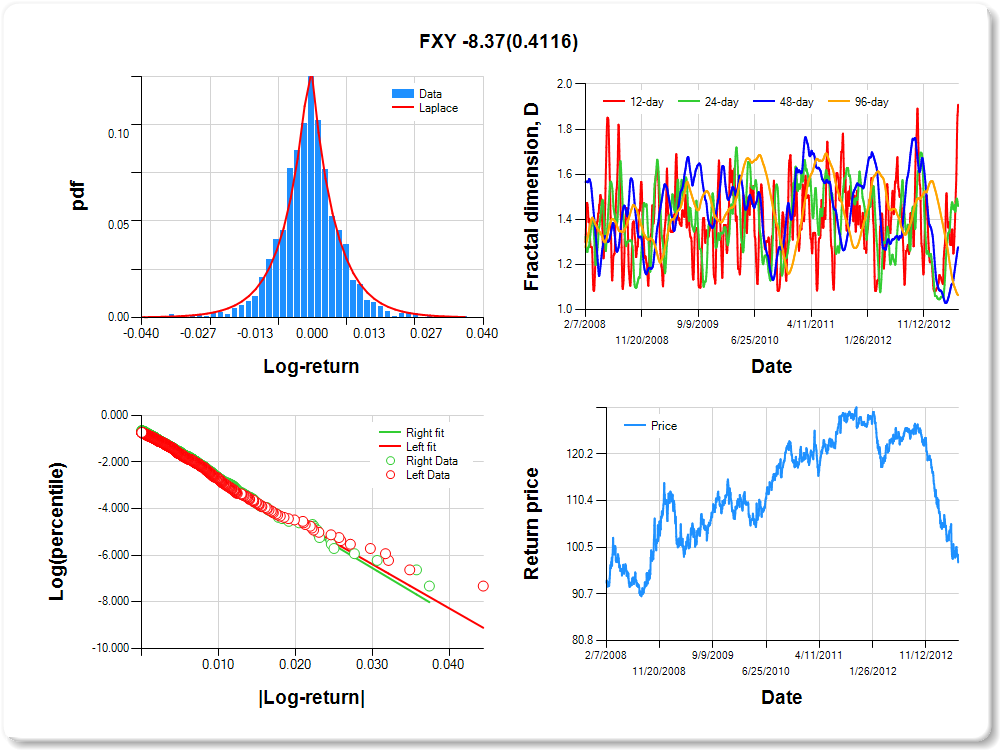

FXY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

2.12 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.156 |

0.239 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.716 |

0.054 |

-13.316 |

0.0000 |

|log-return| |

-188.644 |

7.204 |

-26.187 |

0.0000 |

I(right-tail) |

0.089 |

0.075 |

1.193 |

0.2329 |

|log-return|*I(right-tail) |

-8.375 |

10.197 |

-0.821 |

0.4116 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.091 |

0.541 |

0.723 |

0.936 |

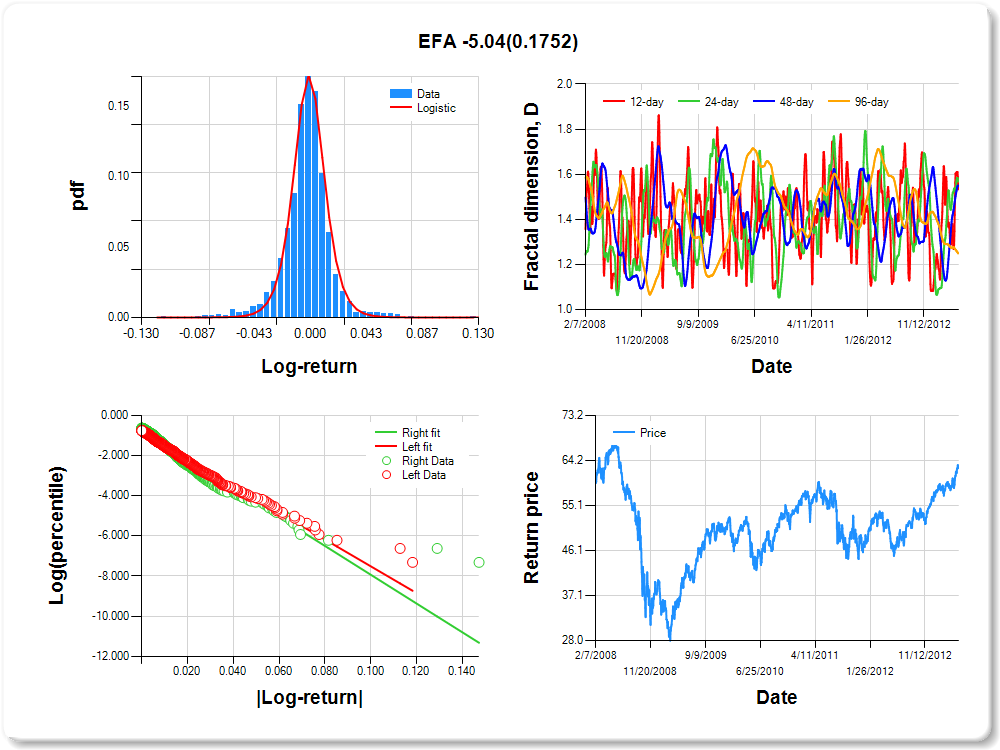

EFA

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.07 |

0.40 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.170 |

0.100 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.853 |

0.052 |

-16.535 |

0.0000 |

|log-return| |

-66.572 |

2.582 |

-25.786 |

0.0000 |

I(right-tail) |

0.085 |

0.070 |

1.205 |

0.2283 |

|log-return|*I(right-tail) |

-5.043 |

3.718 |

-1.356 |

0.1752 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.467 |

0.432 |

0.449 |

0.751 |

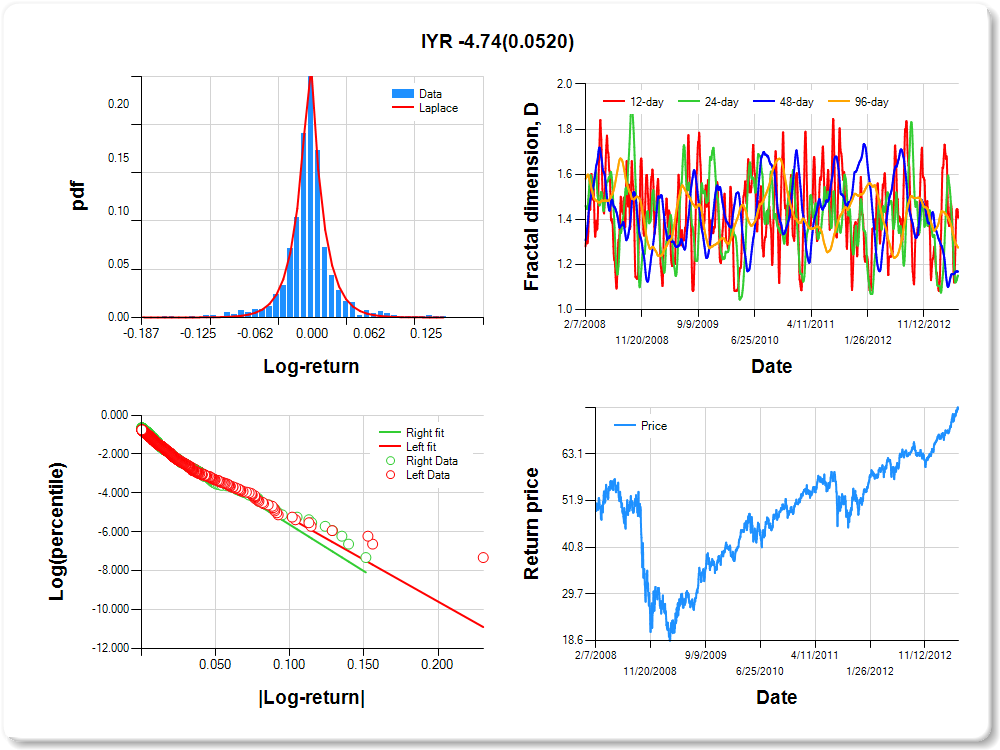

IYR

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.08 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.09 |

