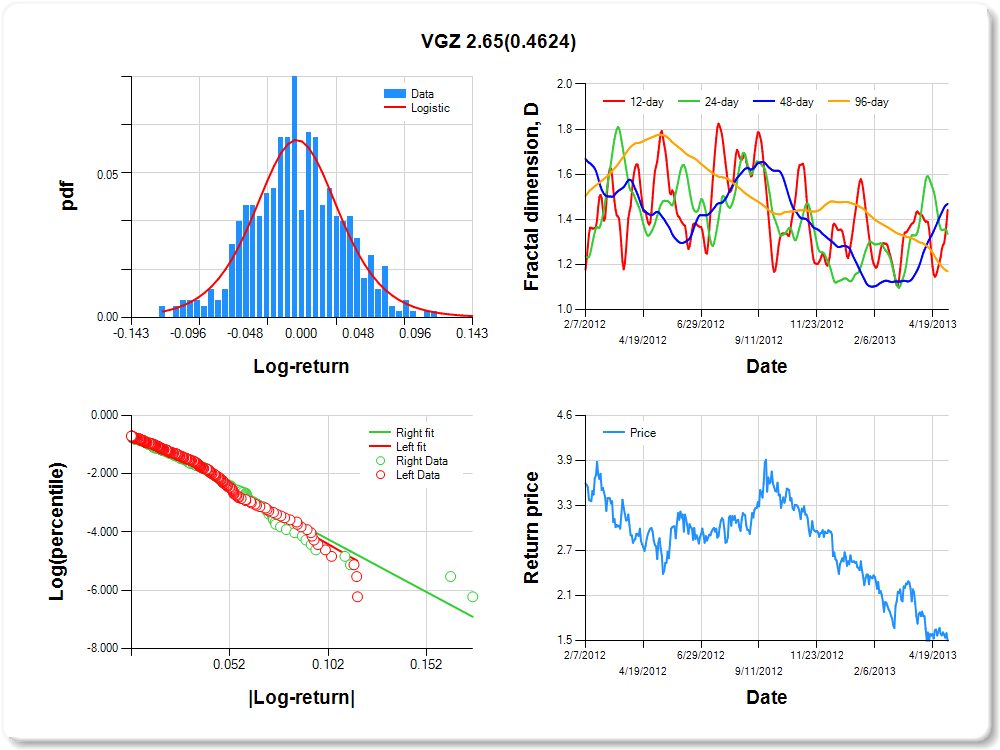

VGZ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.11 |

-0.10 |

-0.06 |

-0.05 |

-0.03 |

0.00 |

0.02 |

0.07 |

0.10 |

0.12 |

1.92 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.361 |

0.276 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.453 |

0.105 |

-4.308 |

0.0000 |

|log-return| |

-38.853 |

2.608 |

-14.895 |

0.0000 |

I(right-tail) |

-0.104 |

0.148 |

-0.702 |

0.4828 |

|log-return|*I(right-tail) |

2.651 |

3.604 |

0.735 |

0.4624 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.558 |

0.664 |

0.531 |

0.831 |

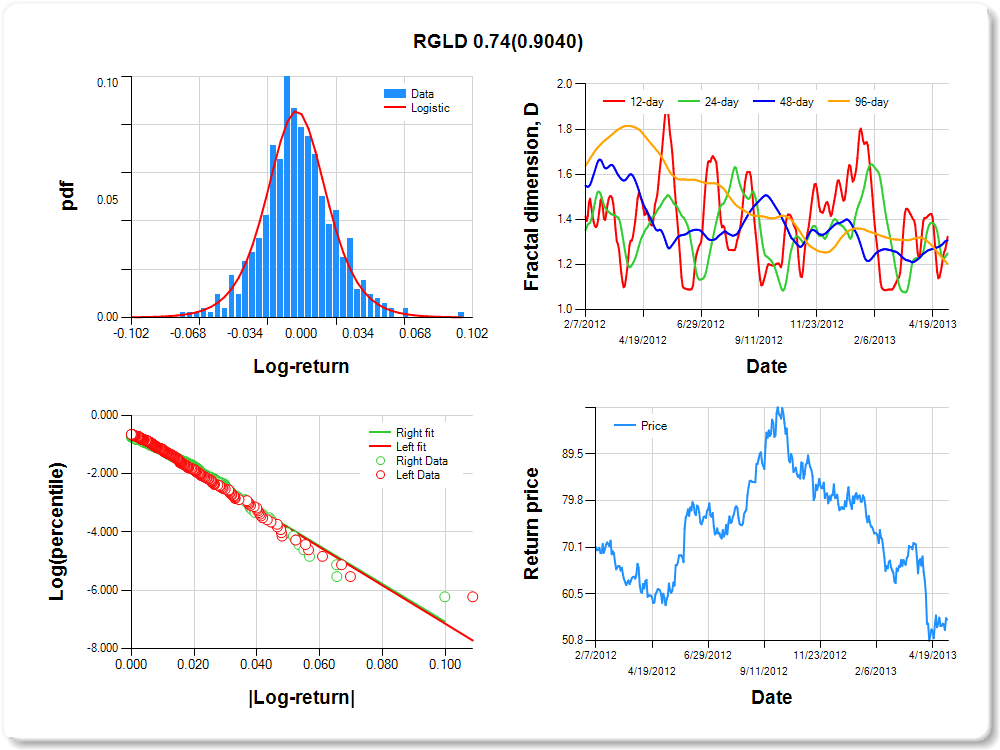

