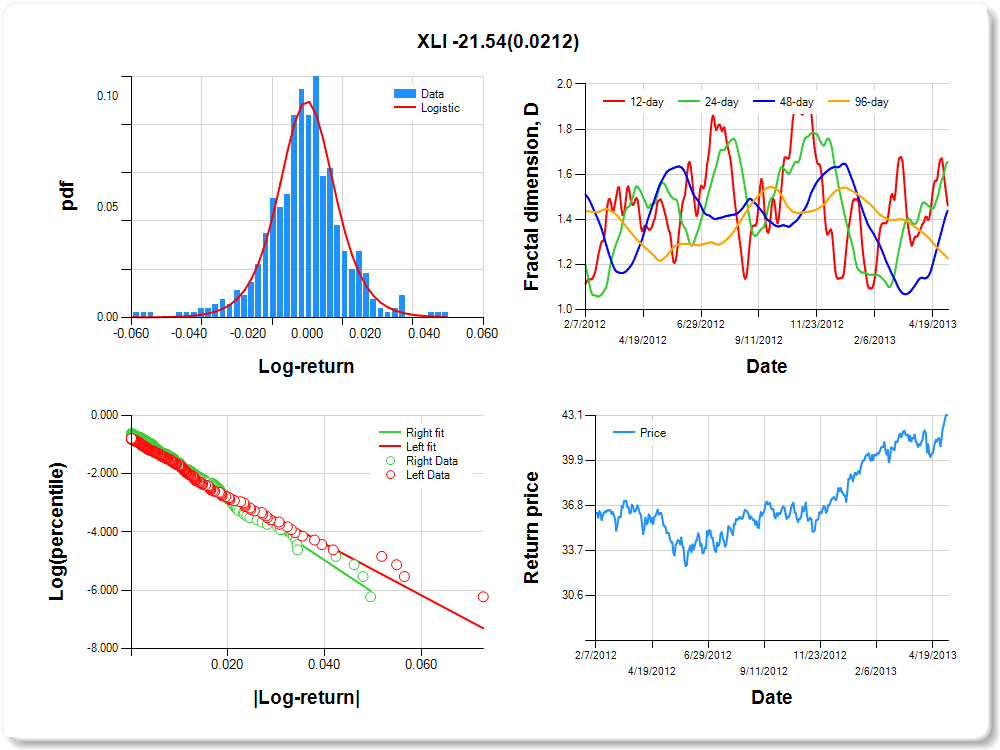

XLI

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

1.74 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.355 |

0.175 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.861 |

0.092 |

-9.319 |

0.0000 |

|log-return| |

-88.226 |

6.169 |

-14.302 |

0.0000 |

I(right-tail) |

0.302 |

0.130 |

2.331 |

0.0201 |

|log-return|*I(right-tail) |

-21.539 |

9.319 |

-2.311 |

0.0212 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.537 |

0.345 |

0.561 |

0.773 |

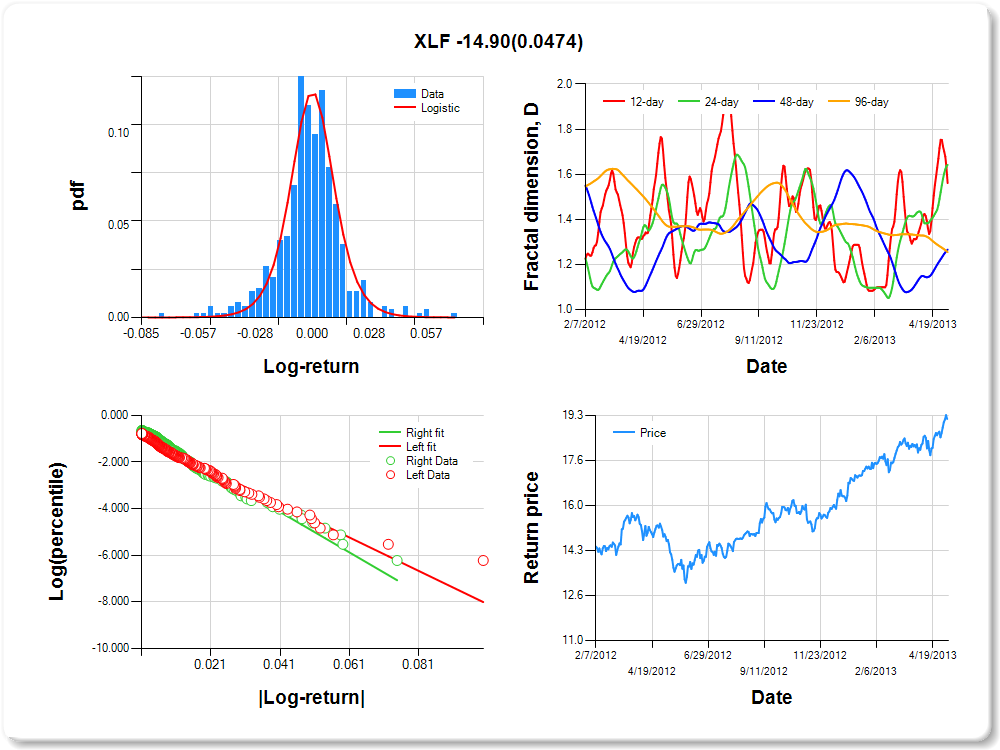

XLF

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.06 |

3.03 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.278 |