0.10 |

3.12 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.363 |

0.132 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.985 |

0.048 |

-20.580 |

0.0000 |

|log-return| |

-42.981 |

1.685 |

-25.504 |

0.0000 |

I(right-tail) |

0.125 |

0.066 |

1.884 |

0.0597 |

|log-return|*I(right-tail) |

-4.744 |

2.439 |

-1.945 |

0.0520 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.593 |

0.850 |

0.832 |

0.726 |

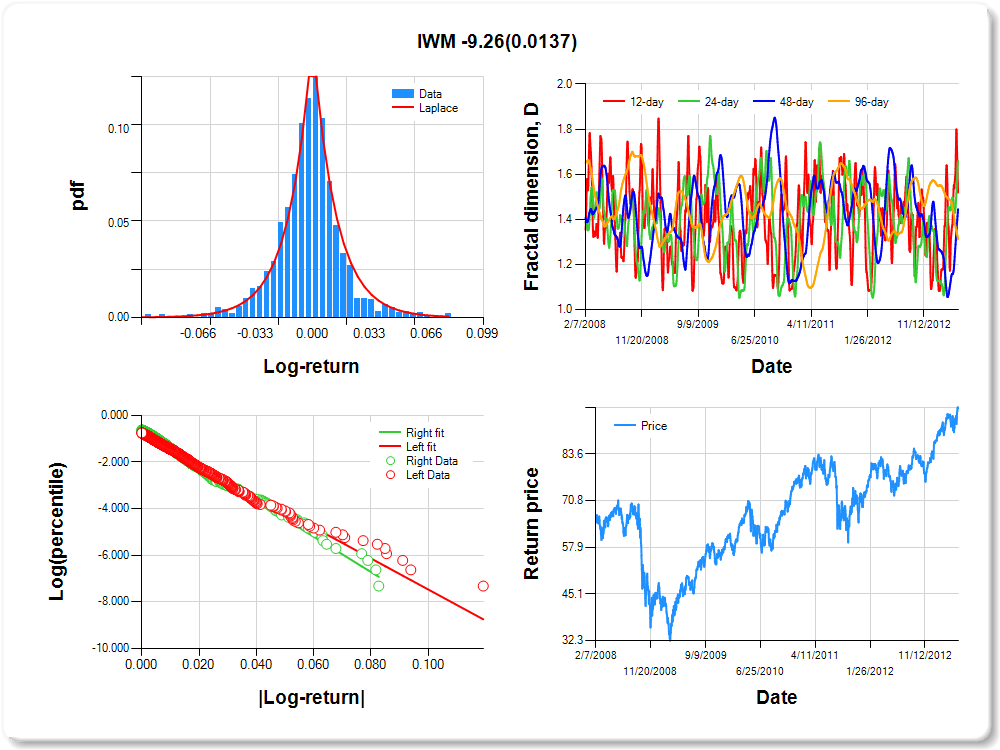

IWM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.07 |

0.11 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.342 |

0.231 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.806 |

0.052 |

-15.390 |

0.0000 |

|log-return| |

-66.589 |

2.566 |

-25.951 |

0.0000 |

I(right-tail) |

0.159 |

0.072 |

2.196 |

0.0282 |

|log-return|*I(right-tail) |

-9.260 |

3.753 |

-2.468 |

0.0137 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.481 |

0.341 |

0.555 |

0.688 |

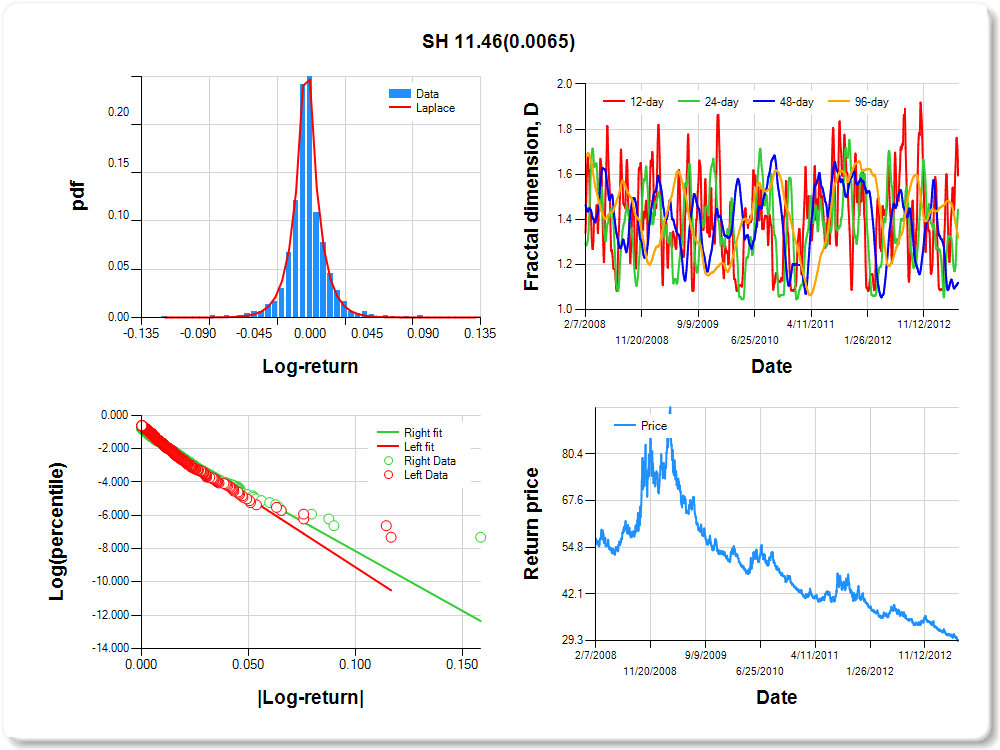

SH

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.06 |

3.89 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.273 |

0.112 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.809 |

0.046 |

-17.483 |

0.0000 |

|log-return| |

-83.054 |

3.067 |

-27.077 |

0.0000 |

I(right-tail) |

-0.184 |

0.068 |

-2.706 |

0.0069 |

|log-return|*I(right-tail) |

11.463 |

4.208 |

2.724 |

0.0065 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.406 |

0.557 |

0.881 |

0.682 |

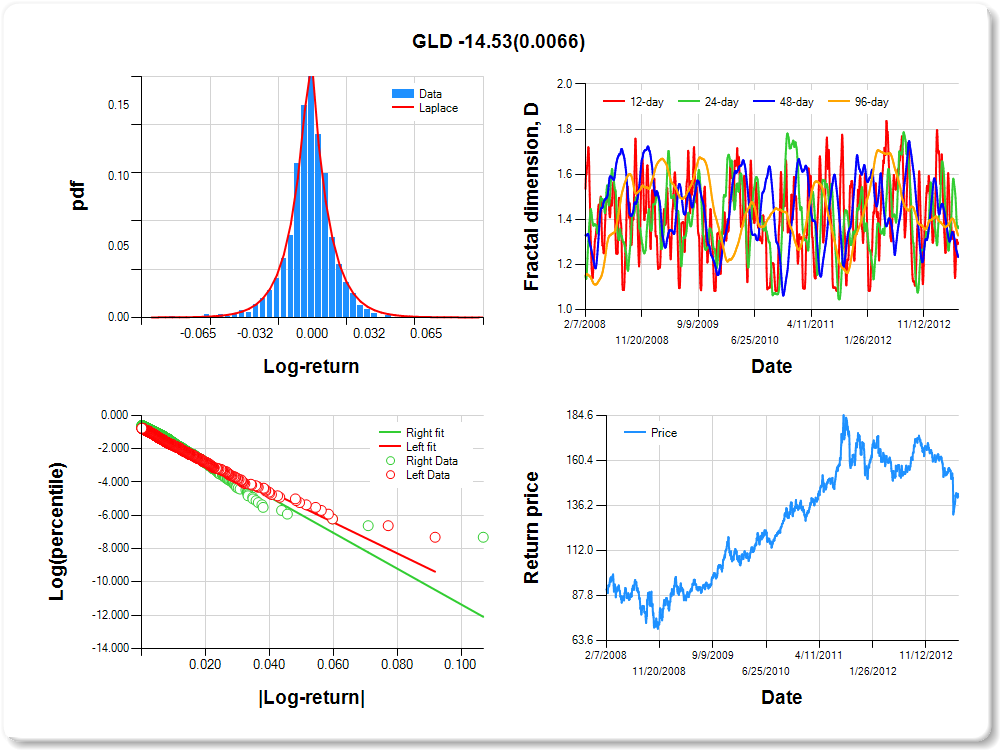

GLD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