RGLD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.05 |

0.06 |

4.94 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.054 |

0.195 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.575 |

0.093 |

-6.196 |

0.0000 |

|log-return| |

-65.762 |

4.261 |

-15.432 |

0.0000 |

I(right-tail) |

-0.008 |

0.137 |

-0.060 |

0.9524 |

|log-return|*I(right-tail) |

0.740 |

6.133 |

0.121 |

0.9040 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.677 |

0.751 |

0.693 |

0.798 |

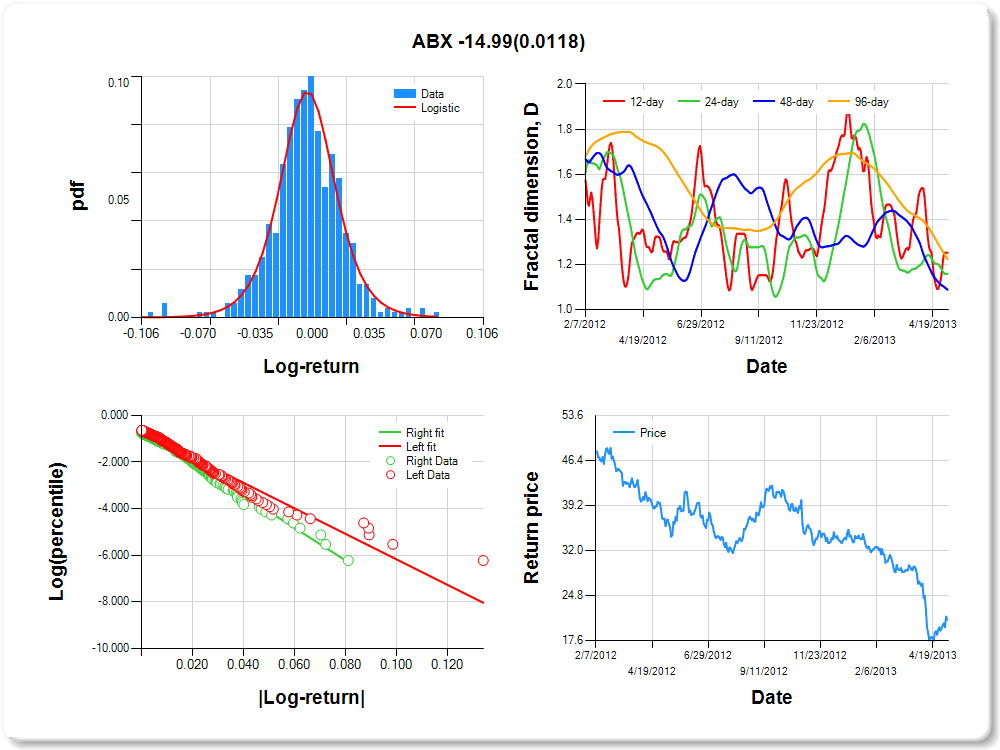

ABX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.08 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.06 |

