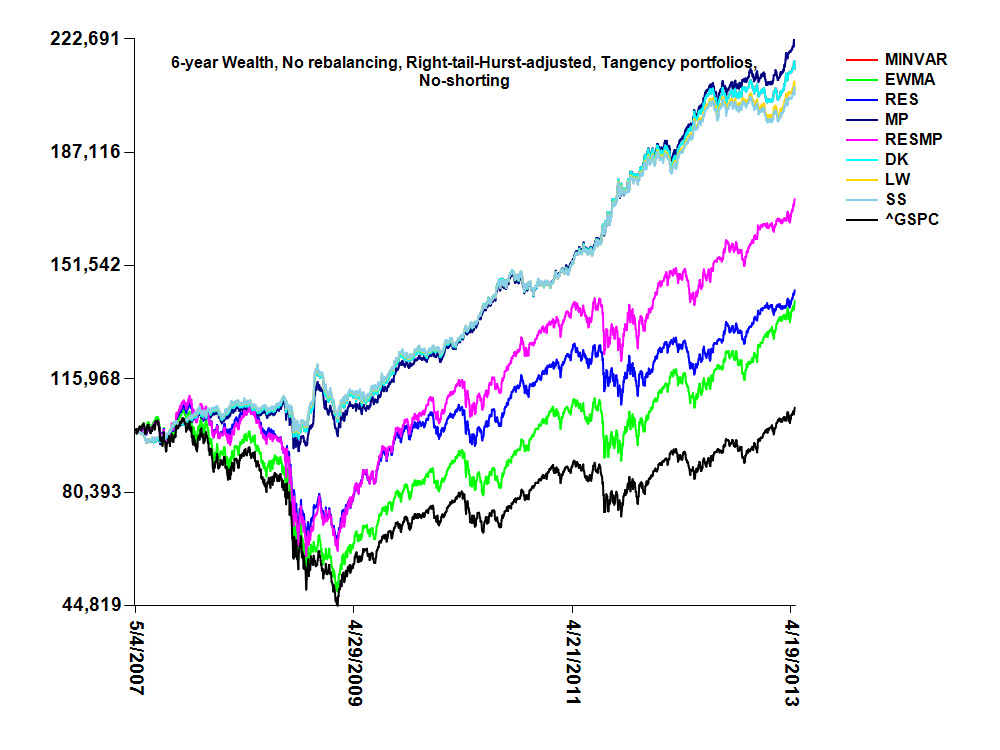

| 6 | No rebalancing | Log-return pdfs, fractal dimensions, tail risks, CVaR |

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

