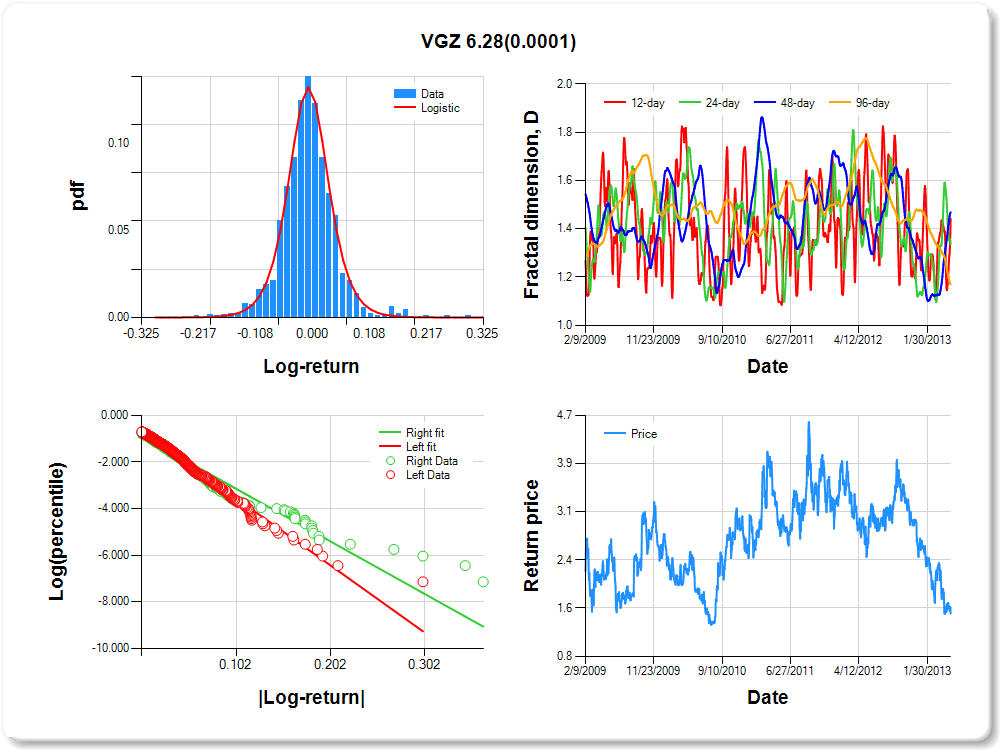

VGZ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.15 |

-0.12 |

-0.08 |

-0.05 |

-0.03 |

0.00 |

0.03 |

0.08 |

0.19 |

0.21 |

0.93 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.171 |

0.129 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.608 |

0.061 |

-9.987 |

0.0000 |

|log-return| |

-28.846 |

1.195 |

-24.133 |

0.0000 |

I(right-tail) |

-0.242 |

0.084 |

-2.890 |

0.0039 |

|log-return|*I(right-tail) |

6.282 |

1.547 |

4.060 |

0.0001 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.558 |

0.664 |

0.531 |

0.831 |

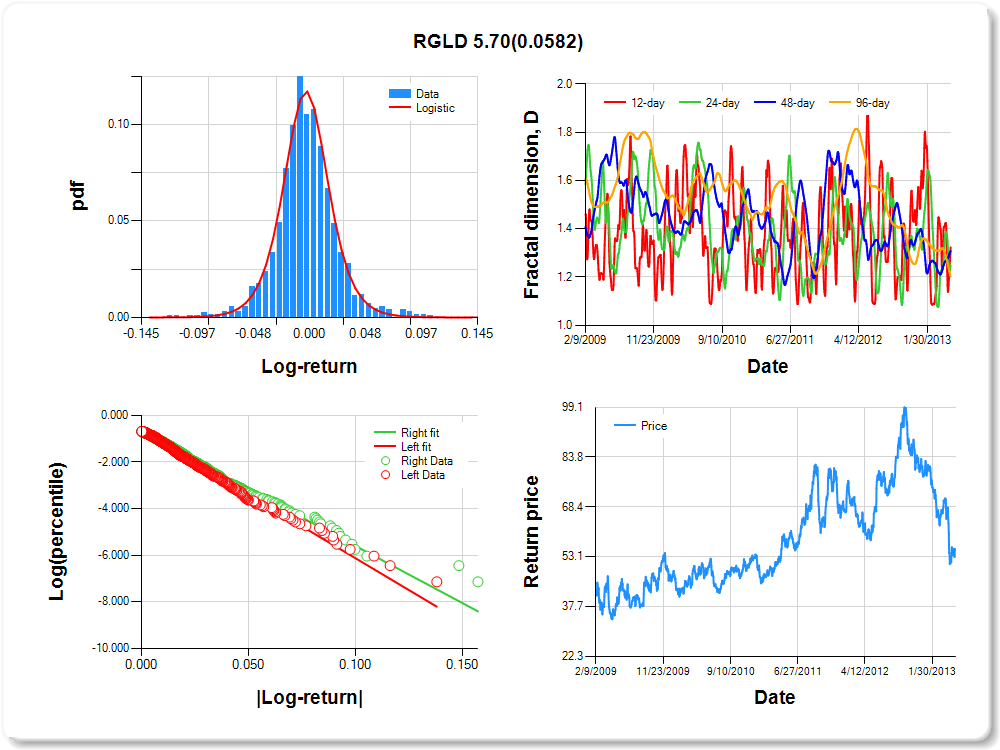

RGLD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.07 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.09 |