0.140 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.901 |

0.089 |

-10.088 |

0.0000 |

|log-return| |

-71.574 |

4.993 |

-14.336 |

0.0000 |

I(right-tail) |

0.262 |

0.126 |

2.073 |

0.0387 |

|log-return|*I(right-tail) |

-14.900 |

7.497 |

-1.988 |

0.0474 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.439 |

0.358 |

0.734 |

0.745 |

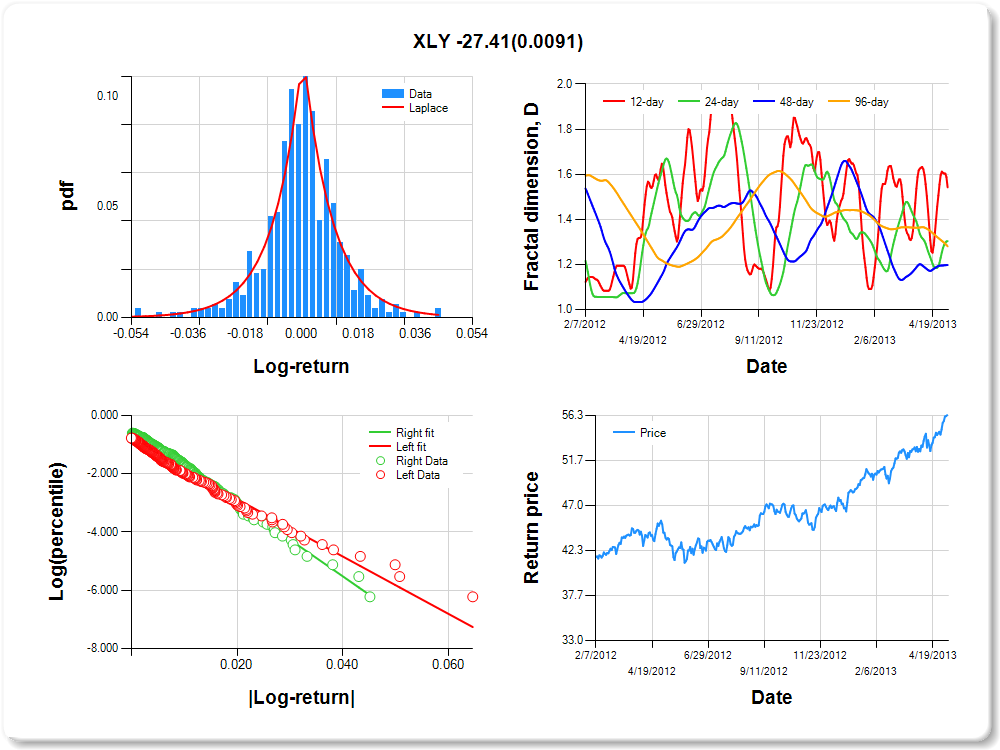

XLY

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

2.93 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.347 |

0.287 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.904 |

0.089 |

-10.153 |

0.0000 |

|log-return| |

