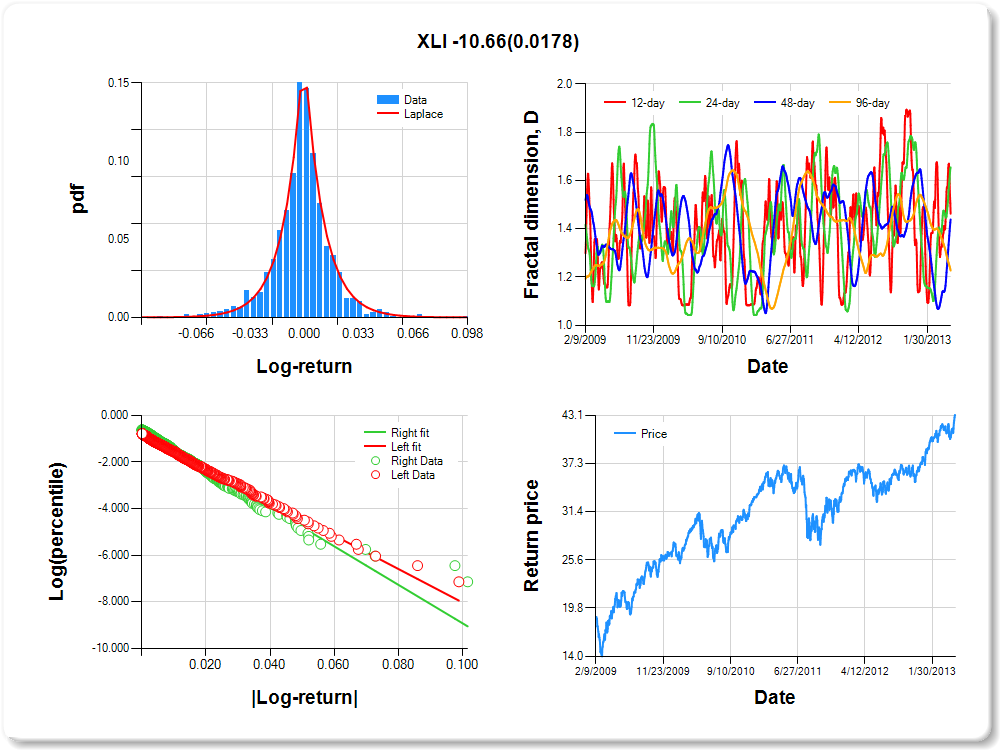

XLI

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

1.48 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.001 |

0.198 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.840 |

0.058 |

-14.472 |

0.0000 |

|log-return| |

-71.757 |

3.072 |

-23.358 |

0.0000 |

I(right-tail) |

0.177 |

0.079 |

2.228 |

0.0261 |

|log-return|*I(right-tail) |

-10.662 |

4.494 |

-2.372 |

0.0178 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.537 |

0.345 |

0.561 |

0.773 |

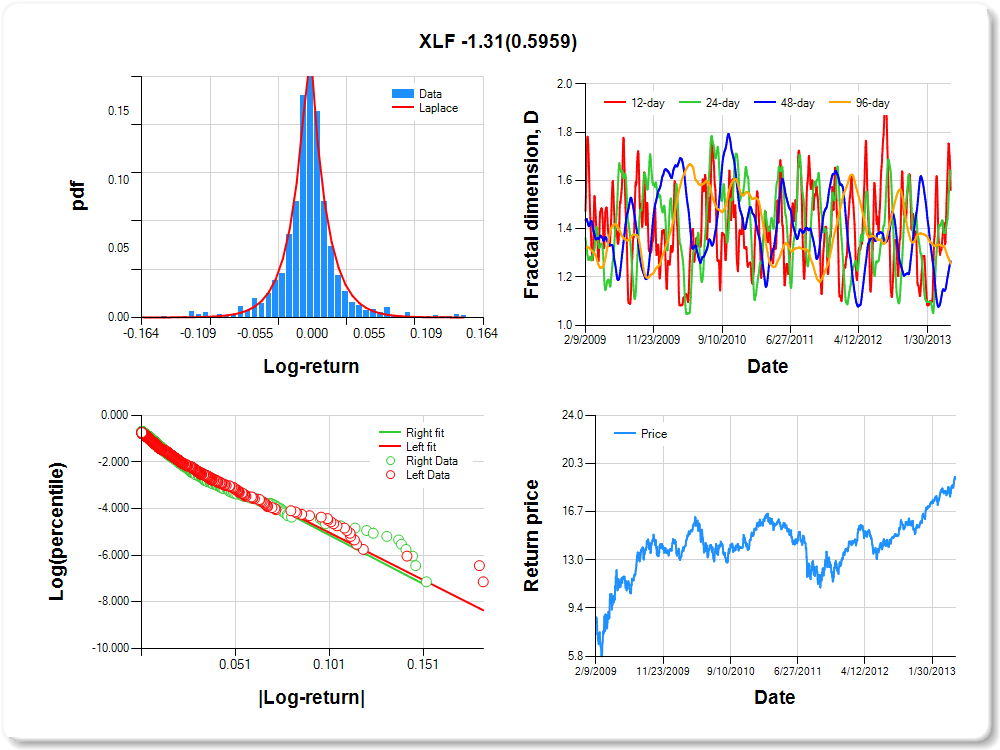

XLF

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.11 |

-0.10 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.10 |

0.14 |

1.18 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.158 |