0.10 |

0.89 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.116 |

0.147 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.669 |

0.058 |

-11.626 |

0.0000 |

|log-return| |

-54.589 |

2.228 |

-24.498 |

0.0000 |

I(right-tail) |

-0.047 |

0.081 |

-0.576 |

0.5645 |

|log-return|*I(right-tail) |

5.700 |

3.006 |

1.896 |

0.0582 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.677 |

0.751 |

0.693 |

0.798 |

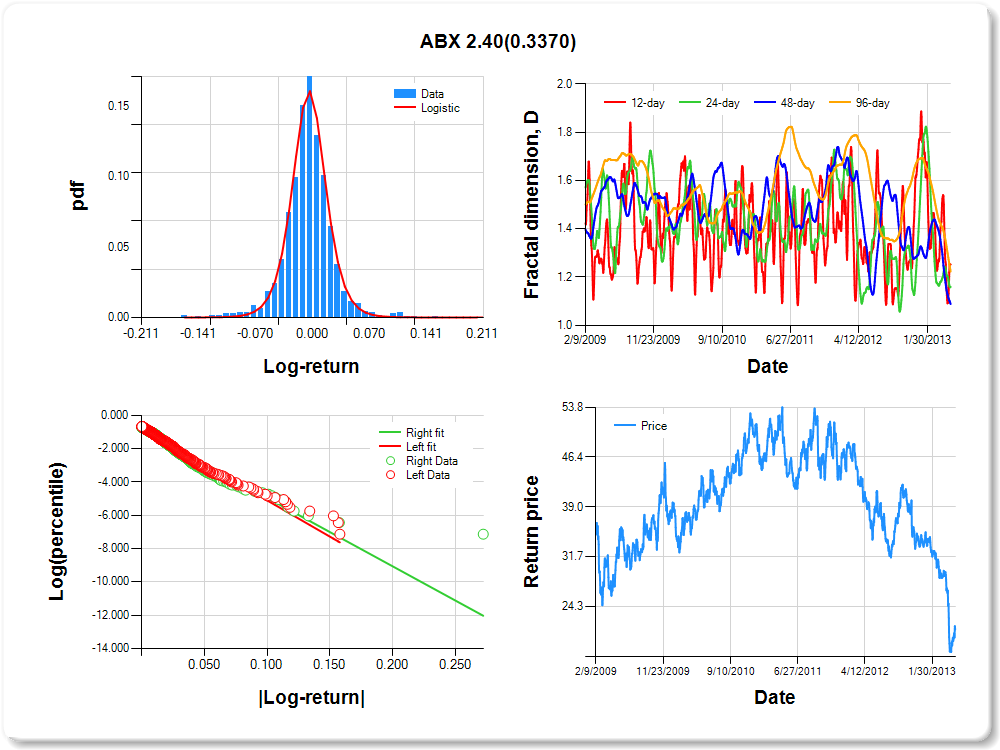

ABX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.11 |

-0.09 |

-0.05 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.09 |

0.12 |

0.64 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.455 |

0.107 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.761 |

0.054 |

-14.028 |

0.0000 |

|log-return| |

-43.447 |

1.771 |

-24.527 |

0.0000 |

I(right-tail) |

-0.086 |

0.077 |

-1.116 |

0.2644 |