2.50 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.120 |

0.174 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.857 |

0.052 |

-16.383 |

0.0000 |

|log-return| |

-92.848 |

3.630 |

-25.578 |

0.0000 |

I(right-tail) |

0.245 |

0.073 |

3.368 |

0.0008 |

|log-return|*I(right-tail) |

-14.527 |

5.338 |

-2.721 |

0.0066 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.703 |

0.640 |

0.767 |

0.672 |

SPY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

0.94 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.209 |

0.130 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.950 |

0.051 |

-18.615 |

0.0000 |

|log-return| |

-76.488 |

3.033 |

-25.215 |

0.0000 |

I(right-tail) |

0.156 |

0.068 |

2.284 |

0.0225 |

|log-return|*I(right-tail) |

-8.308 |

4.351 |

-1.909 |

0.0564 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.416 |

0.511 |

0.863 |

0.668 |

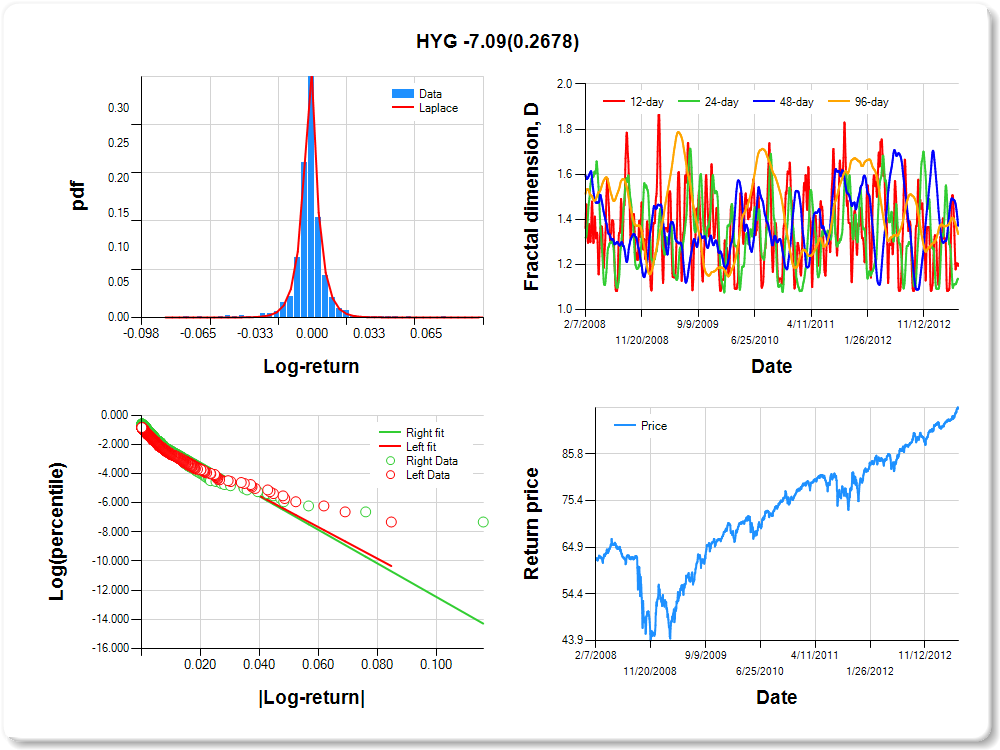

HYG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.00 |

0.01 |

0.03 |

0.04 |

2.16 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.257 |

0.080 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.197 |

0.048 |

-25.121 |

0.0000 |

|log-return| |

-108.115 |

4.564 |

-23.687 |

0.0000 |

I(right-tail) |

0.237 |

0.064 |

3.706 |

0.0002 |

|log-return|*I(right-tail) |

-7.087 |

6.393 |

-1.109 |

0.2678 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.807 |

0.863 |

0.628 |

0.665 |

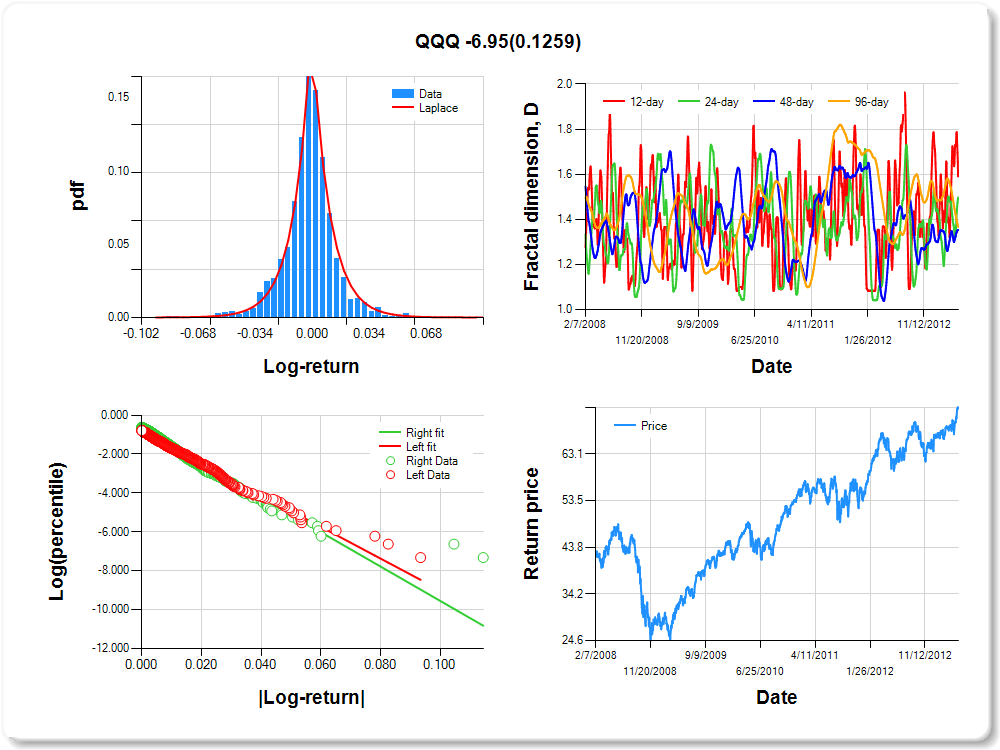

QQQ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.64 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.147 |