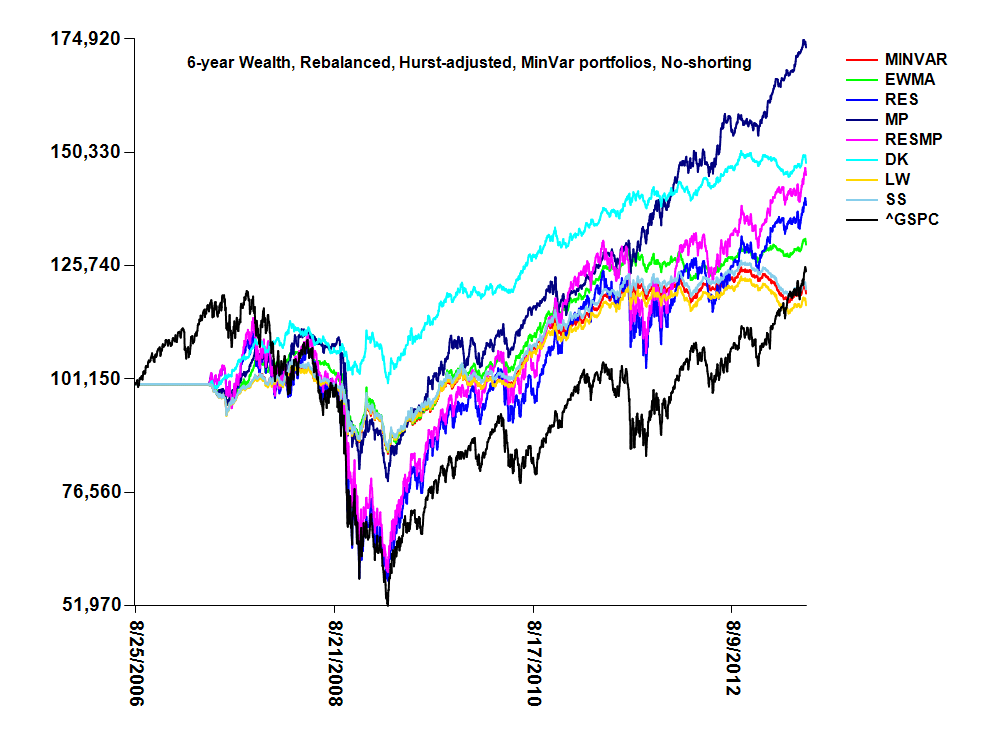

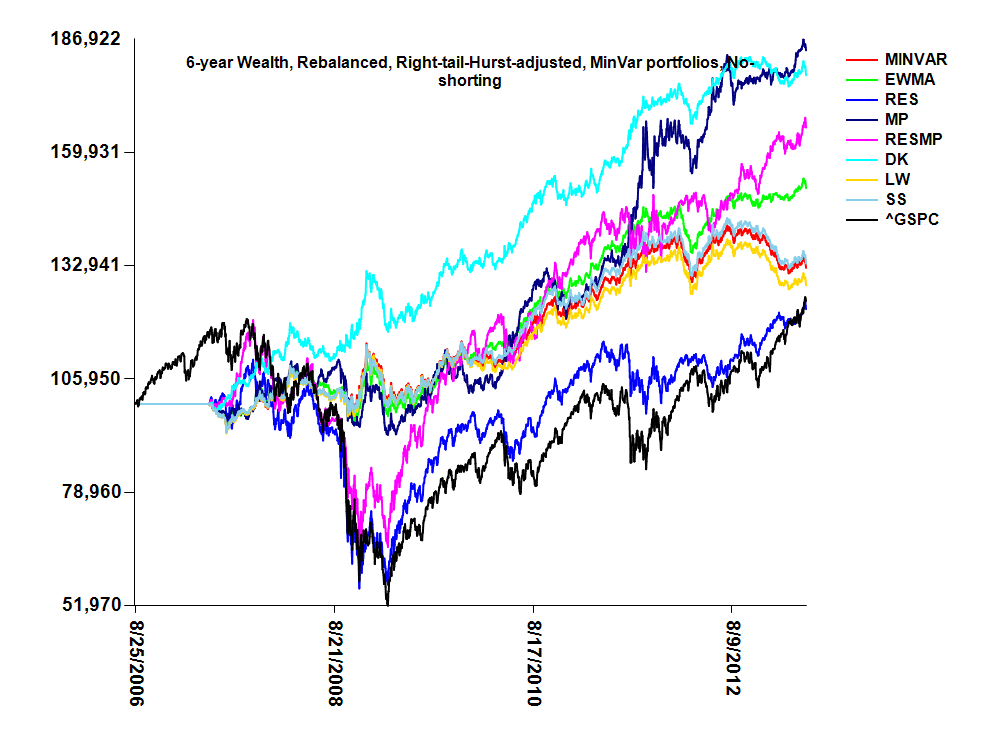

| 6 | Rebalanced quarterly | Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