|log-return|*I(right-tail) |

2.400 |

2.499 |

0.960 |

0.3370 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.748 |

0.841 |

0.912 |

0.777 |

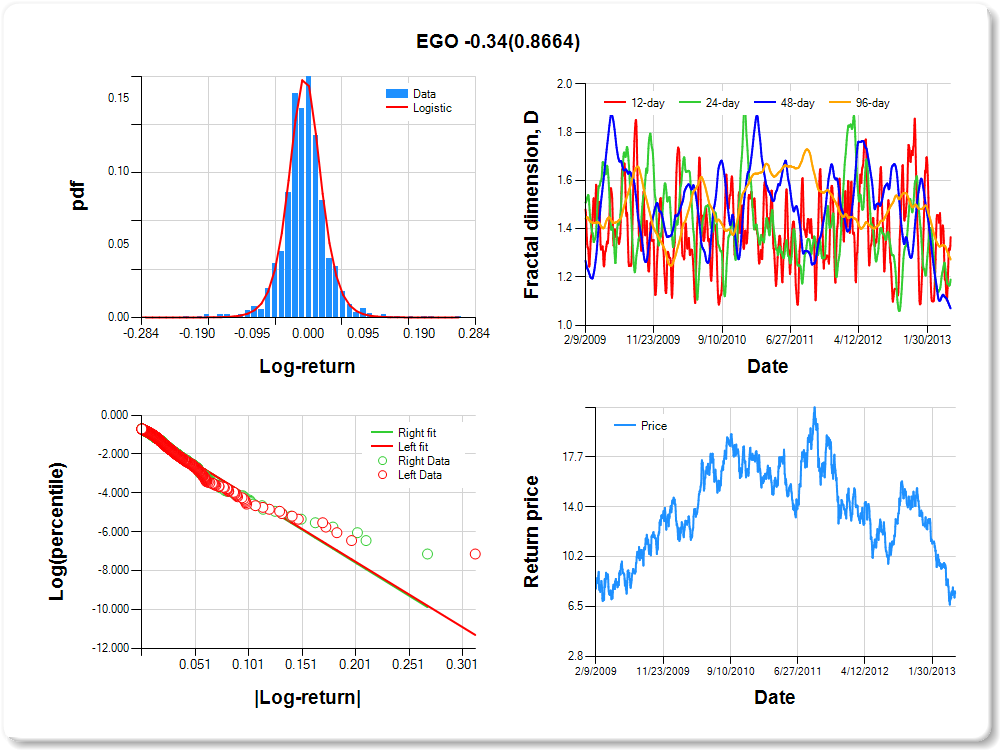

EGO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.14 |

-0.09 |

-0.05 |

-0.04 |

-0.02 |

0.00 |

0.02 |

0.06 |

0.11 |

0.15 |

0.52 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.129 |

0.104 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.790 |

0.056 |

-14.215 |

0.0000 |

|log-return| |

-33.649 |

1.425 |

-23.619 |

0.0000 |

I(right-tail) |

0.016 |

0.079 |

0.205 |

0.8373 |

|log-return|*I(right-tail) |

-0.339 |

2.012 |

-0.168 |

0.8664 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.634 |

0.810 |

0.930 |

0.727 |

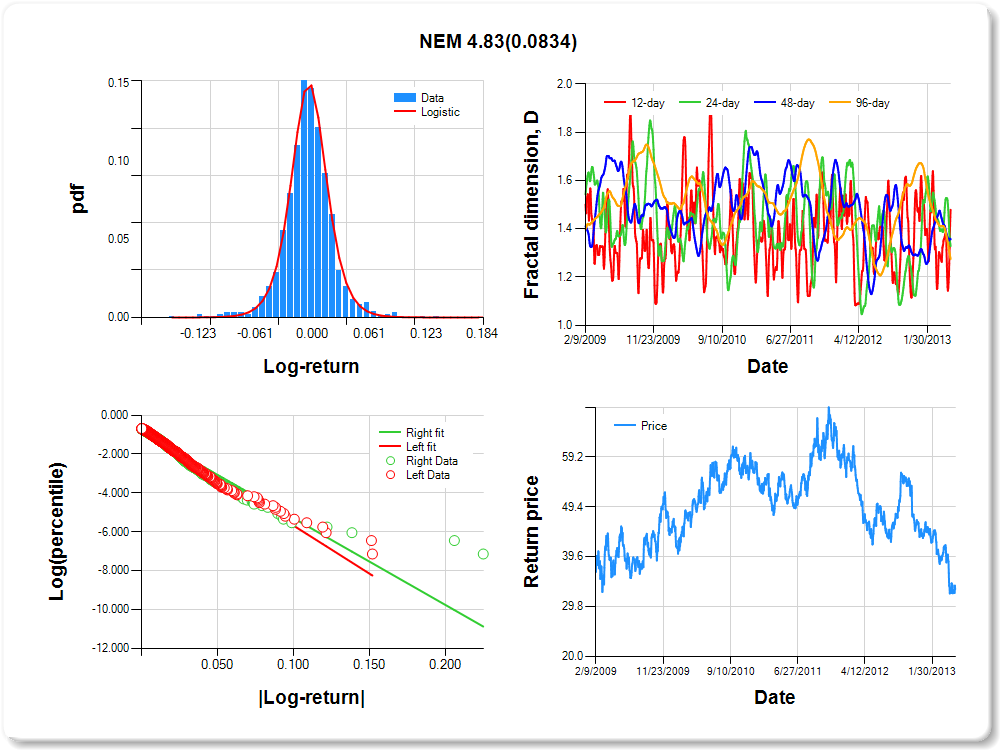

NEM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.08 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.08 |