0.175 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.844 |

0.053 |

-15.916 |

0.0000 |

|log-return| |

-81.439 |

3.187 |

-25.552 |

0.0000 |

I(right-tail) |

0.147 |

0.072 |

2.041 |

0.0415 |

|log-return|*I(right-tail) |

-6.949 |

4.538 |

-1.531 |

0.1259 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.409 |

0.502 |

0.648 |

0.634 |

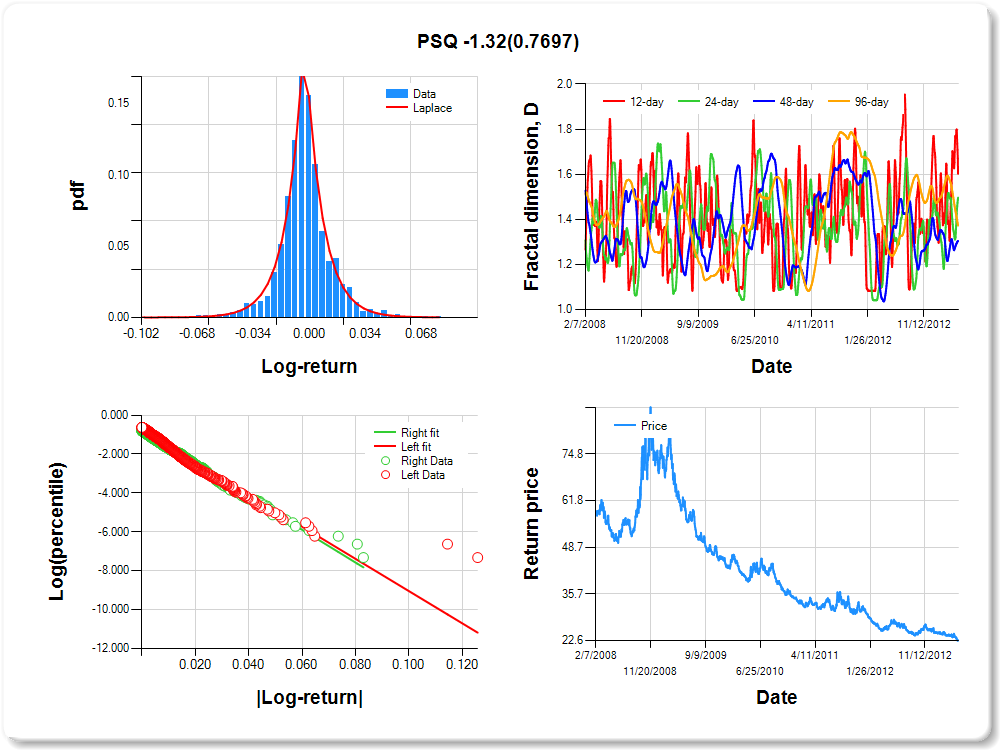

PSQ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

0.27 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.333 |

0.172 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.739 |

0.048 |

-15.452 |

0.0000 |

|log-return| |

-82.991 |

3.054 |

-27.176 |

0.0000 |

I(right-tail) |

-0.082 |

0.072 |

-1.143 |

0.2532 |

|log-return|*I(right-tail) |

-1.318 |

4.501 |

-0.293 |

0.7697 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.398 |

0.503 |

0.696 |

0.628 |

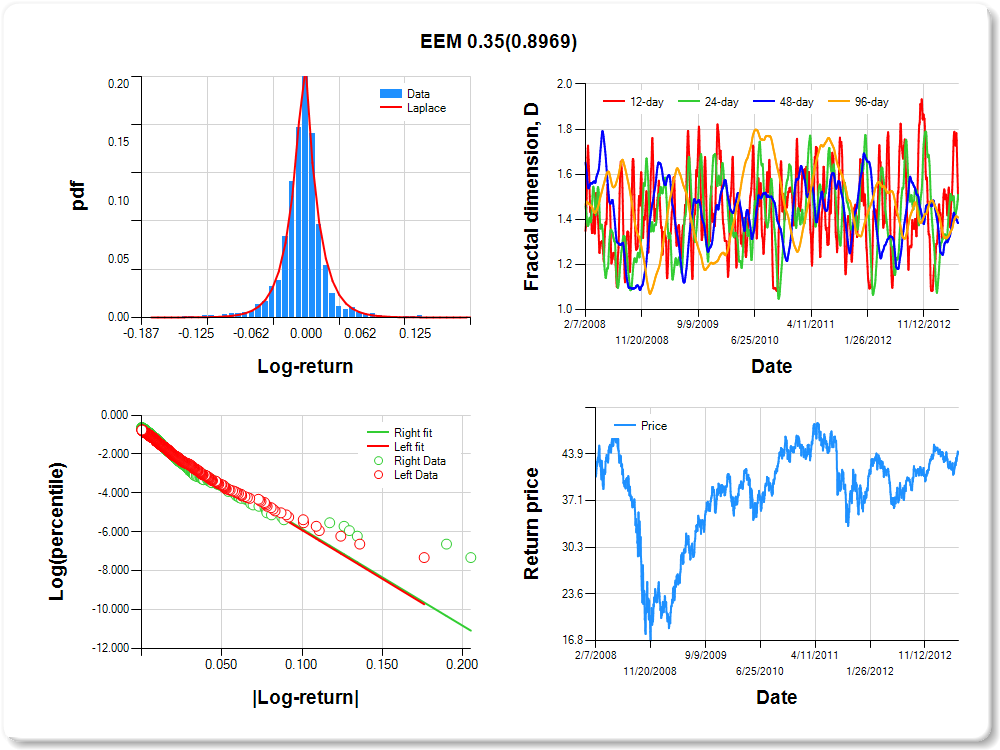

EEM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.07 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.07 |