Returns,

Weights,

|

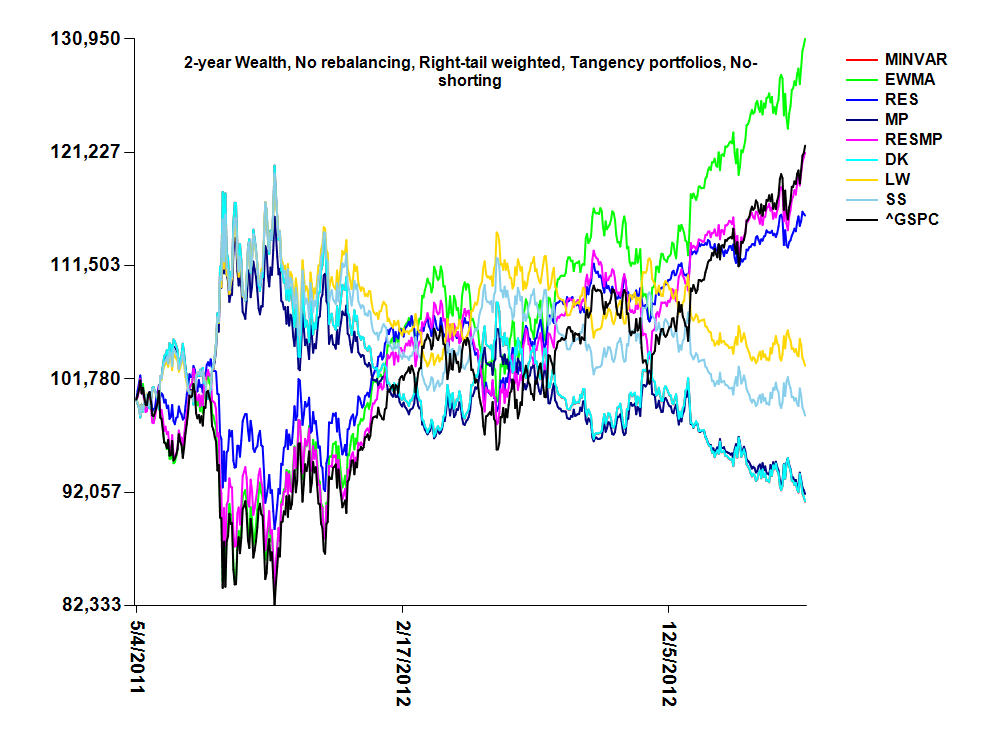

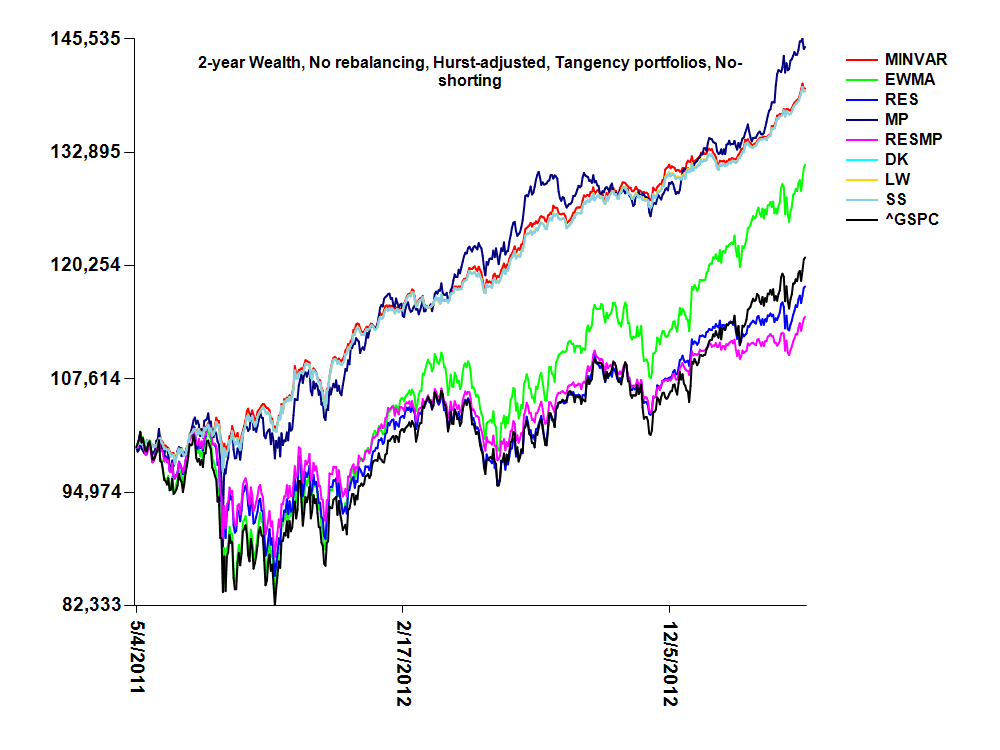

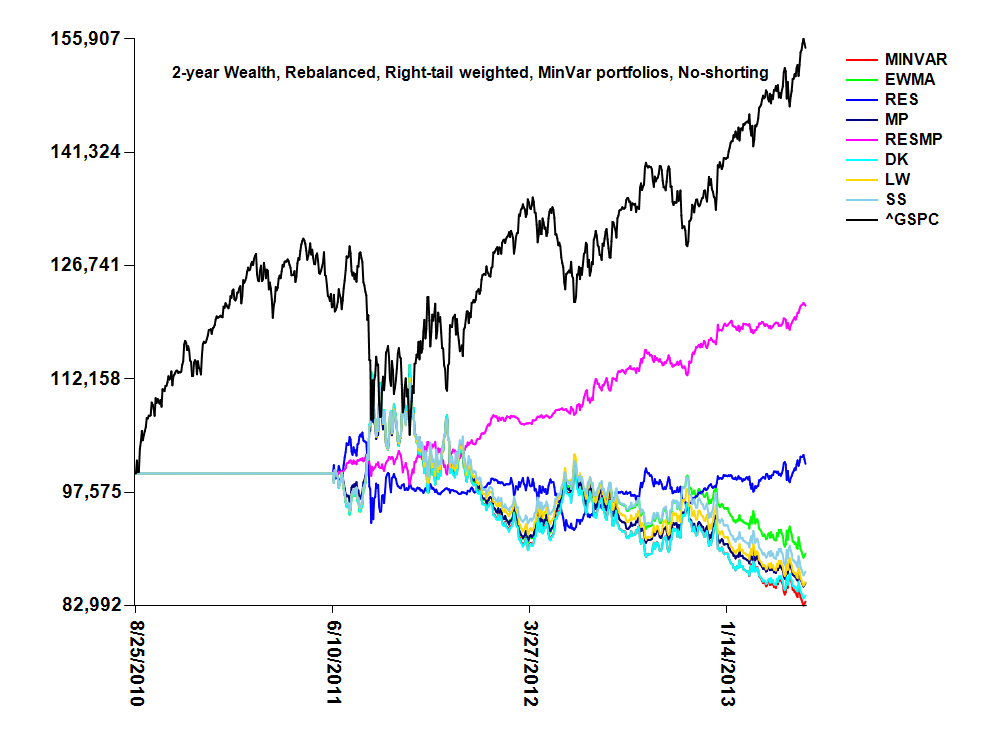

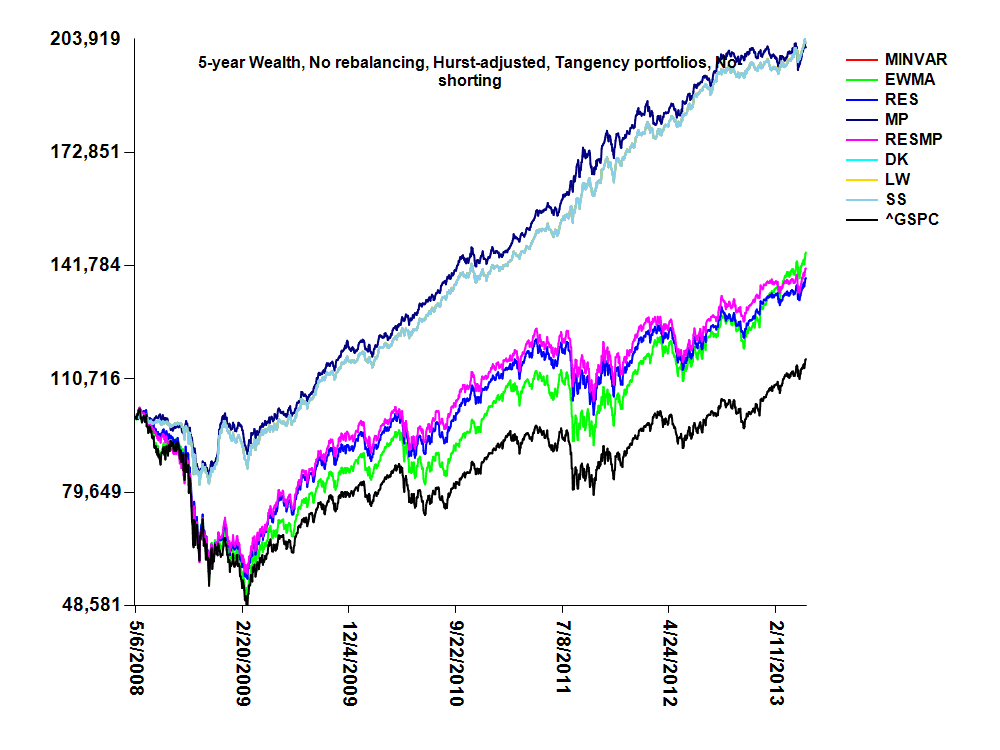

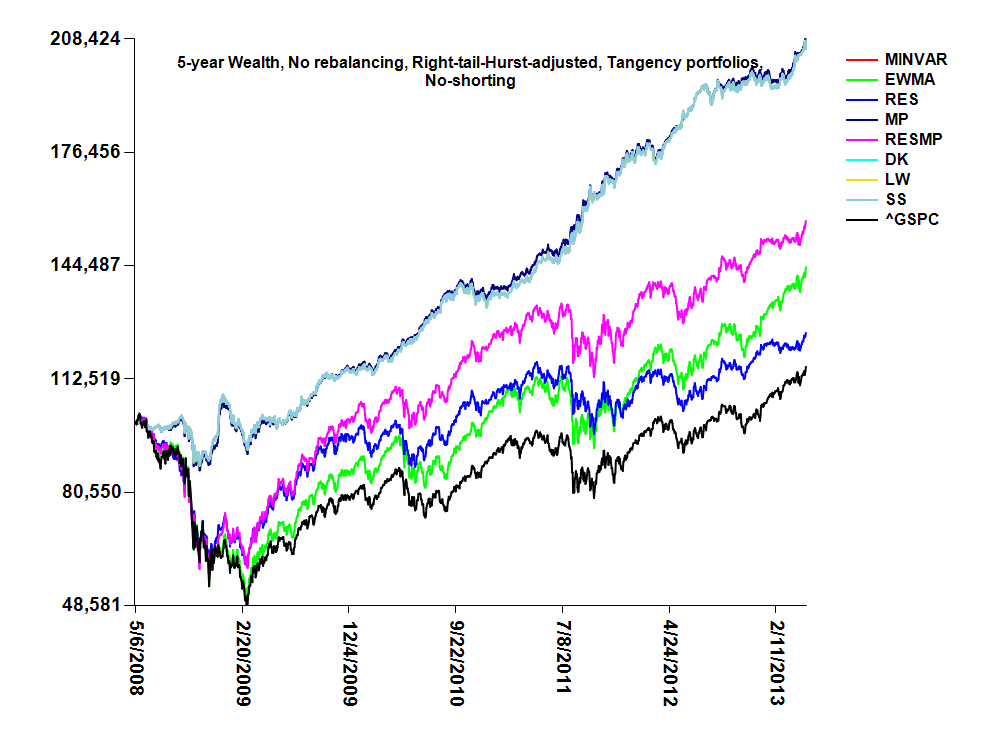