0.10 |

0.12 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.333 |

0.114 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.736 |

0.055 |

-13.278 |

0.0000 |

|log-return| |

-49.472 |

2.028 |

-24.392 |

0.0000 |

I(right-tail) |

-0.106 |

0.078 |

-1.357 |

0.1750 |

|log-return|*I(right-tail) |

4.830 |

2.787 |

1.733 |

0.0834 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.521 |

0.671 |

0.644 |

0.725 |

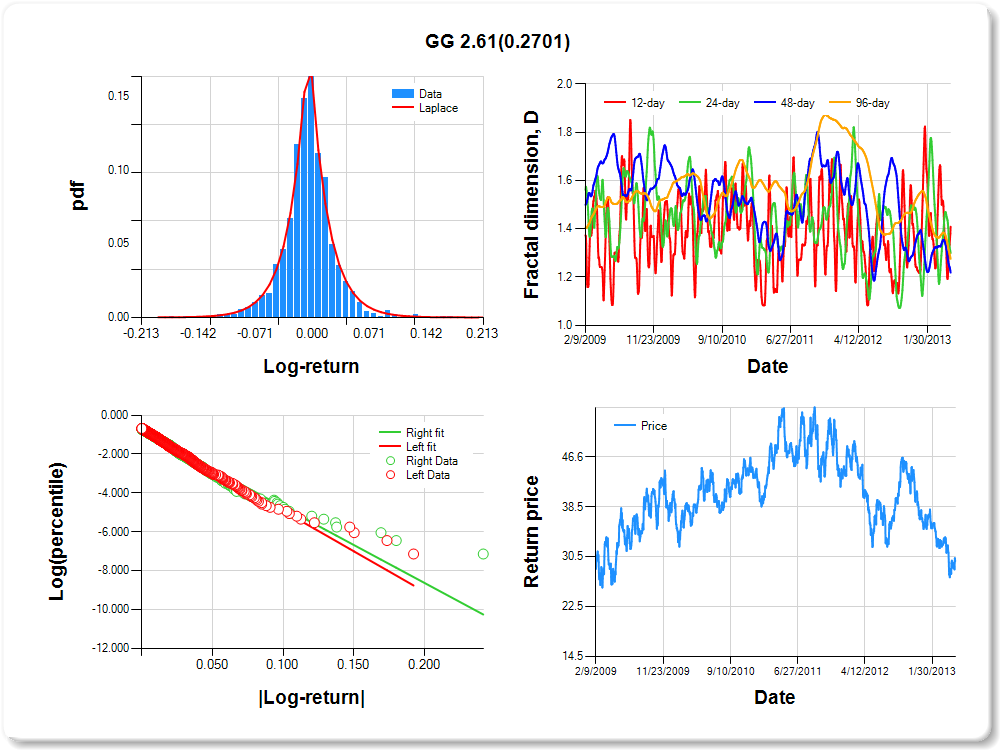

GG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.11 |

-0.08 |

-0.05 |

-0.04 |

-0.02 |

0.00 |

0.02 |

0.05 |

0.10 |

0.13 |

0.32 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.198 |

0.178 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.749 |

0.055 |

-13.668 |

0.0000 |

|log-return| |

-41.653 |

1.701 |

-24.486 |

0.0000 |

I(right-tail) |

-0.068 |

0.078 |