0.08 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.118 |

0.087 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.897 |

0.050 |

-17.820 |

0.0000 |

|log-return| |

-50.072 |

1.950 |

-25.683 |

0.0000 |

I(right-tail) |

0.026 |

0.068 |

0.389 |

0.6975 |

|log-return|*I(right-tail) |

0.352 |

2.715 |

0.130 |

0.8969 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.513 |

0.491 |

0.616 |

0.592 |

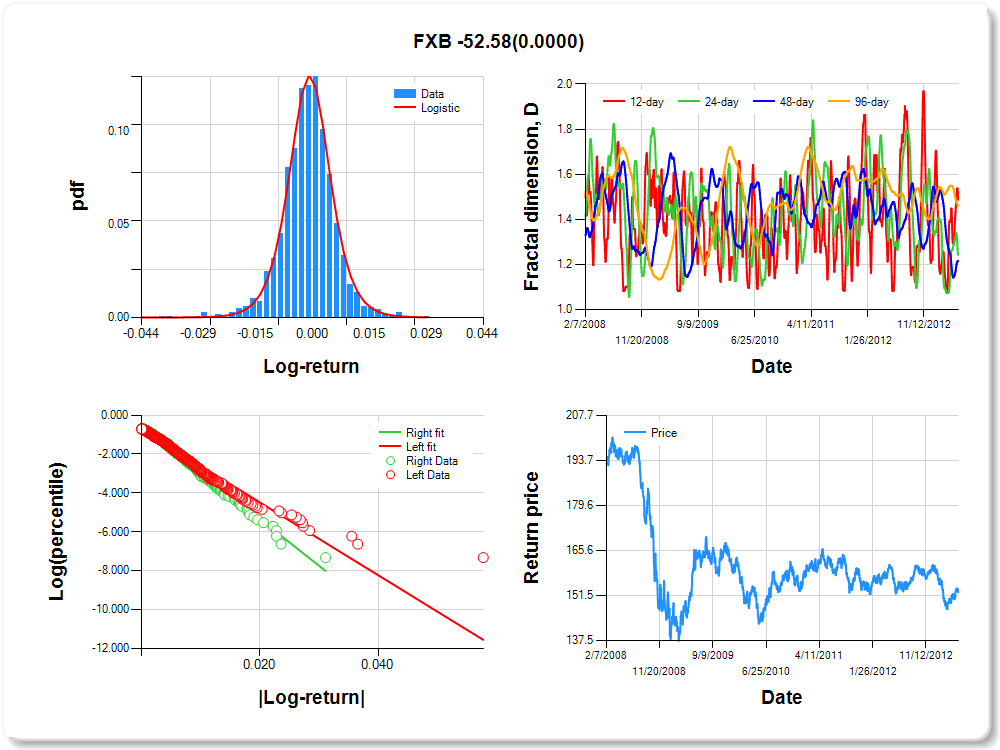

FXB

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

0.80 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.519 |

0.131 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.741 |

0.052 |

-14.279 |

0.0000 |

|log-return| |

-186.907 |

7.140 |

-26.178 |

0.0000 |

I(right-tail) |

0.196 |

0.076 |

2.580 |

0.0100 |

|log-return|*I(right-tail) |

-52.583 |

11.386 |

-4.618 |

0.0000 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.513 |

0.757 |

0.784 |

0.538 |

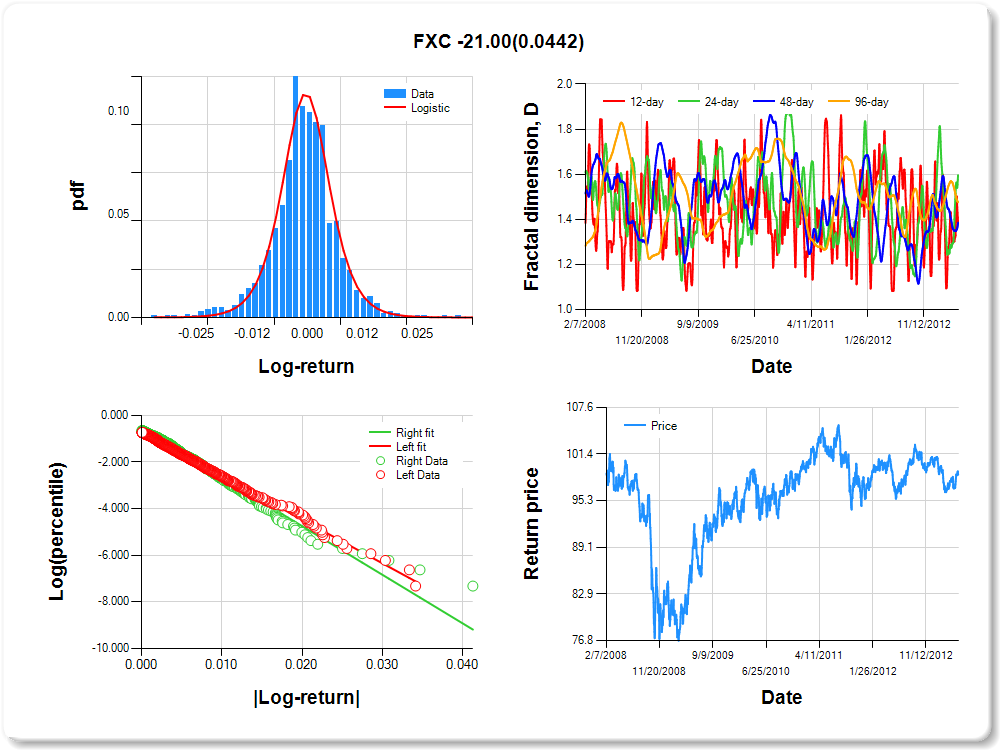

FXC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.02 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

2.39 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.145 |

0.158 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.724 |

0.053 |

-13.588 |

0.0000 |

|log-return| |

-187.148 |

7.093 |

-26.386 |

0.0000 |

I(right-tail) |

0.141 |

0.075 |

1.866 |

0.0622 |

|log-return|*I(right-tail) |

-21.000 |

10.426 |

-2.014 |

0.0442 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.615 |

0.404 |

0.614 |

0.524 |

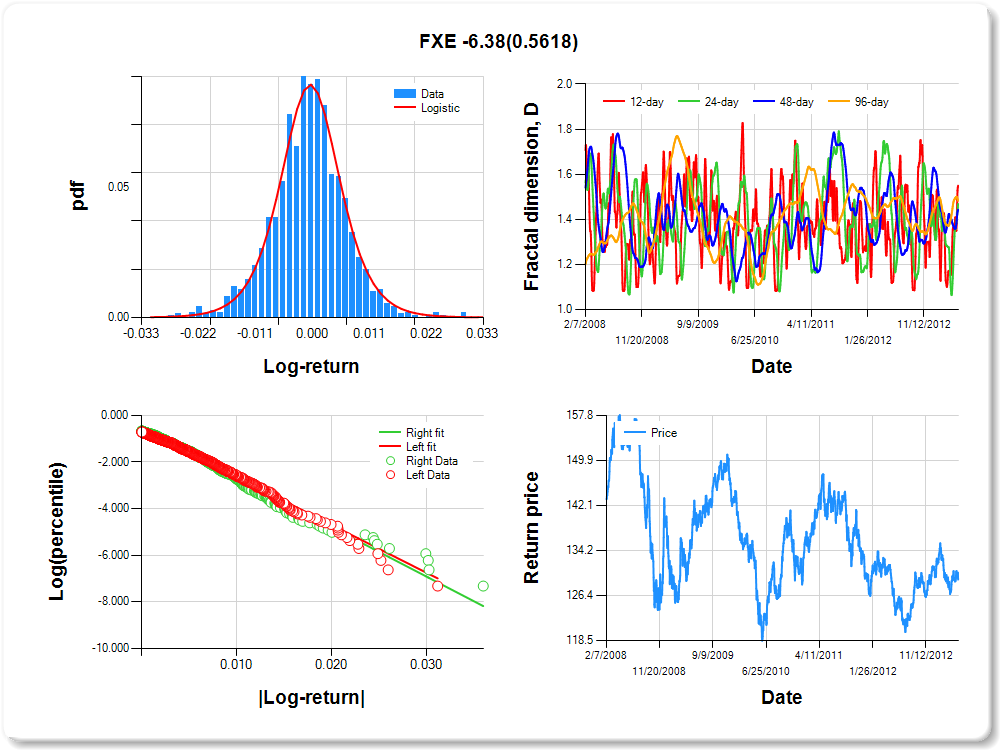

FXE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.02 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