-98.409 |

6.831 |

-14.406 |

0.0000 |

I(right-tail) |

0.418 |

0.129 |

3.250 |

0.0012 |

|log-return|*I(right-tail) |

-27.410 |

10.471 |

-2.618 |

0.0091 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.458 |

0.696 |

0.803 |

0.720 |

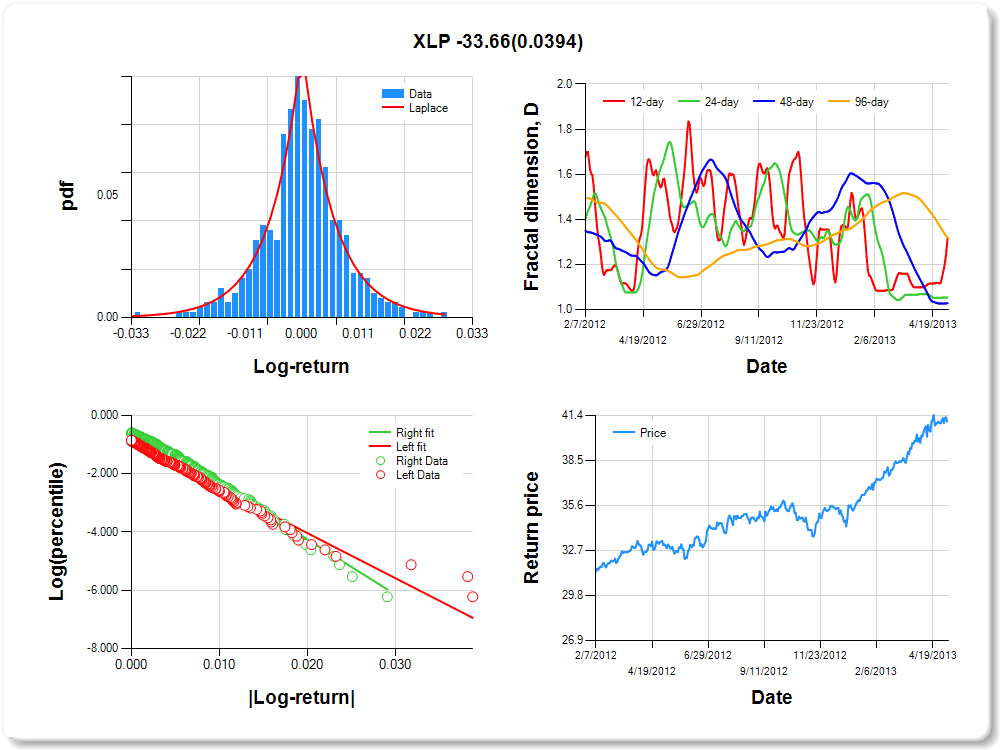

XLP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.01 |

0.02 |

0.02 |

2.56 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.278 |

0.312 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.912 |

0.096 |

-9.532 |

0.0000 |

|log-return| |

-154.936 |

11.204 |

-13.829 |

0.0000 |

I(right-tail) |

0.462 |

0.134 |

3.452 |

0.0006 |

|log-return|*I(right-tail) |