-0.880 |

0.3789 |

|log-return|*I(right-tail) |

2.606 |

2.362 |

1.103 |

0.2701 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.591 |

0.701 |

0.782 |

0.725 |

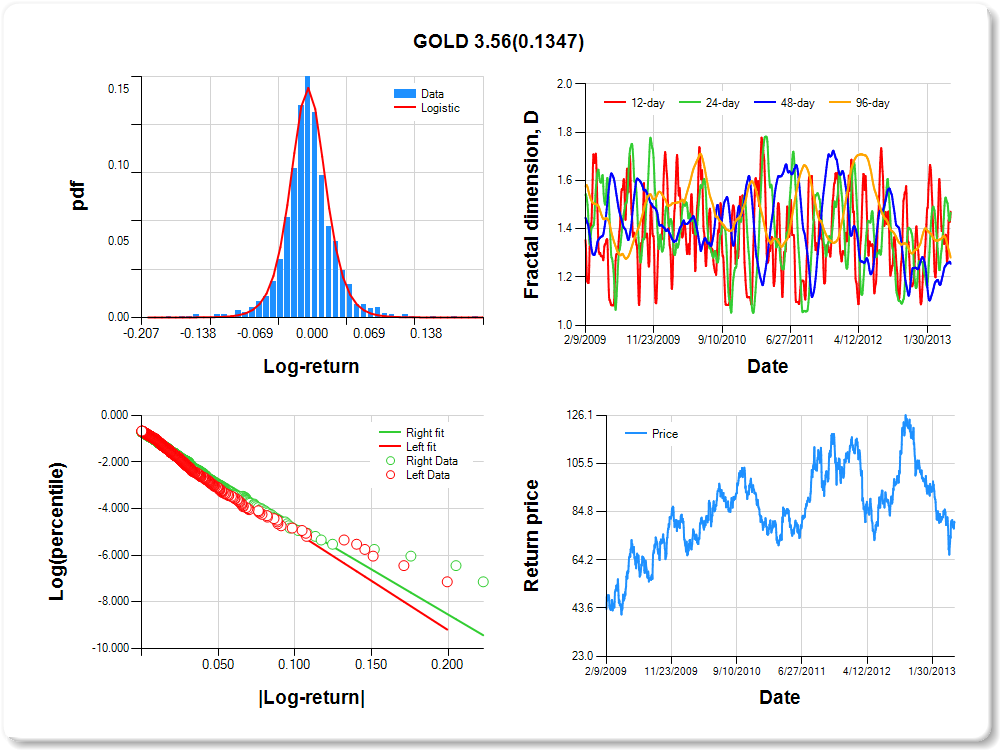

GOLD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.12 |

-0.08 |

-0.05 |

-0.03 |

-0.02 |

0.00 |

0.02 |

0.05 |

0.09 |

0.12 |

3.24 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.105 |

0.114 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.764 |

0.054 |

-14.027 |

0.0000 |

|log-return| |

-42.231 |

1.738 |

-24.305 |

0.0000 |

I(right-tail) |

-0.043 |

0.077 |

-0.552 |

0.5814 |

|log-return|*I(right-tail) |

3.556 |

2.376 |

1.497 |

0.1347 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.529 |

0.533 |

0.746 |

0.719 |

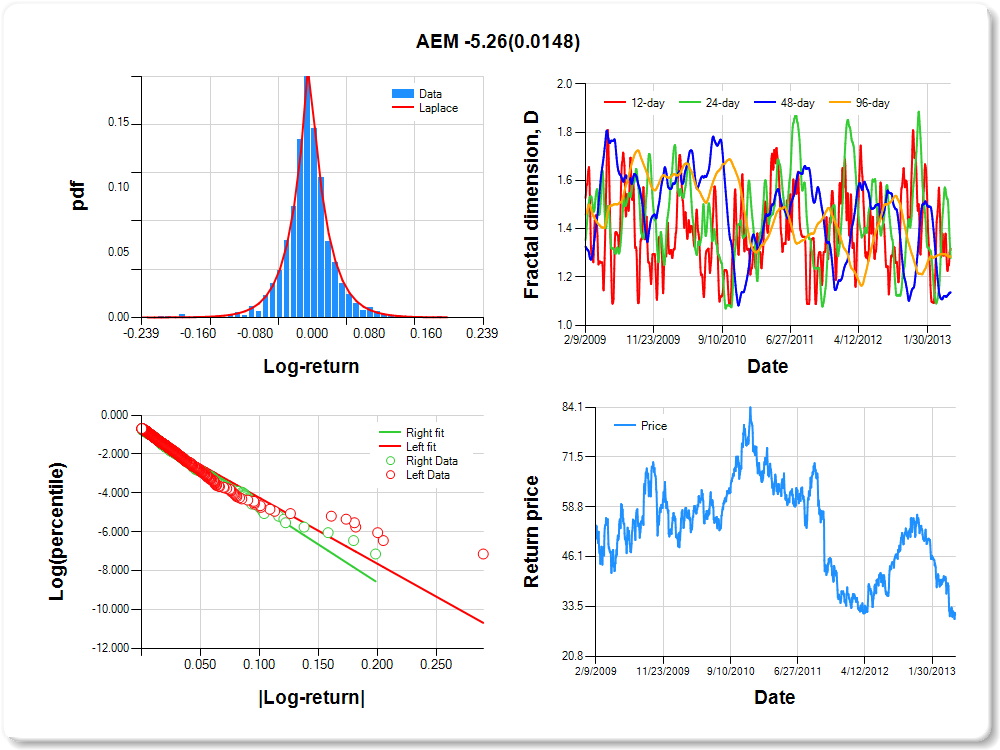

AEM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.16 |