2.52 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.406 |

0.178 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.707 |

0.086 |

-8.211 |

0.0000 |

|log-return| |

-54.646 |

3.567 |

-15.318 |

0.0000 |

I(right-tail) |

0.065 |

0.131 |

0.492 |

0.6229 |

|log-return|*I(right-tail) |

-14.990 |

5.930 |

-2.528 |

0.0118 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.748 |

0.841 |

0.912 |

0.777 |

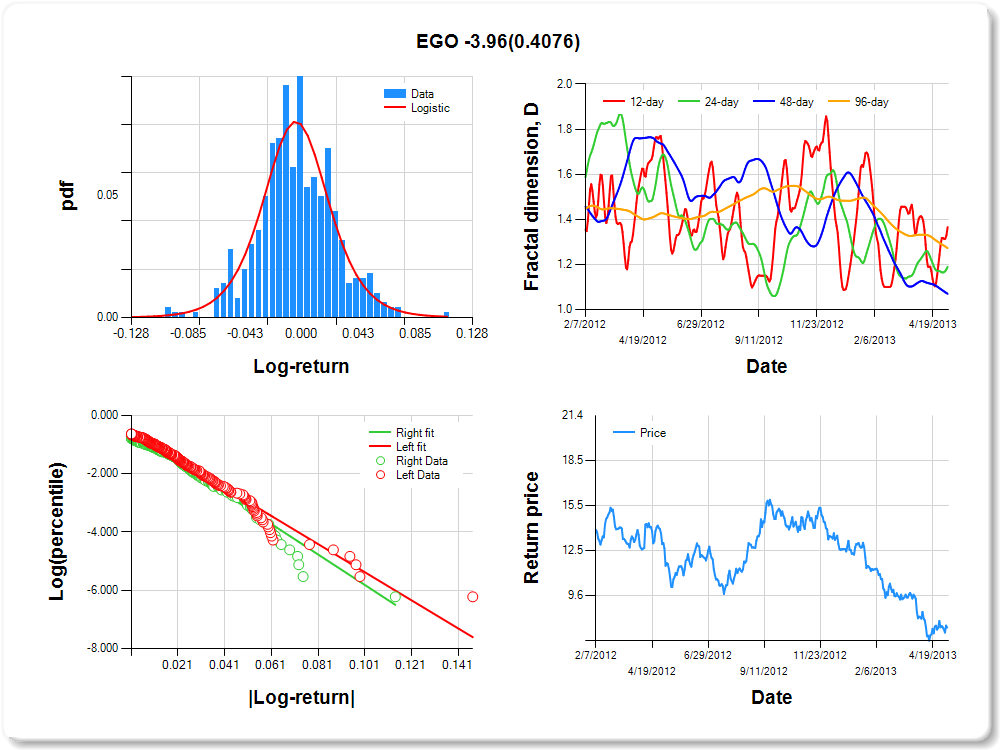

EGO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.09 |

-0.08 |

-0.05 |

-0.04 |

-0.02 |

0.00 |

0.02 |

0.05 |

0.07 |

0.07 |

1.84 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.191 |

0.213 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.535 |

0.093 |

-5.721 |

0.0000 |

|log-return| |

-48.202 |

3.109 |

-15.502 |

0.0000 |

I(right-tail) |

-0.037 |

0.141 |

-0.264 |

0.7920 |