0.98 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.109 |

0.192 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.591 |

0.056 |

-10.546 |

0.0000 |

|log-return| |

-205.168 |

7.724 |

-26.562 |

0.0000 |

I(right-tail) |

0.027 |

0.078 |

0.342 |

0.7322 |

|log-return|*I(right-tail) |

-6.379 |

10.991 |

-0.580 |

0.5618 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.450 |

0.531 |

0.557 |

0.518 |

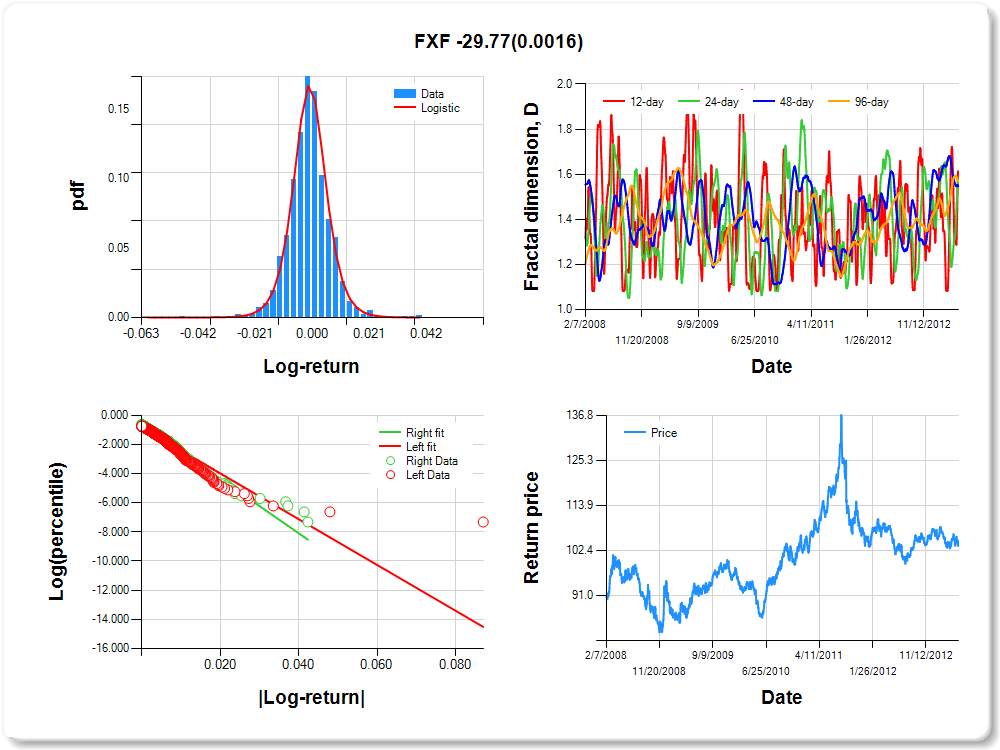

FXF

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.02 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