0.164 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.958 |

0.053 |

-18.231 |

0.0000 |

|log-return| |

-40.634 |

1.729 |

-23.507 |

0.0000 |

I(right-tail) |

0.027 |

0.073 |

0.365 |

0.7154 |

|log-return|*I(right-tail) |

-1.309 |

2.467 |

-0.530 |

0.5959 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.439 |

0.358 |

0.734 |

0.745 |

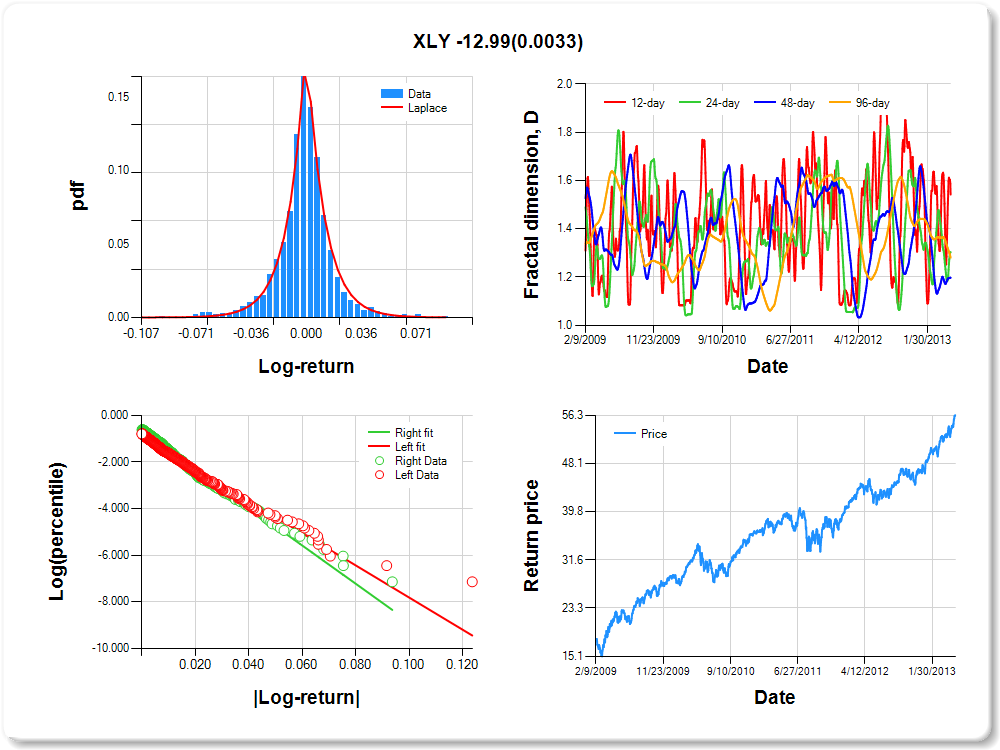

XLY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

0.44 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.262 |

0.182 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.919 |

0.057 |

-16.239 |

0.0000 |

|log-return| |

-68.910 |

2.991 |

-23.036 |

0.0000 |

I(right-tail) |

0.255 |

0.078 |

3.261 |

0.0011 |

|log-return|*I(right-tail) |

-12.994 |

4.408 |

-2.948 |

0.0033 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.458 |

