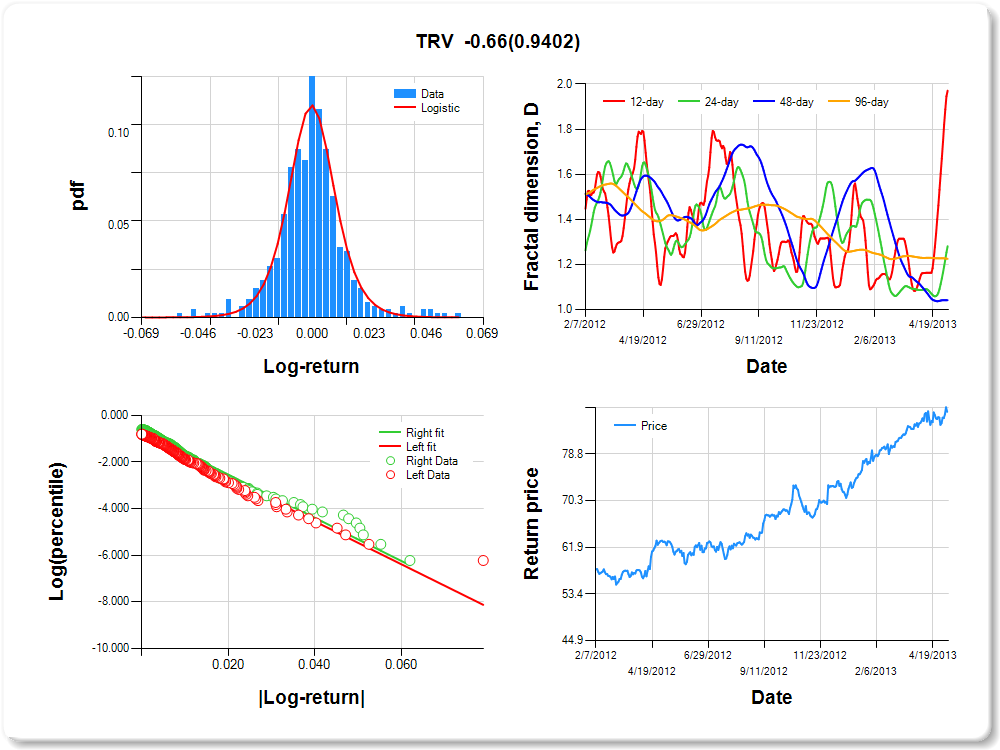

TRV

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.05 |

0.05 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.232 |

0.149 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.869 |

0.093 |

-9.290 |

0.0000 |

|log-return| |

-91.875 |

6.504 |

-14.126 |

0.0000 |

I(right-tail) |

0.180 |

0.125 |

1.438 |

0.1510 |

|log-return|*I(right-tail) |

-0.658 |

8.767 |

-0.075 |

0.9402 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.029 |

0.719 |

0.958 |

0.775 |

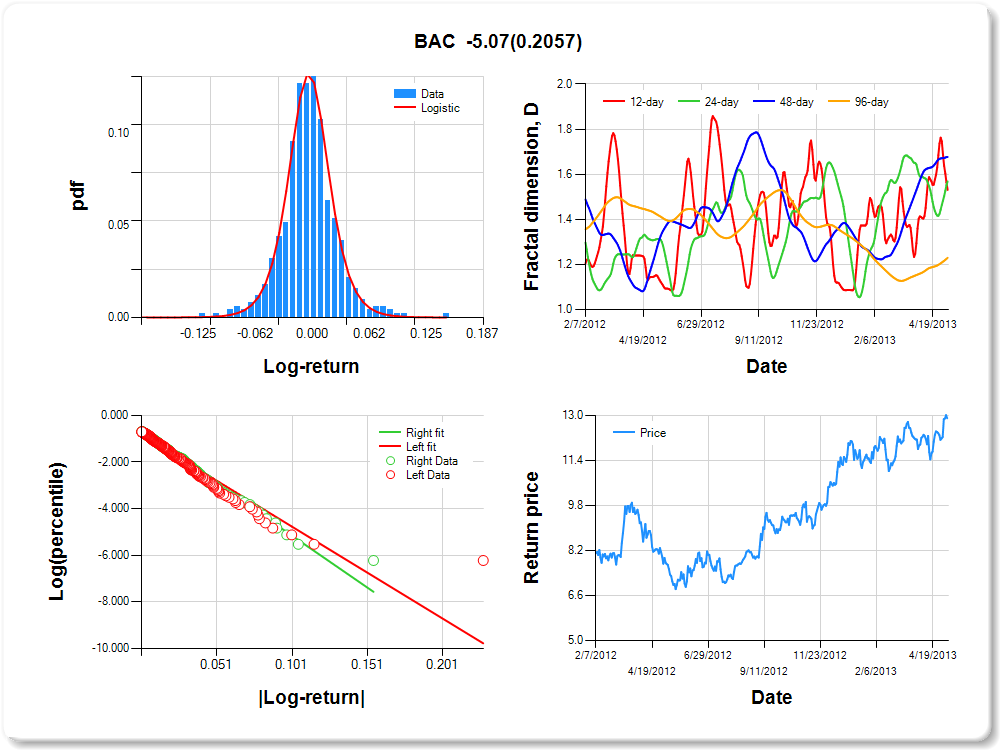

BAC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.10 |

-0.08 |

-0.05 |

-0.03 |

-0.02 |

0.00 |

0.02 |

0.05 |

0.09 |

0.09 |

2.18 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.325 |

0.130 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.820 |

0.088 |

-9.362 |

0.0000 |

|log-return| |

-39.331 |