|log-return|*I(right-tail) |

-3.965 |

4.784 |

-0.829 |

0.4076 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.634 |

0.810 |

0.930 |

0.727 |

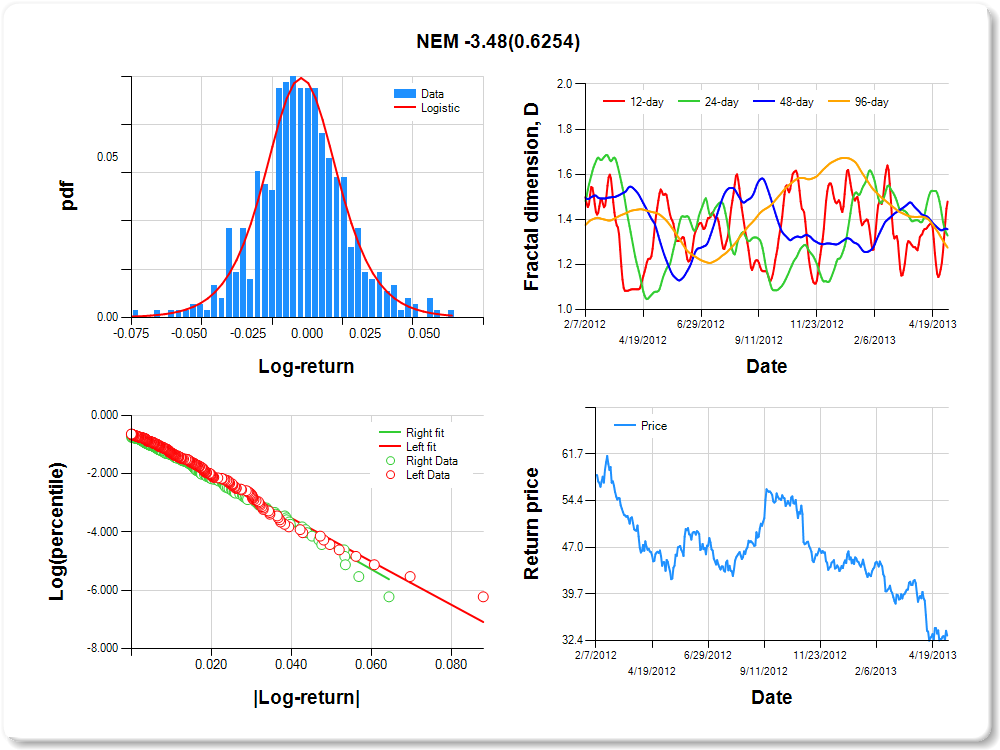

NEM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

2.80 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.241 |

0.230 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.549 |

0.093 |

-5.918 |

0.0000 |

|log-return| |

-74.352 |

4.778 |

-15.562 |

0.0000 |

I(right-tail) |

-0.058 |

0.137 |

-0.421 |

0.6736 |

|log-return|*I(right-tail) |

-3.485 |

7.134 |

-0.488 |

0.6254 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.521 |

0.671 |

0.644 |

0.725 |

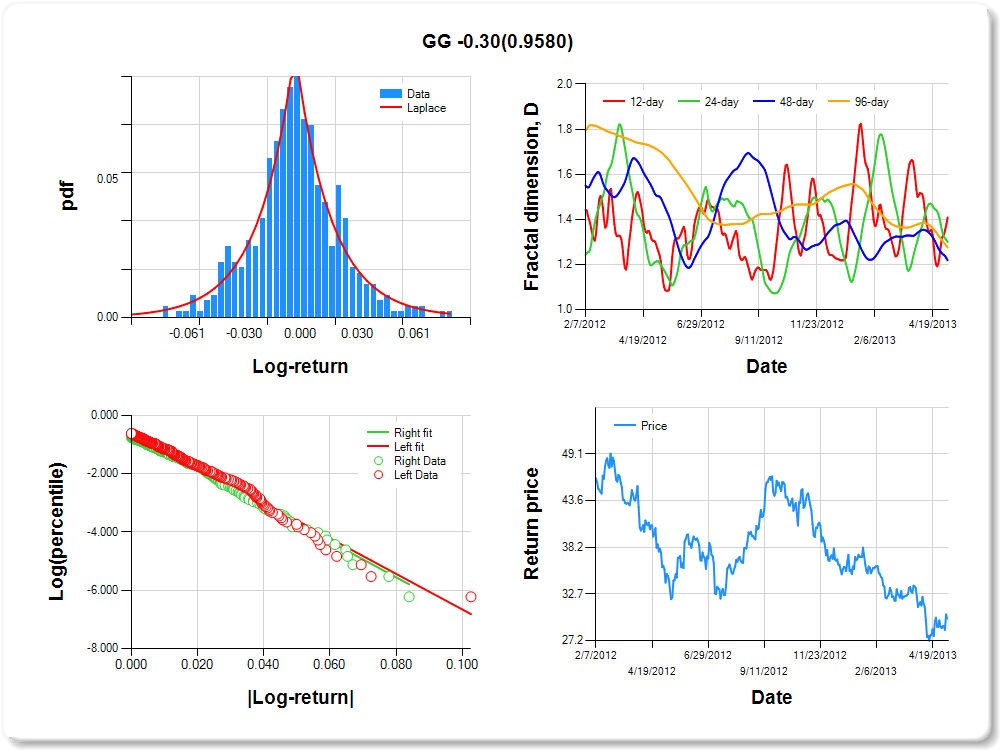

GG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.06 |

0.07 |

3.32 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.144 |