0.696 |

0.803 |

0.720 |

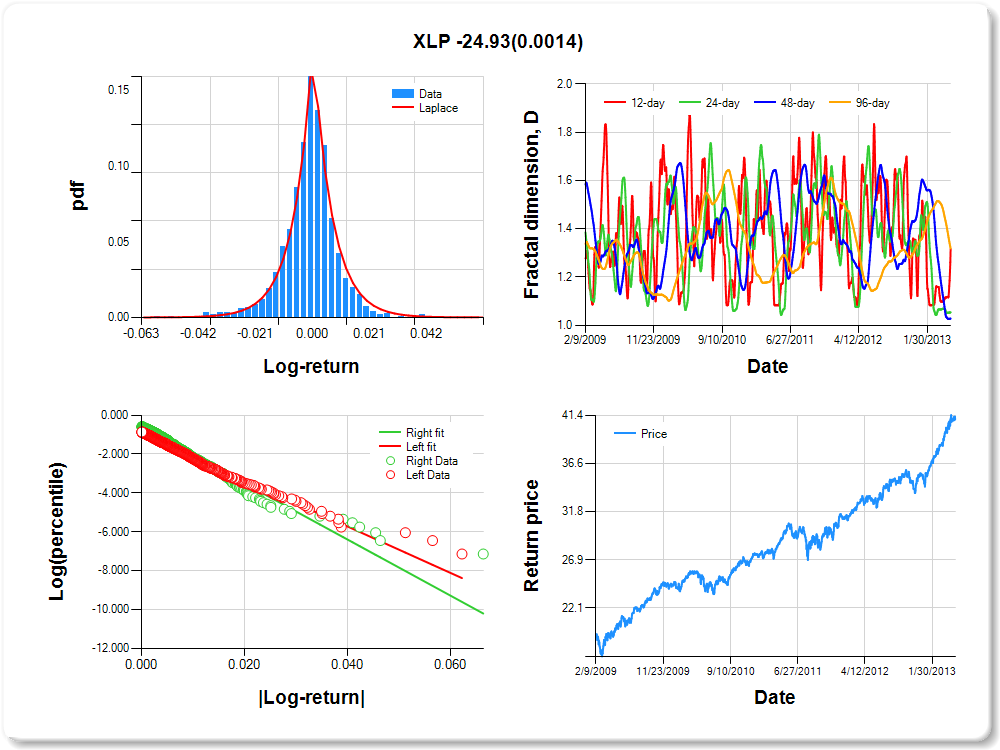

XLP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

0.04 |

0.54 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.015 |

0.189 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.924 |

0.060 |

-15.334 |

0.0000 |

|log-return| |

-119.454 |

5.353 |

-22.313 |

0.0000 |

I(right-tail) |

0.330 |

0.081 |

4.069 |

0.0001 |

|log-return|*I(right-tail) |

-24.925 |

7.802 |

-3.195 |

0.0014 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.683 |

0.946 |

0.972 |

0.681 |

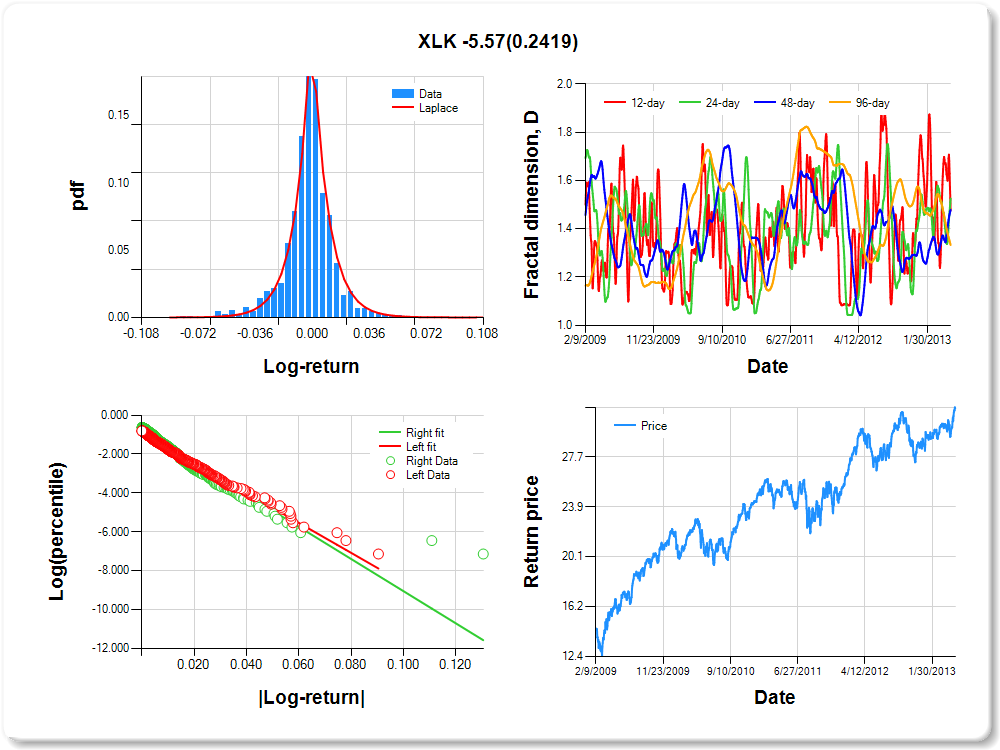

XLK

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

1.46 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.284 |

0.155 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.895 |