2.717 |

-14.477 |

0.0000 |

I(right-tail) |

0.124 |

0.126 |

0.979 |

0.3282 |

|log-return|*I(right-tail) |

-5.072 |

4.003 |

-1.267 |

0.2057 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.469 |

0.432 |

0.323 |

0.770 |

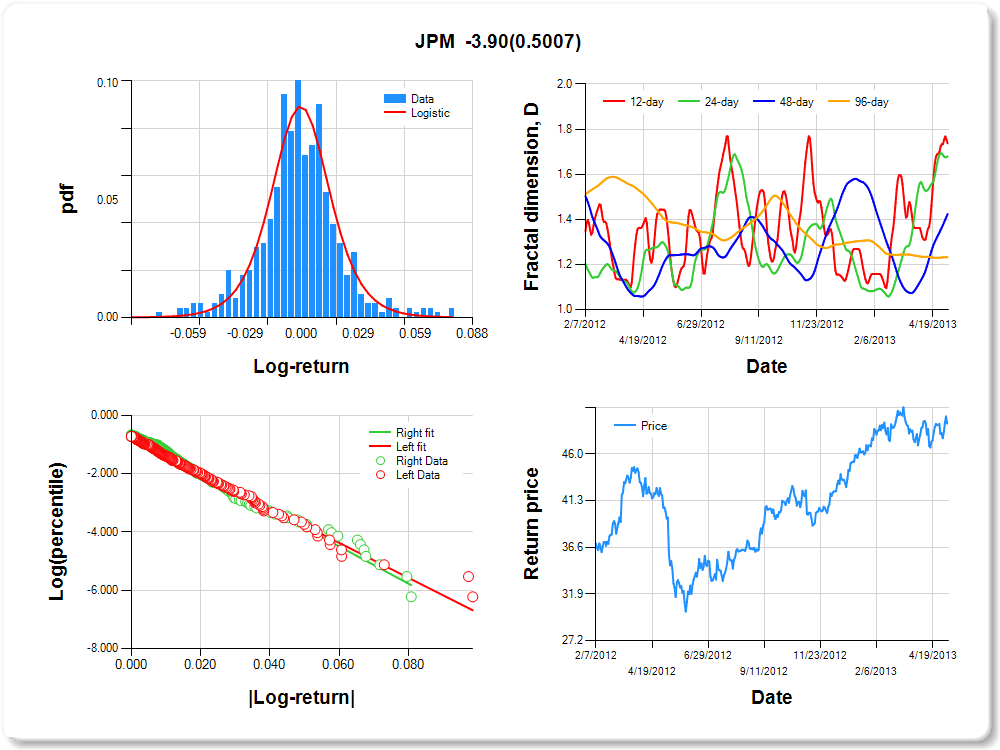

JPM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.06 |

-0.04 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.07 |

0.07 |

0.66 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.190 |

0.190 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.767 |

0.090 |

-8.533 |

0.0000 |

|log-return| |

-59.957 |

4.016 |

-14.928 |

0.0000 |

I(right-tail) |

0.113 |

0.128 |

0.882 |

0.3782 |

|log-return|*I(right-tail) |

-3.905 |

5.795 |

-0.674 |

0.5007 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.263 |

0.321 |

0.576 |

0.767 |

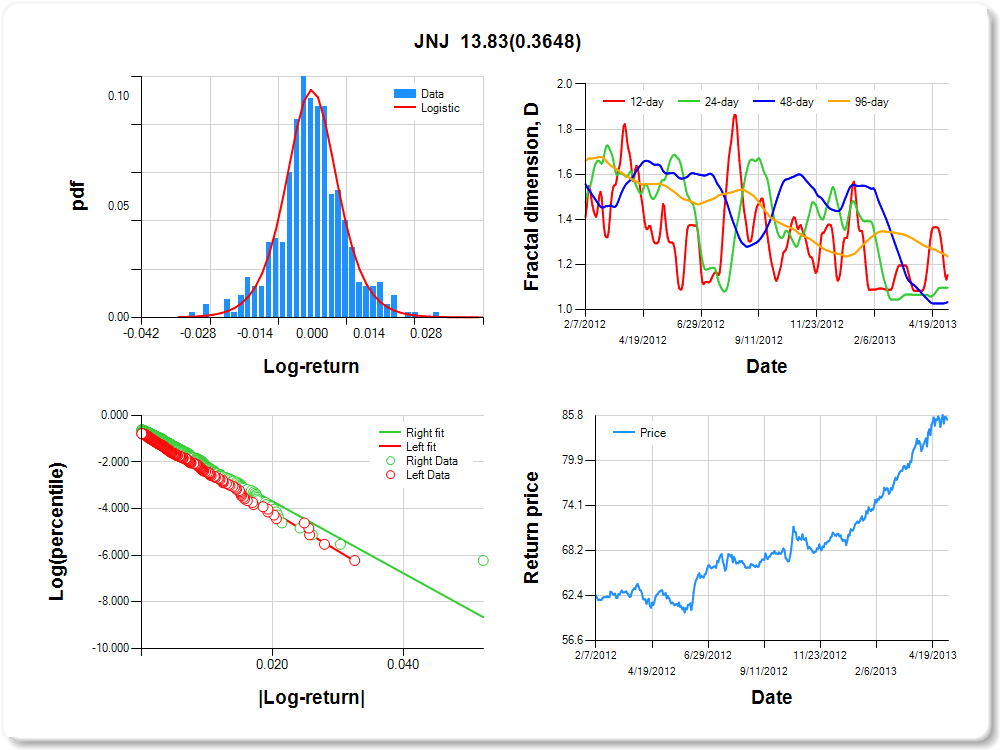