0.358 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.550 |

0.091 |

-6.040 |

0.0000 |

|log-return| |

-61.069 |

3.892 |

-15.691 |

0.0000 |

I(right-tail) |

-0.094 |

0.136 |

-0.691 |

0.4899 |

|log-return|*I(right-tail) |

-0.302 |

5.731 |

-0.053 |

0.9580 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.591 |

0.701 |

0.782 |

0.725 |

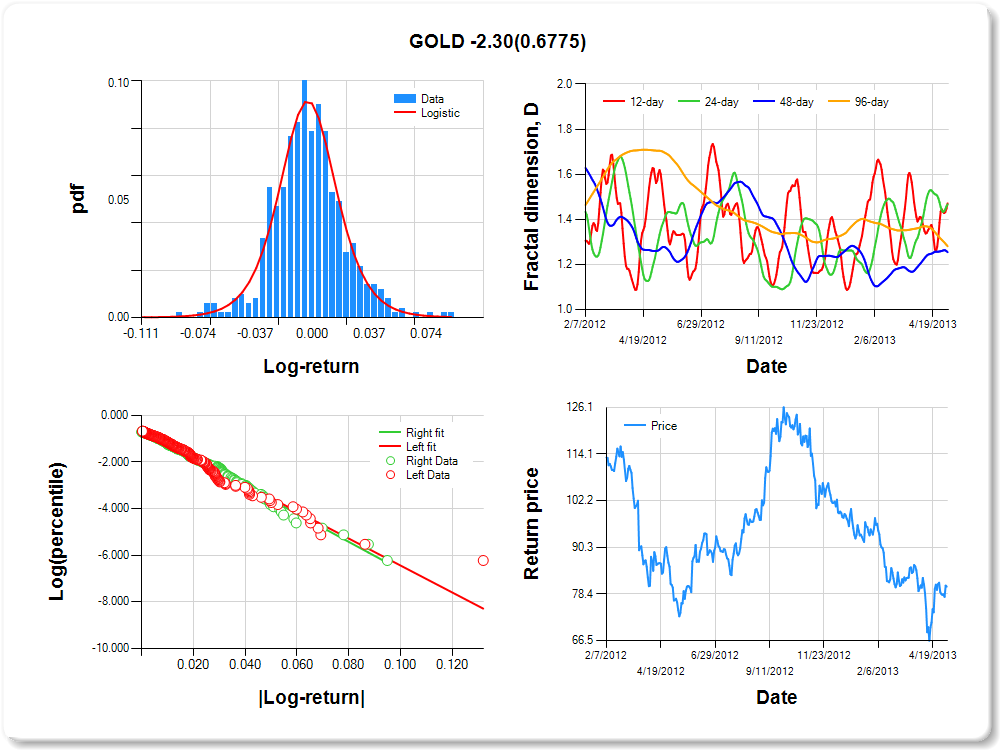

GOLD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.06 |

0.07 |

4.84 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.268 |

0.185 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.656 |

0.092 |

-7.162 |

0.0000 |

|log-return| |

-57.783 |

3.832 |

-15.080 |

0.0000 |

I(right-tail) |

0.042 |

0.133 |

0.315 |

0.7525 |

|log-return|*I(right-tail) |

-2.302 |

5.533 |

-0.416 |

0.6775 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.529 |

0.533 |

0.746 |