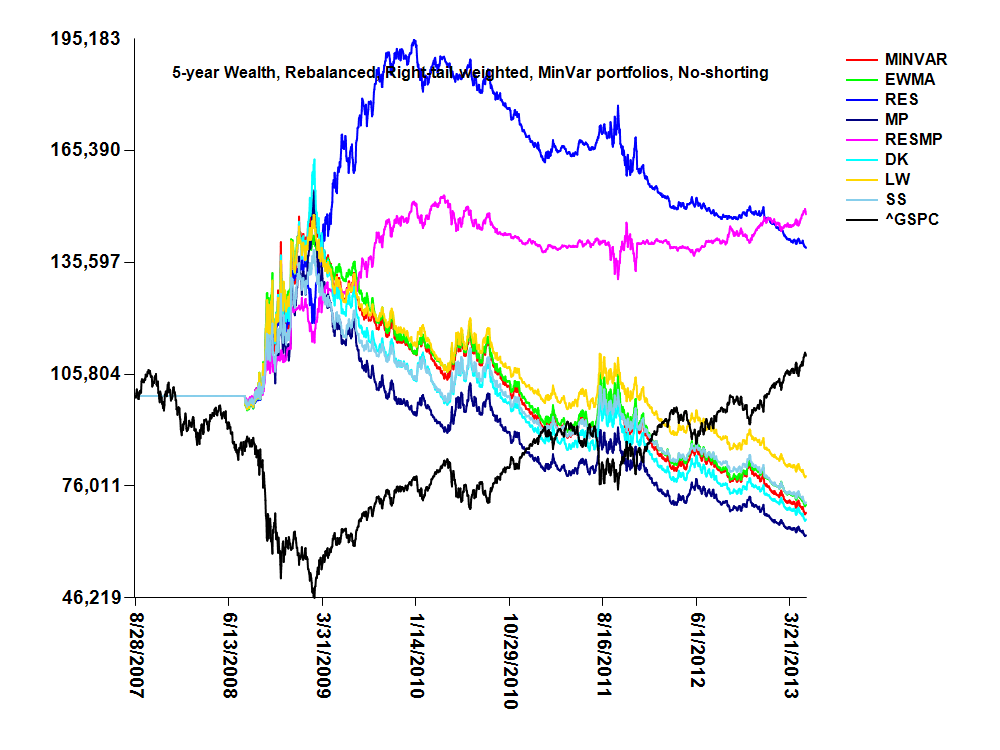

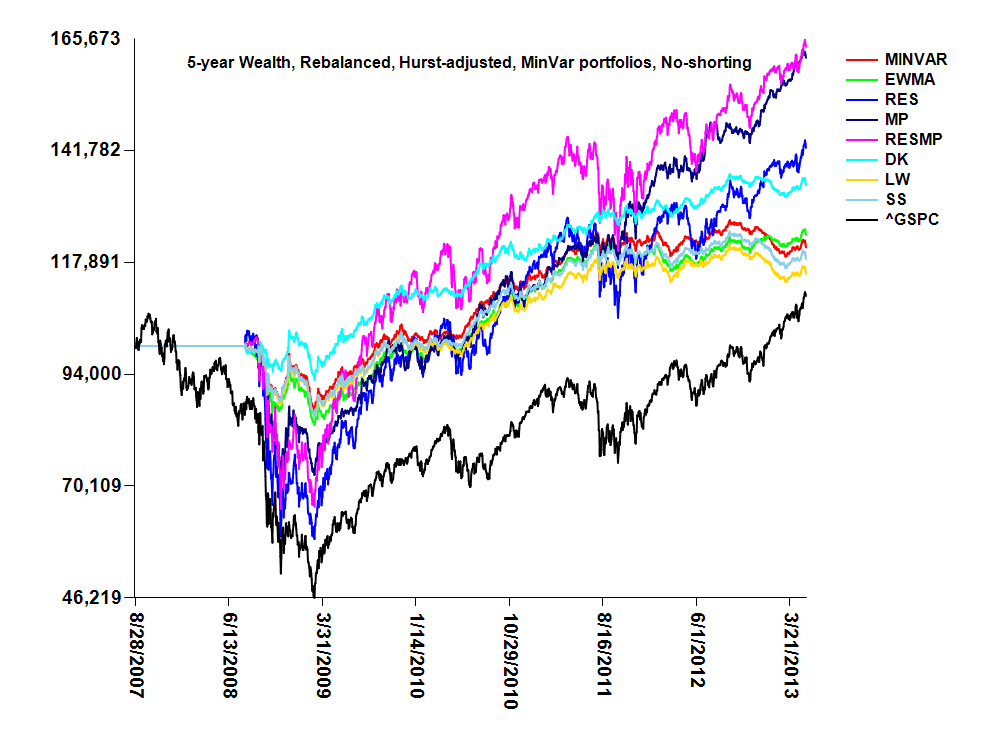

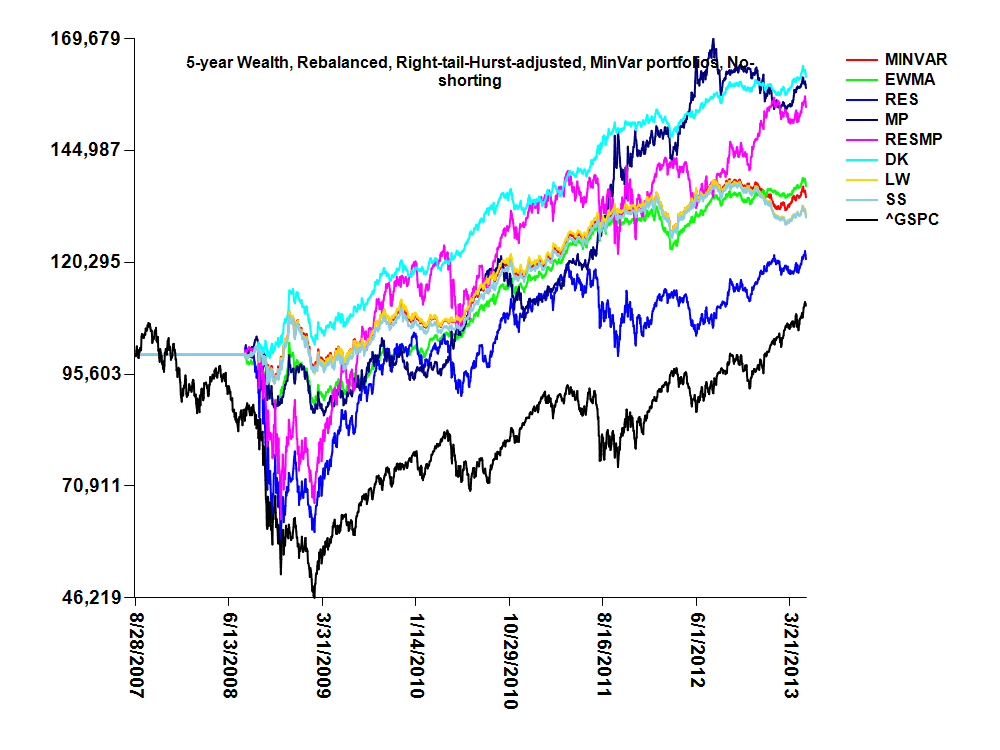

-MinVar - Minimum variance portofolio, tangency is used for unbalanced, whereas minimum variance is use for rebalanced portfolios.

-EWMA - Exponential weighted moving average determination of returns and standard deviation.

-RES - Component subtraction used to remove effect of the first principal component of the correlation matrix on returns.

-MP - Component subtraction used to remove effect of noise eigenvectors (below Marcenko-Pastur cutoff, lambda+), on returns.

-RESMP - Component subtraction employed to remove effects of greatest principal component and noise eigenvectors below MP cutoff.

-DK - Daniels-Kass shrinkage of correlation matrix.

-LW - Ledoit-Wolf shrinkage of correlation matrix.

-SS - Schafer-Strimmer shrinkage of correlation matrix.

-^GSPC - S&P 500 index.

-Dividends applied to all portfolios.

© 2019 NXG Logic, LLC