-33.661 |

16.294 |

-2.066 |

0.0394 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.683 |

0.946 |

0.972 |

0.681 |

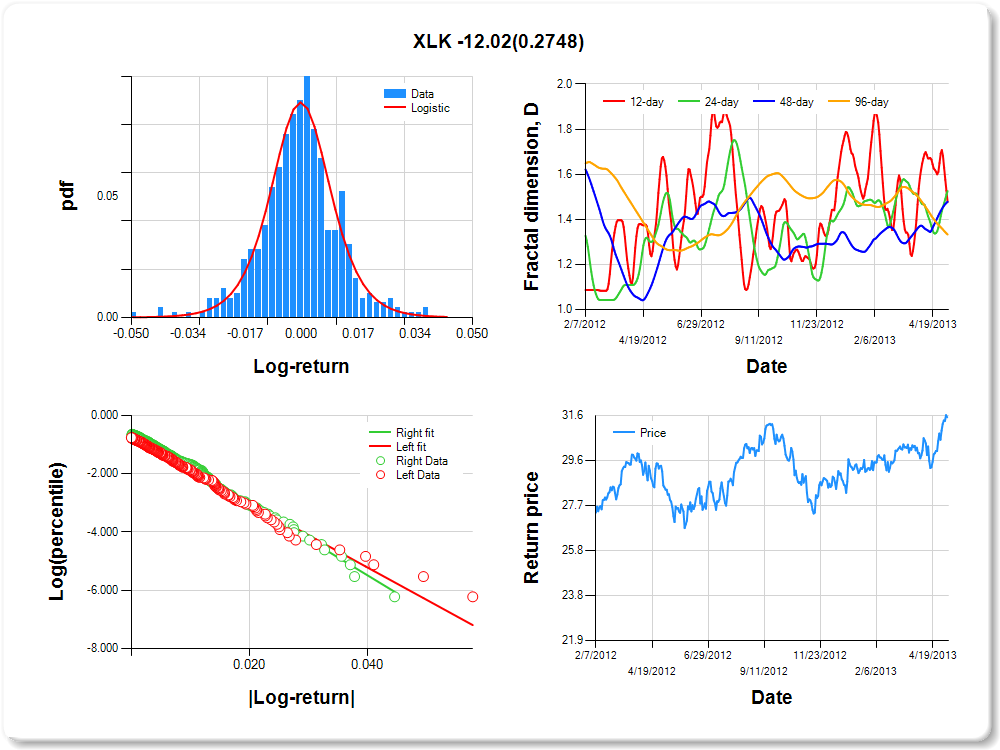

XLK

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

2.56 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.242 |

0.194 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.768 |

0.094 |

-8.139 |

0.0000 |

|log-return| |

-111.001 |

7.636 |

-14.536 |

0.0000 |

I(right-tail) |

0.214 |

0.133 |

1.613 |

0.1074 |

|log-return|*I(right-tail) |

-12.024 |

10.998 |

-1.093 |

0.2748 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.523 |

0.474 |

0.522 |

0.667 |