1.47 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.597 |

0.103 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.844 |

0.052 |

-16.103 |

0.0000 |

|log-return| |

-156.957 |

6.407 |

-24.499 |

0.0000 |

I(right-tail) |

0.230 |

0.074 |

3.110 |

0.0019 |

|log-return|*I(right-tail) |

-29.771 |

9.393 |

-3.169 |

0.0016 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.386 |

0.422 |

0.454 |

0.430 |

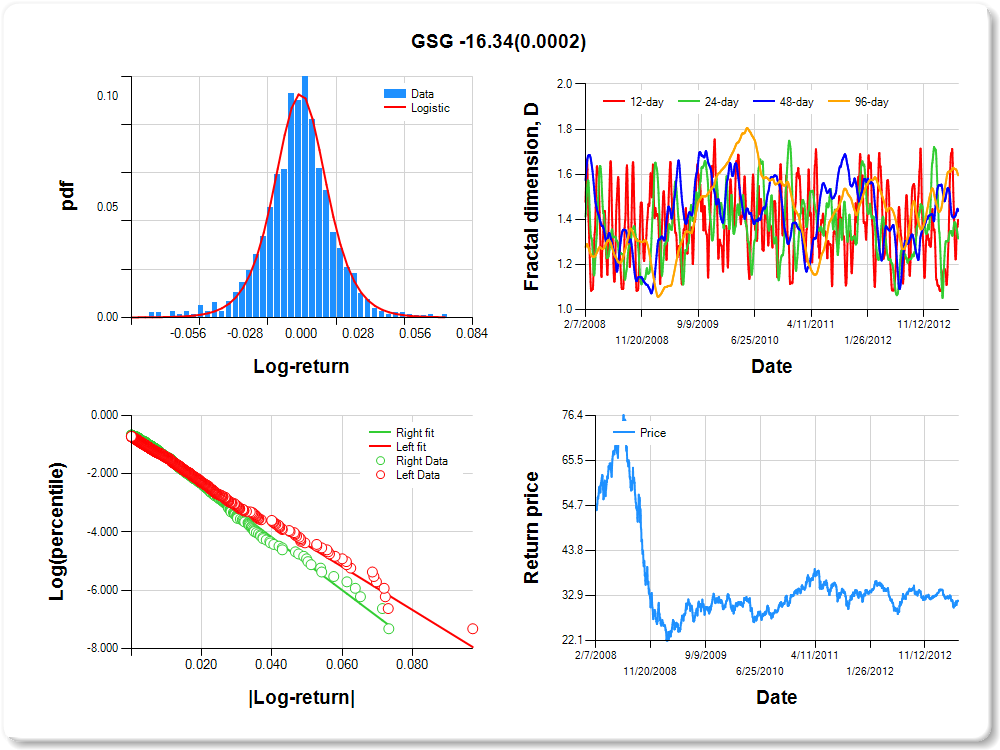

GSG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.05 |

0.97 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.259 |

0.169 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.738 |

0.052 |

-14.058 |

0.0000 |

|log-return| |

-74.109 |

2.801 |

-26.460 |

0.0000 |

I(right-tail) |

0.181 |

0.076 |

2.379 |

0.0175 |

|log-return|*I(right-tail) |

-16.336 |

4.356 |

-3.750 |

0.0002 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.602 |

0.685 |

0.563 |

0.404 |

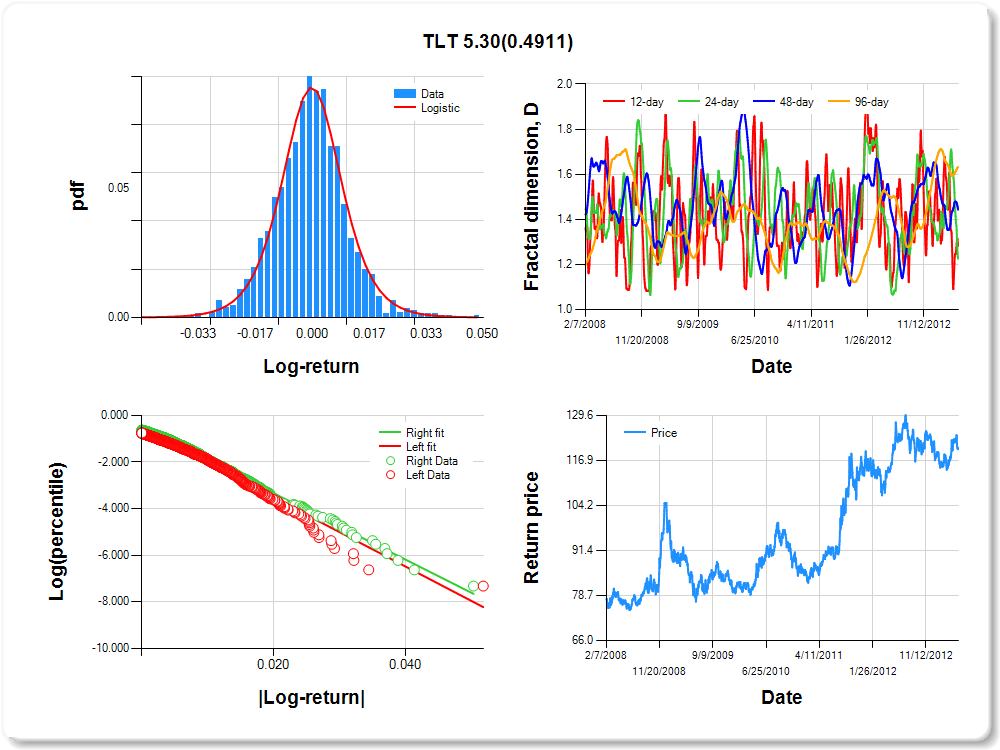

TLT

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

0.48 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.051 |

0.193 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.573 |

0.059 |

-9.656 |

0.0000 |

|log-return| |

-147.766 |

5.728 |

-25.799 |

0.0000 |

I(right-tail) |

0.083 |