0.058 |

-15.552 |

0.0000 |

|log-return| |

-77.163 |

3.344 |

-23.078 |

0.0000 |

I(right-tail) |

0.131 |

0.078 |

1.690 |

0.0912 |

|log-return|*I(right-tail) |

-5.568 |

4.756 |

-1.171 |

0.2419 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.523 |

0.474 |

0.522 |

0.667 |

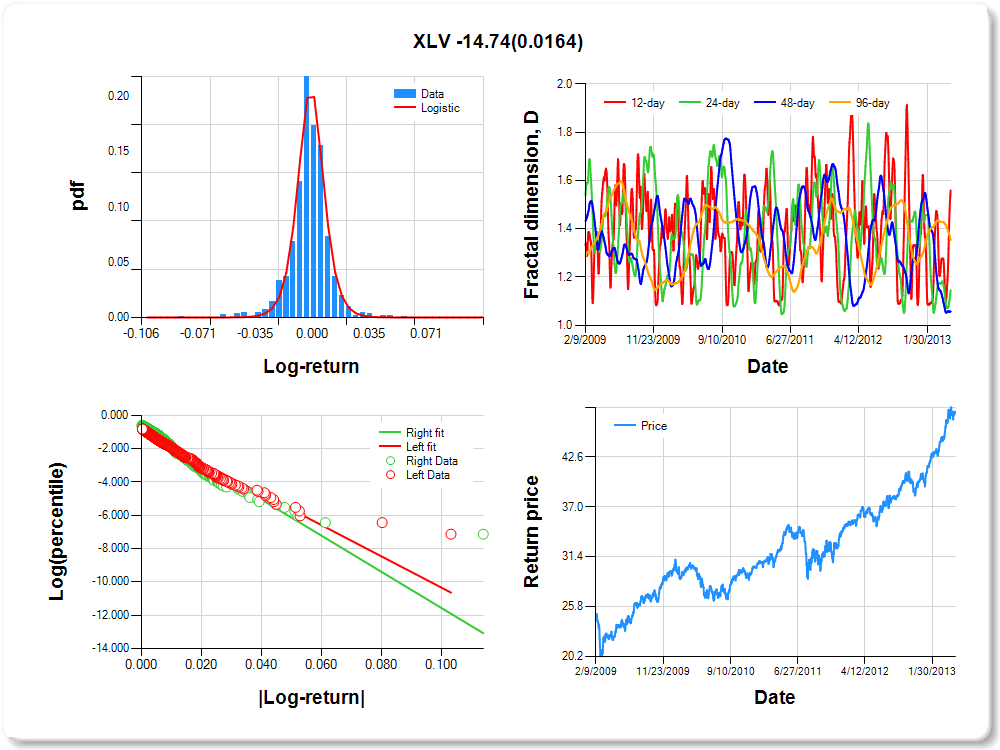

XLV

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

0.21 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.068 |

0.083 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.977 |

0.057 |

-17.174 |

0.0000 |

|log-return| |

-93.834 |

4.201 |

-22.335 |

0.0000 |

I(right-tail) |

0.250 |

0.078 |

3.223 |

0.0013 |

|log-return|*I(right-tail) |

-14.737 |

6.130 |

-2.404 |

0.0164 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.441 |