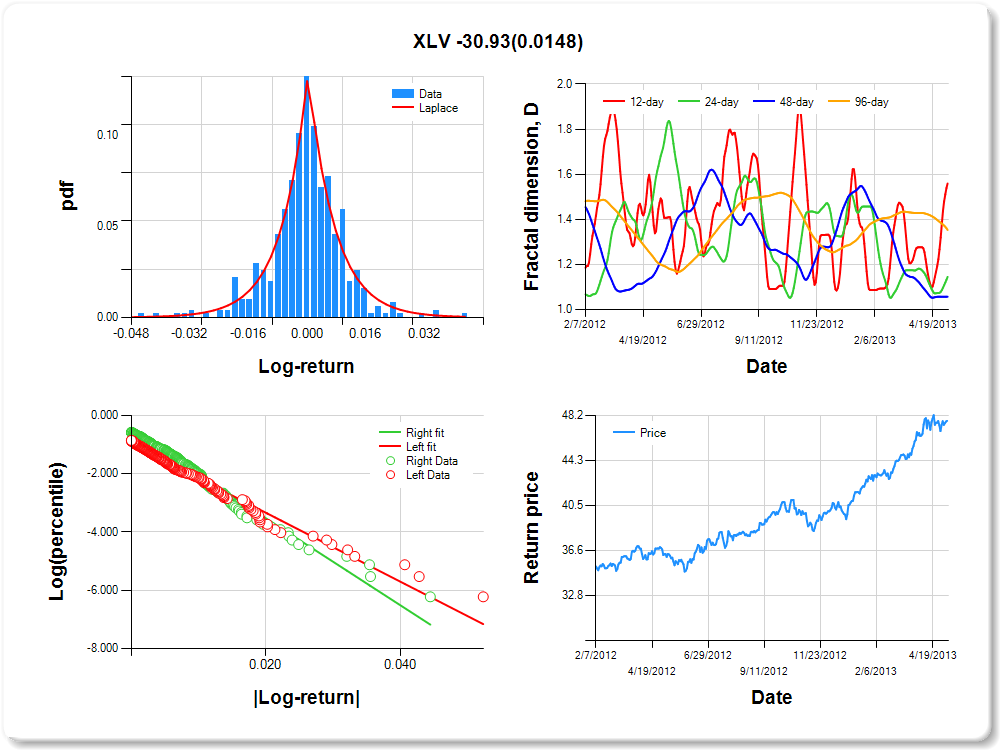

XLV

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

2.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.182 |

0.254 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.958 |

0.094 |

-10.171 |

0.0000 |

|log-return| |

-118.141 |

8.568 |

-13.789 |

0.0000 |

I(right-tail) |

0.435 |

0.129 |

3.364 |

0.0008 |

|log-return|*I(right-tail) |

-30.927 |

12.650 |

-2.445 |

0.0148 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.441 |

0.855 |

0.943 |

0.647 |

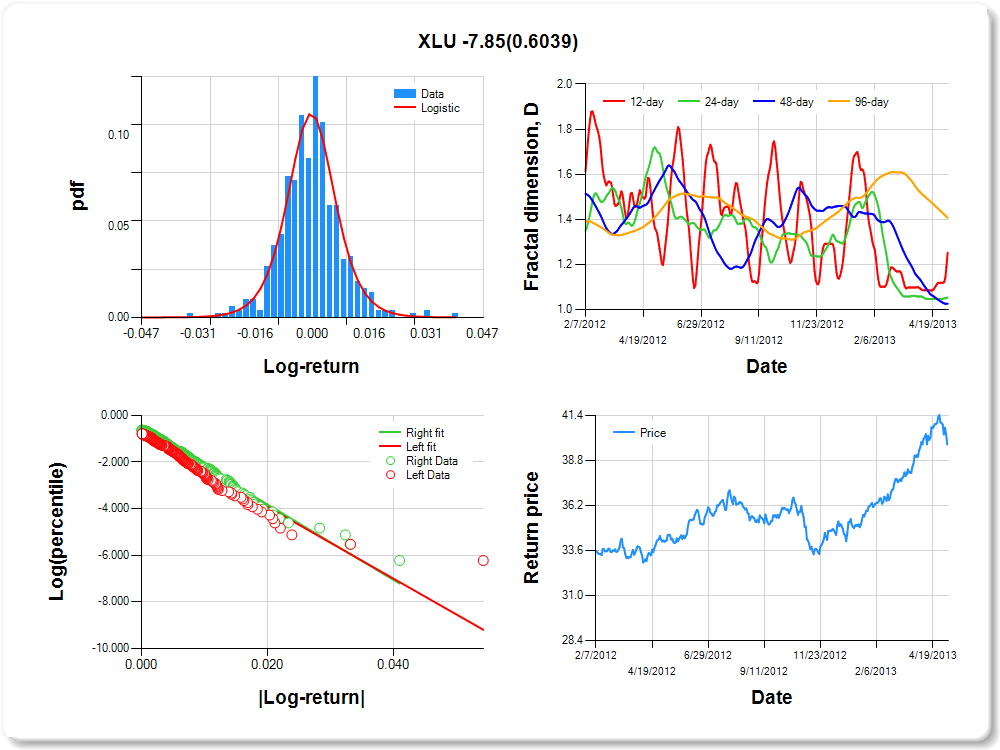

XLU

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.02 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.01 |