0.719 |

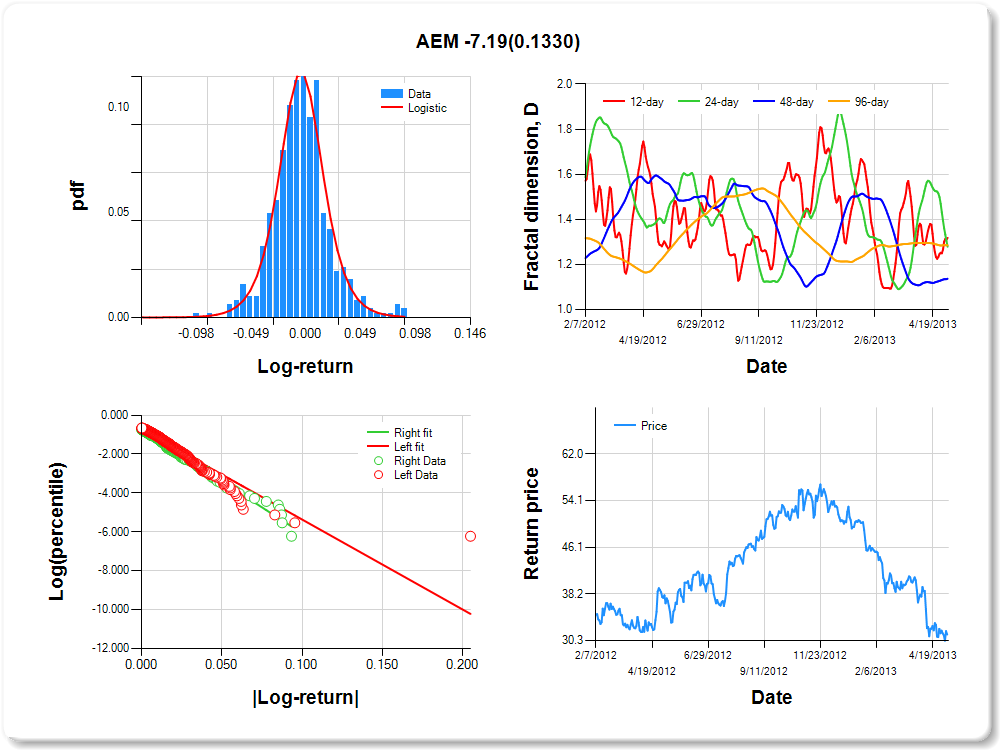

AEM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.08 |

-0.06 |

-0.04 |

-0.03 |

-0.02 |

0.00 |

0.01 |

0.04 |

0.08 |

0.09 |

2.78 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.624 |

0.147 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.734 |

0.088 |

-8.389 |

0.0000 |

|log-return| |

-46.240 |

3.151 |

-14.675 |

0.0000 |

I(right-tail) |

0.009 |

0.127 |

0.070 |

0.9443 |

|log-return|*I(right-tail) |

-7.192 |

4.779 |

-1.505 |

0.1330 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.682 |

0.721 |

0.863 |

0.715 |

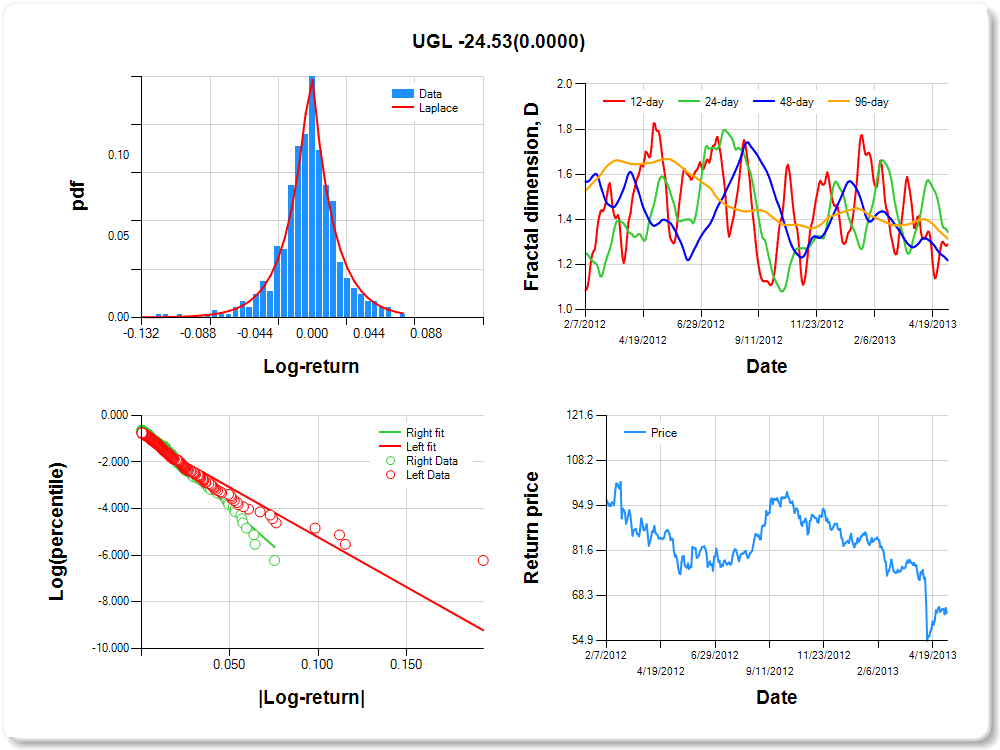

UGL

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.11 |

-0.07 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.06 |

0.06 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.771 |