0.080 |

1.037 |

0.3001 |

|log-return|*I(right-tail) |

5.302 |

7.698 |

0.689 |

0.4911 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.718 |

0.774 |

0.557 |

0.368 |

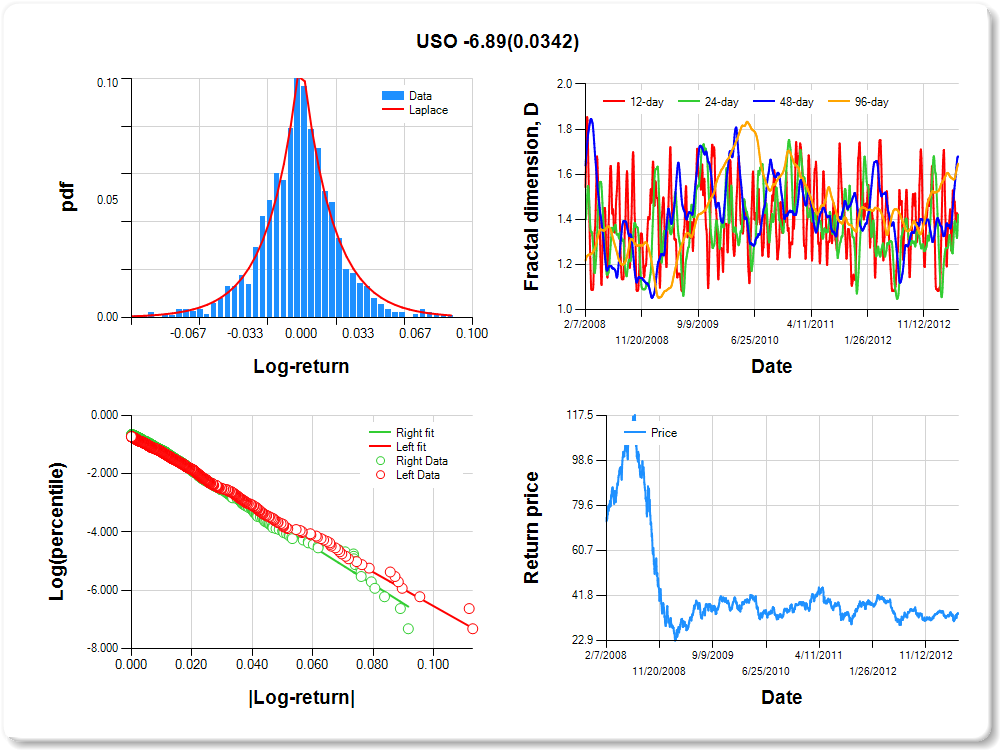

USO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.07 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.06 |

0.08 |

1.94 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.203 |

0.303 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.711 |

0.054 |

-13.283 |

0.0000 |

|log-return| |

-58.331 |

2.210 |

-26.395 |

0.0000 |

I(right-tail) |

0.127 |

0.075 |

1.687 |

0.0918 |

|log-return|*I(right-tail) |

-6.889 |

3.250 |

-2.120 |

0.0342 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.578 |

0.580 |

0.321 |

0.353 |

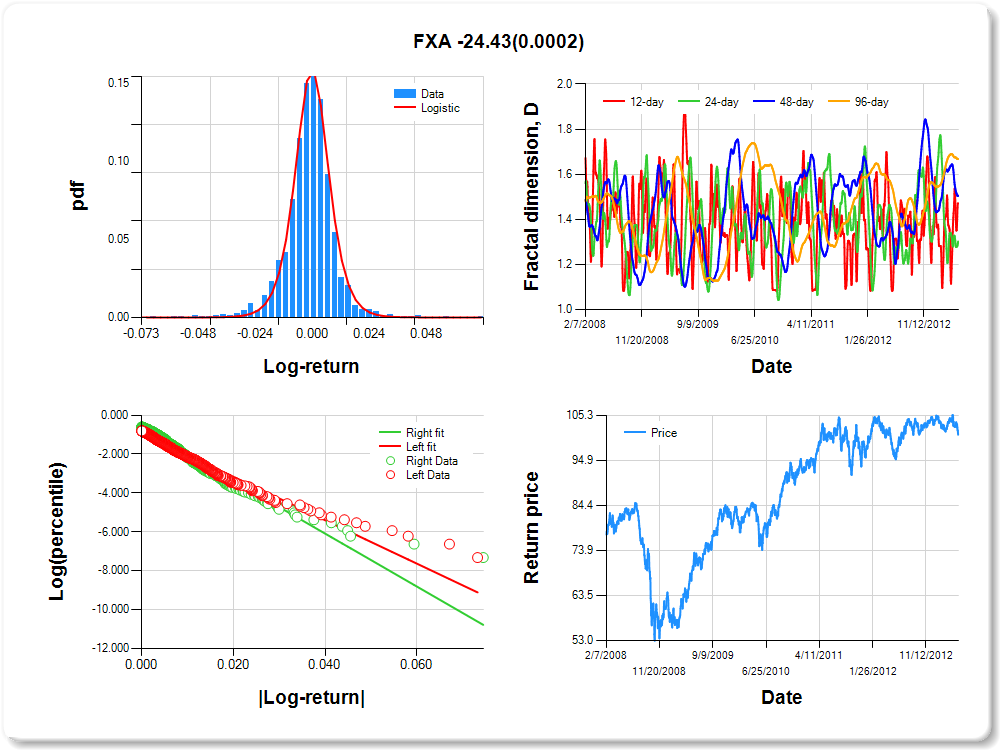

FXA

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

0.43 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.013 |

0.108 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.927 |

0.052 |

-17.846 |

0.0000 |

|log-return| |

-111.580 |

4.452 |

-25.062 |

0.0000 |

I(right-tail) |

0.292 |

0.072 |

4.071 |

0.0000 |

|log-return|*I(right-tail) |

-24.428 |

6.640 |

-3.679 |

0.0002 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.529 |

0.698 |

0.494 |

0.332 |