0.02 |

0.03 |

4.70 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.260 |

0.153 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.826 |

0.095 |

-8.656 |

0.0000 |

|log-return| |

-153.707 |

11.037 |

-13.927 |

0.0000 |

I(right-tail) |

0.260 |

0.132 |

1.975 |

0.0489 |

|log-return|*I(right-tail) |

-7.848 |

15.120 |

-0.519 |

0.6039 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.748 |

0.946 |

0.974 |

0.593 |

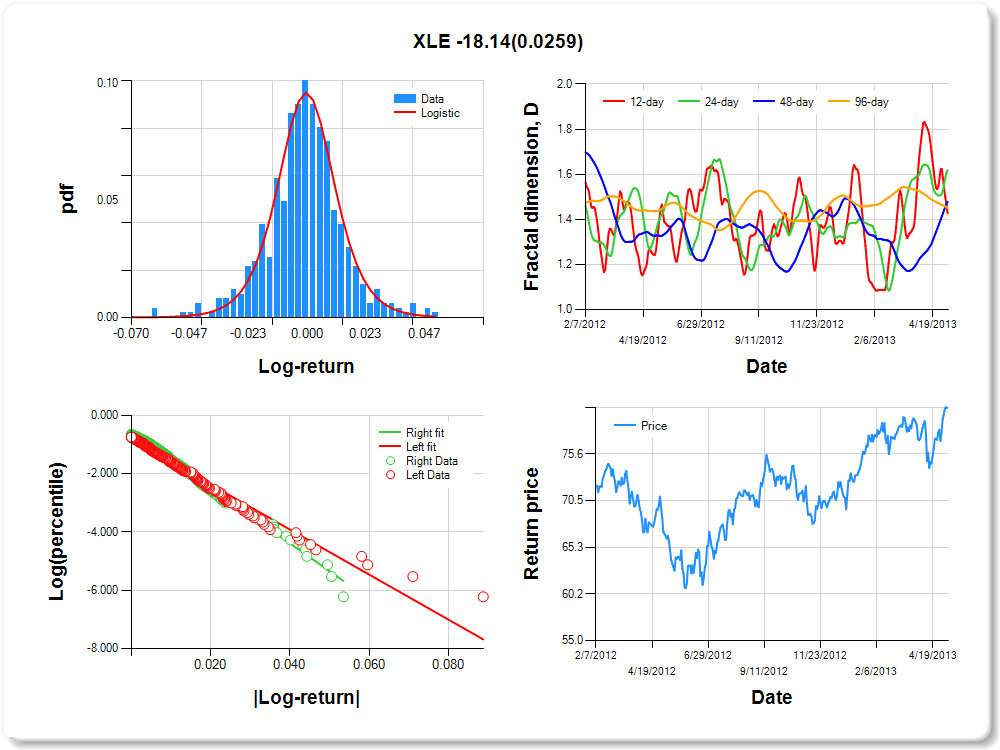

XLE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

3.93 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.449 |

0.179 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.820 |

0.090 |

-9.112 |

0.0000 |

|log-return| |

-77.311 |

5.288 |

-14.620 |

0.0000 |

I(right-tail) |

0.253 |

0.129 |

1.958 |

0.0508 |

|log-return|*I(right-tail) |

-18.137 |

8.115 |

-2.235 |

0.0259 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.573 |

0.382 |

0.522 |

0.550 |

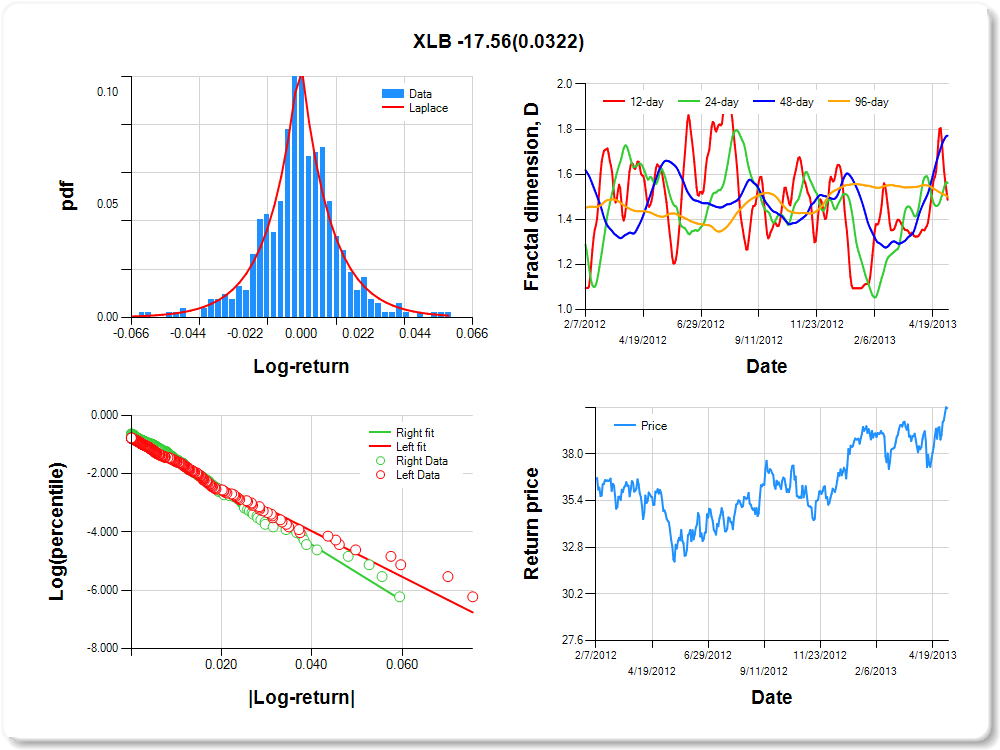

XLB

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.220 |

0.294 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.831 |

0.092 |

-9.029 |

0.0000 |

|log-return| |

-78.195 |

5.403 |

-14.473 |

0.0000 |

I(right-tail) |

0.242 |

0.129 |

1.872 |

0.0618 |

|log-return|*I(right-tail) |

-17.557 |

8.173 |

-2.148 |

0.0322 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.513 |

0.439 |

0.229 |

0.499 |