-0.09 |

-0.05 |

-0.04 |

-0.02 |

0.00 |

0.02 |

0.05 |

0.10 |

0.12 |

0.96 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.321 |

0.167 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.866 |

0.053 |

-16.488 |

0.0000 |

|log-return| |

-33.844 |

1.429 |

-23.681 |

0.0000 |

I(right-tail) |

0.087 |

0.076 |

1.141 |

0.2541 |

|log-return|*I(right-tail) |

-5.263 |

2.156 |

-2.441 |

0.0148 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.682 |

0.721 |

0.863 |

0.715 |

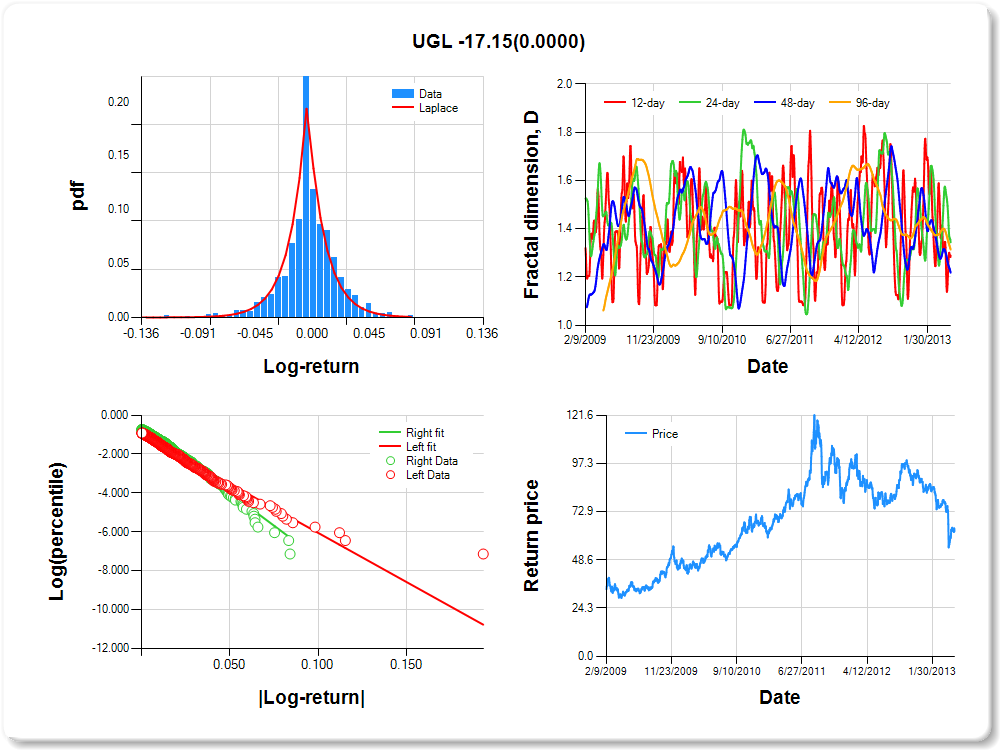

UGL

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.06 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.06 |

0.07 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.657 |

0.170 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-1.007 |

0.061 |

-16.430 |

0.0000 |

|log-return| |