0.855 |

0.943 |

0.647 |

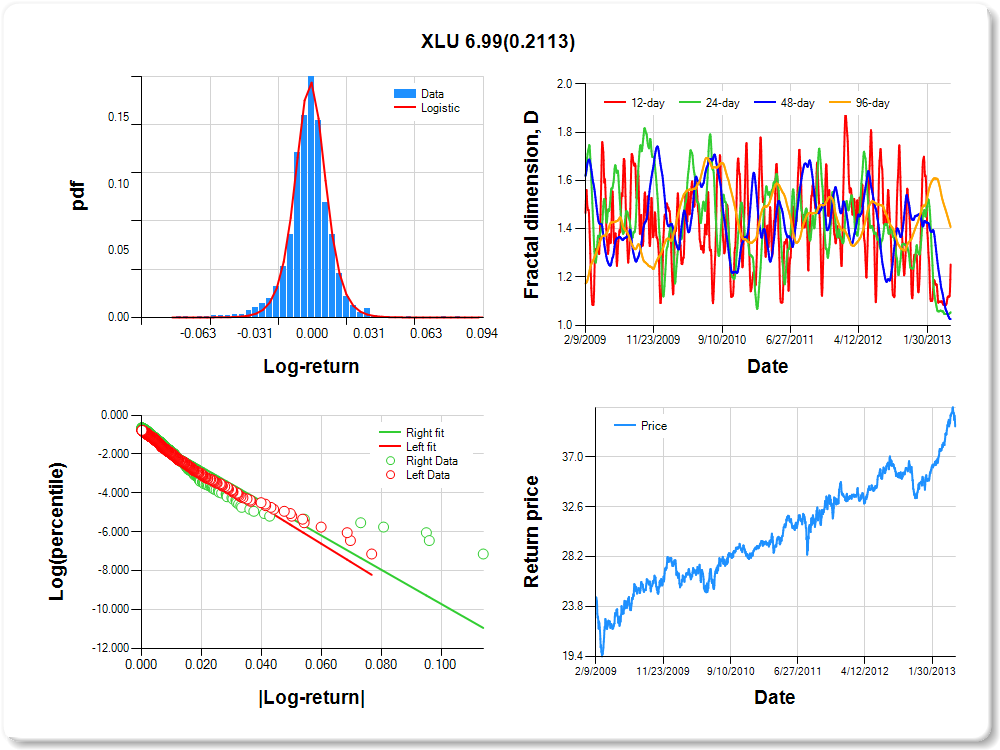

XLU

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

1.37 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.321 |

0.097 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.899 |

0.056 |

-16.004 |

0.0000 |

|log-return| |

-94.911 |

4.101 |

-23.145 |

0.0000 |

I(right-tail) |

0.005 |

0.076 |

0.067 |

0.9462 |

|log-return|*I(right-tail) |

6.995 |

5.593 |

1.251 |

0.2113 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.748 |

0.946 |

0.974 |

0.593 |

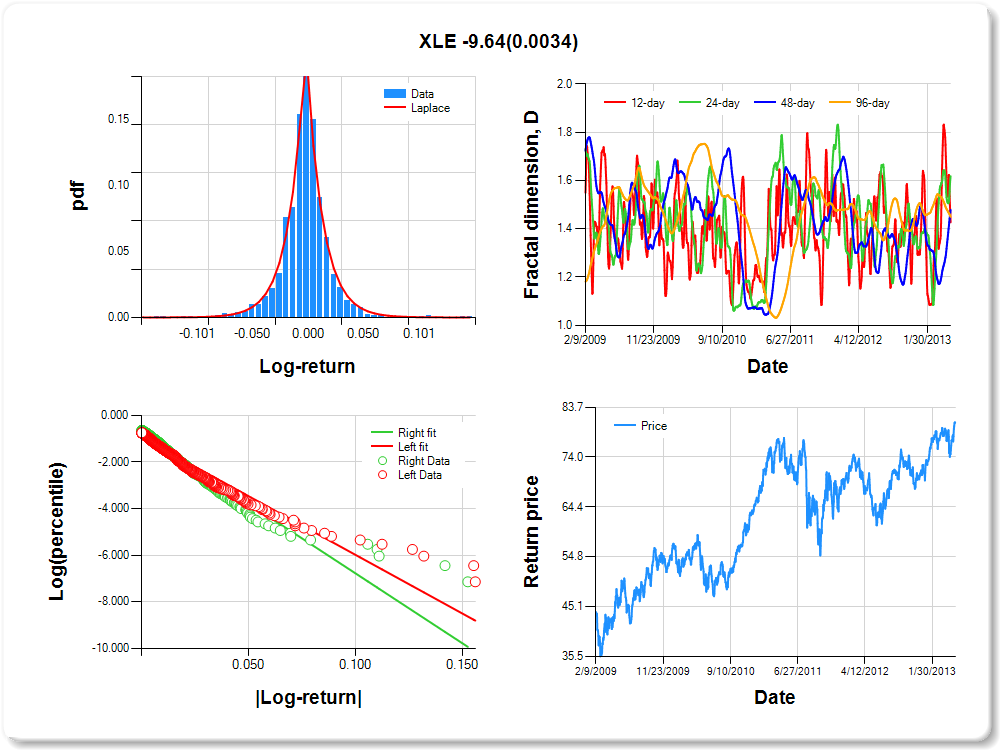

XLE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.07 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.07 |

1.40 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.025 |