JNJ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

0.02 |

3.33 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.370 |

0.167 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.764 |

0.096 |

-7.963 |

0.0000 |

|log-return| |

-167.829 |

11.584 |

-14.488 |

0.0000 |

I(right-tail) |

0.170 |

0.131 |

1.300 |

0.1942 |

|log-return|*I(right-tail) |

13.826 |

15.243 |

0.907 |

0.3648 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.847 |

0.903 |

0.967 |

0.764 |

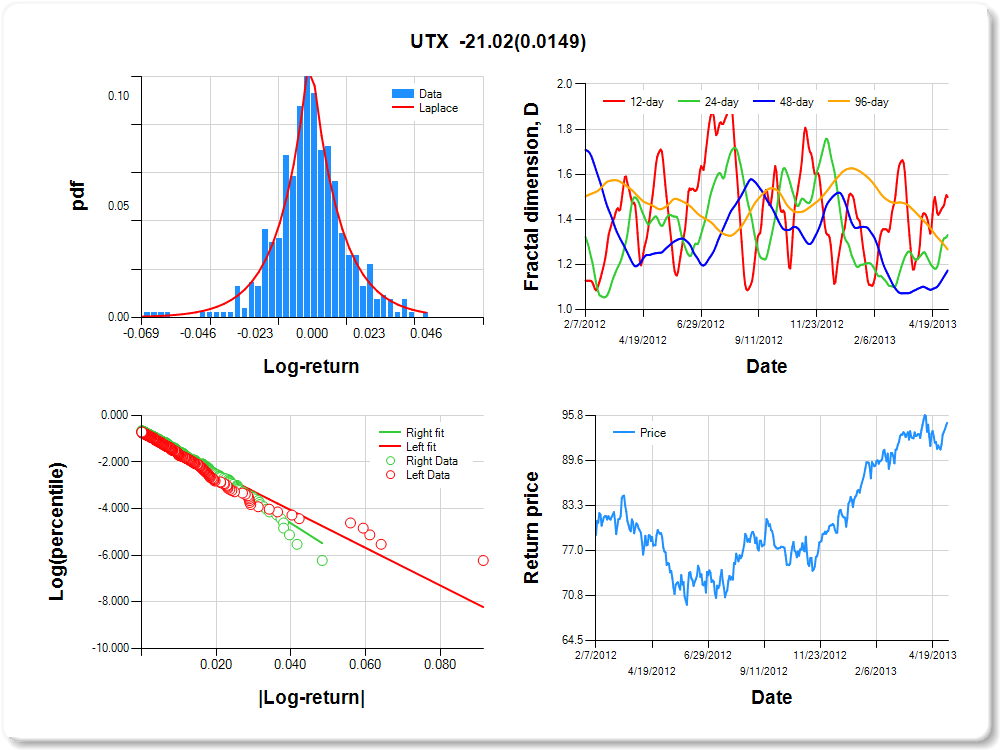

UTX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

2.38 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.539 |

0.283 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.845 |

0.087 |

-9.740 |

0.0000 |

|log-return| |

-80.558 |

5.512 |

-14.614 |

0.0000 |

I(right-tail) |

0.282 |

0.128 |

2.201 |

0.0282 |

|log-return|*I(right-tail) |

-21.025 |