-50.417 |

2.352 |

-21.433 |

0.0000 |

I(right-tail) |

0.396 |

0.087 |

4.542 |

0.0000 |

|log-return|*I(right-tail) |

-17.155 |

3.677 |

-4.666 |

0.0000 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.711 |

0.656 |

0.782 |

0.686 |

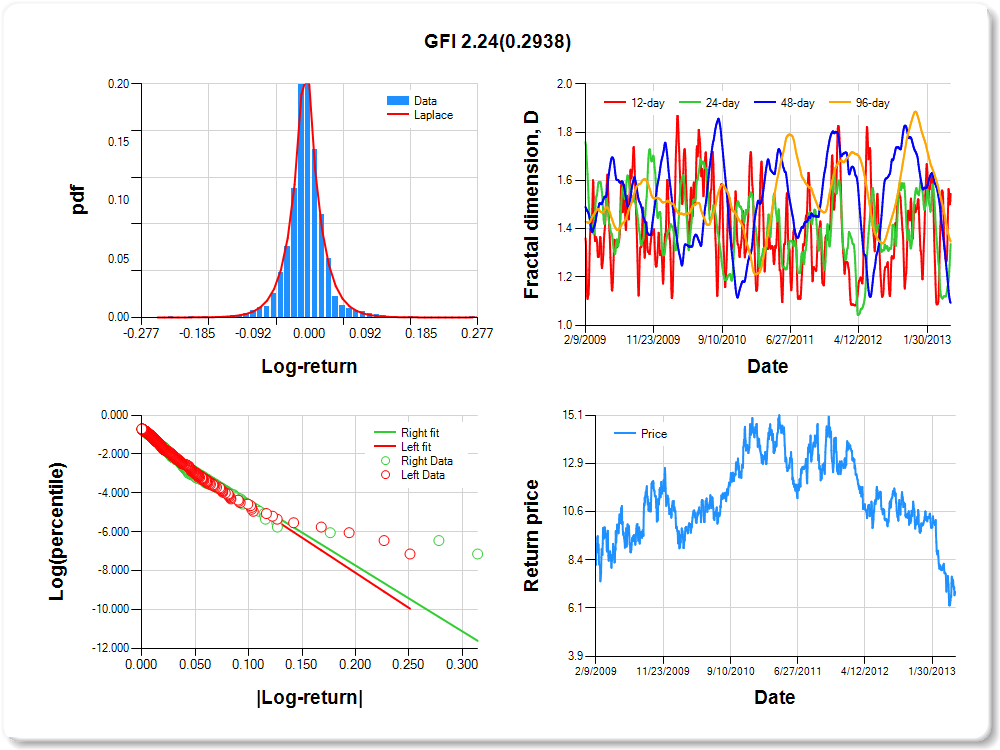

GFI

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.12 |

-0.09 |

-0.05 |

-0.03 |

-0.01 |

0.00 |

0.02 |

0.05 |

0.10 |

0.12 |

0.67 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

-0.199 |

0.133 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.866 |

0.053 |

-16.209 |

0.0000 |

|log-return| |

-36.143 |

1.529 |

-23.642 |

0.0000 |

I(right-tail) |

-0.072 |

0.075 |

-0.962 |

0.3362 |

|log-return|*I(right-tail) |

2.239 |

2.132 |

1.050 |

0.2938 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.455 |

0.663 |

0.907 |

0.653 |