0.164 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.954 |

0.053 |

-17.859 |

0.0000 |

|log-return| |

-50.293 |

2.170 |

-23.176 |

0.0000 |

I(right-tail) |

0.171 |

0.075 |

2.284 |

0.0225 |

|log-return|*I(right-tail) |

-9.644 |

3.285 |

-2.936 |

0.0034 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.573 |

0.382 |

0.522 |

0.550 |

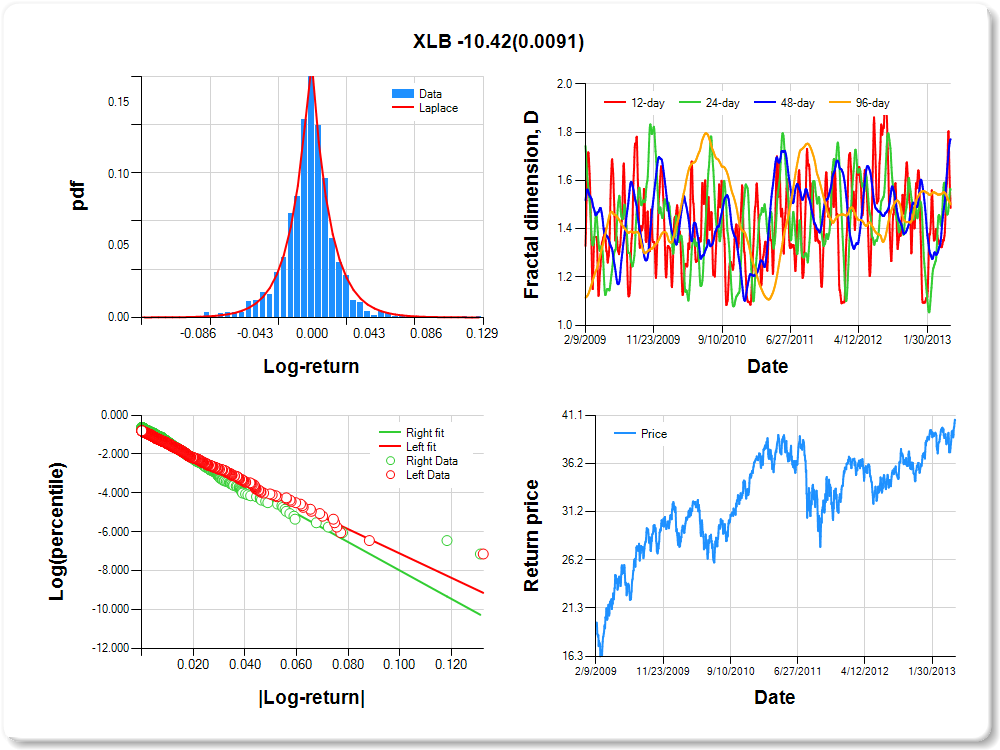

XLB

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.026 |

0.184 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.838 |

0.059 |

-14.245 |

0.0000 |

|log-return| |

-62.572 |

2.703 |

-23.145 |

0.0000 |

I(right-tail) |

0.171 |

0.080 |

2.135 |

0.0330 |

|log-return|*I(right-tail) |

-10.417 |

3.988 |

-2.612 |

0.0091 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.513 |

0.439 |

0.229 |

0.499 |