0.218 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.967 |

0.085 |

-11.339 |

0.0000 |

|log-return| |

-42.607 |

3.028 |

-14.071 |

0.0000 |

I(right-tail) |

0.376 |

0.124 |

3.027 |

0.0026 |

|log-return|*I(right-tail) |

-24.527 |

5.260 |

-4.663 |

0.0000 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.711 |

0.656 |

0.782 |

0.686 |

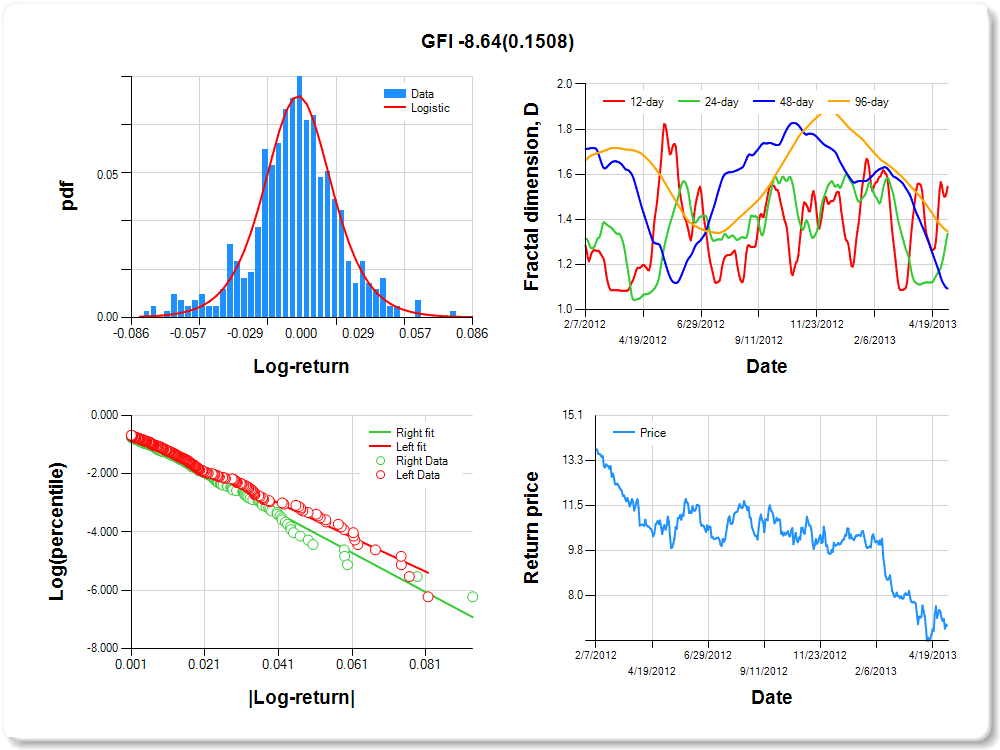

GFI

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.05 |

0.06 |

1.96 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.123 |

0.219 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.627 |

0.093 |

-6.758 |

0.0000 |

|log-return| |

-58.764 |

3.851 |

-15.261 |

0.0000 |

I(right-tail) |

-0.005 |

0.137 |

-0.034 |

0.9729 |

|log-return|*I(right-tail) |

-8.641 |

6.005 |

-1.439 |

0.1508 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.455 |

0.663 |

0.907 |

0.653 |