8.607 |

-2.443 |

0.0149 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.501 |

0.669 |

0.827 |

0.733 |

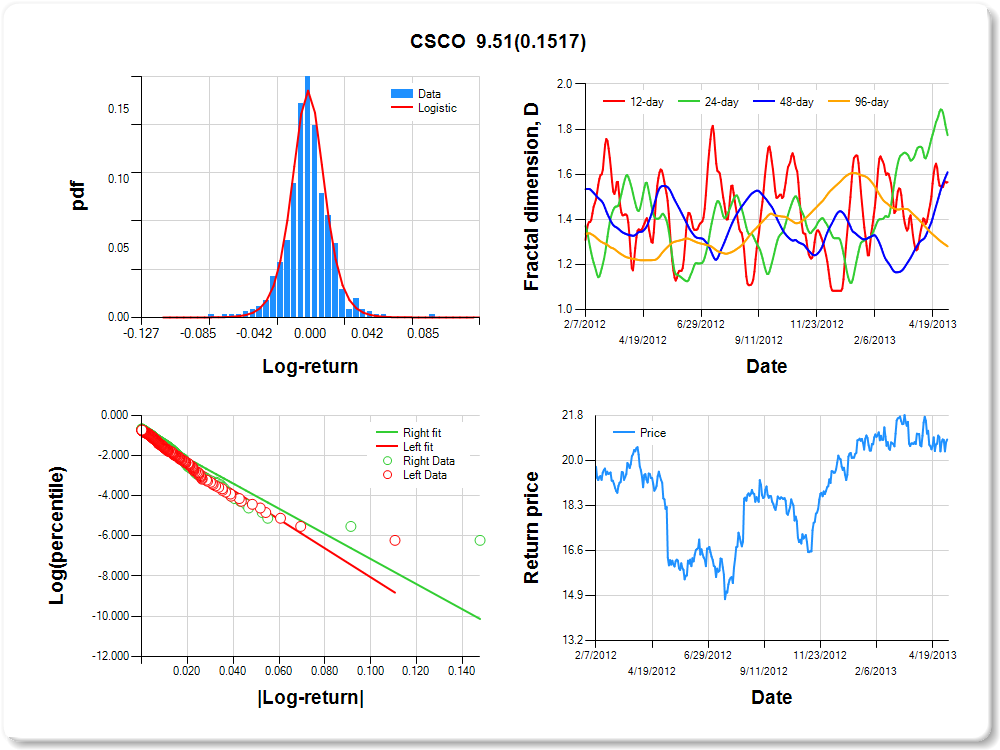

CSCO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

2.49 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.239 |

0.105 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.835 |

0.089 |

-9.408 |

0.0000 |

|log-return| |

-72.008 |

4.958 |

-14.523 |

0.0000 |

I(right-tail) |

-0.042 |

0.122 |

-0.345 |

0.7299 |

|log-return|*I(right-tail) |

9.505 |

6.620 |

1.436 |

0.1517 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.435 |

0.226 |

0.391 |

0.719 |

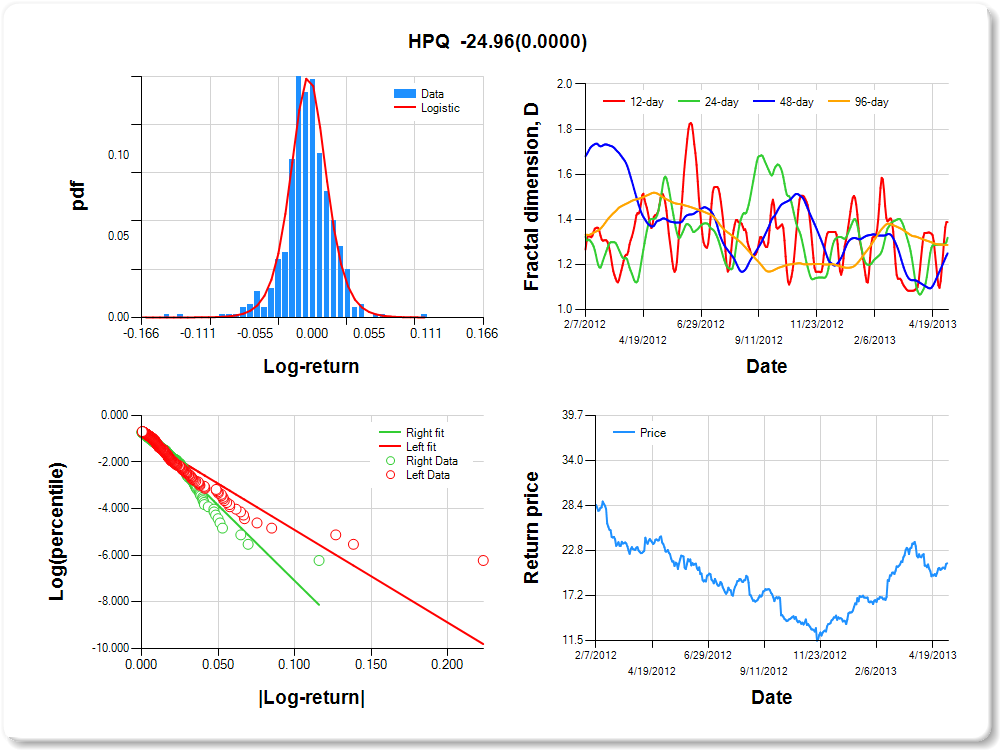

HPQ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.12 |

-0.07 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.04 |

0.05 |

0.05 |

1.85 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.537 |

0.116 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.946 |

0.082 |

-11.515 |

0.0000 |

|log-return| |

-39.704 |

2.821 |

-14.076 |

0.0000 |

I(right-tail) |

0.321 |

0.128 |

2.516 |

0.0122 |

|log-return|*I(right-tail) |

-24.964 |

5.225 |

-4.777 |

0.0000 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.612 |

0.681 |

0.750 |

0.713 |

MMM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.05 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

1.73 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.157 |

0.174 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.914 |

0.086 |

-10.623 |

0.0000 |

|log-return| |

-85.041 |

5.837 |

-14.569 |

0.0000 |

I(right-tail) |

0.338 |

0.126 |

2.668 |

0.0079 |

|log-return|*I(right-tail) |

-25.425 |

9.233 |

-2.754 |

0.0061 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.226 |

0.591 |

0.862 |

0.712 |

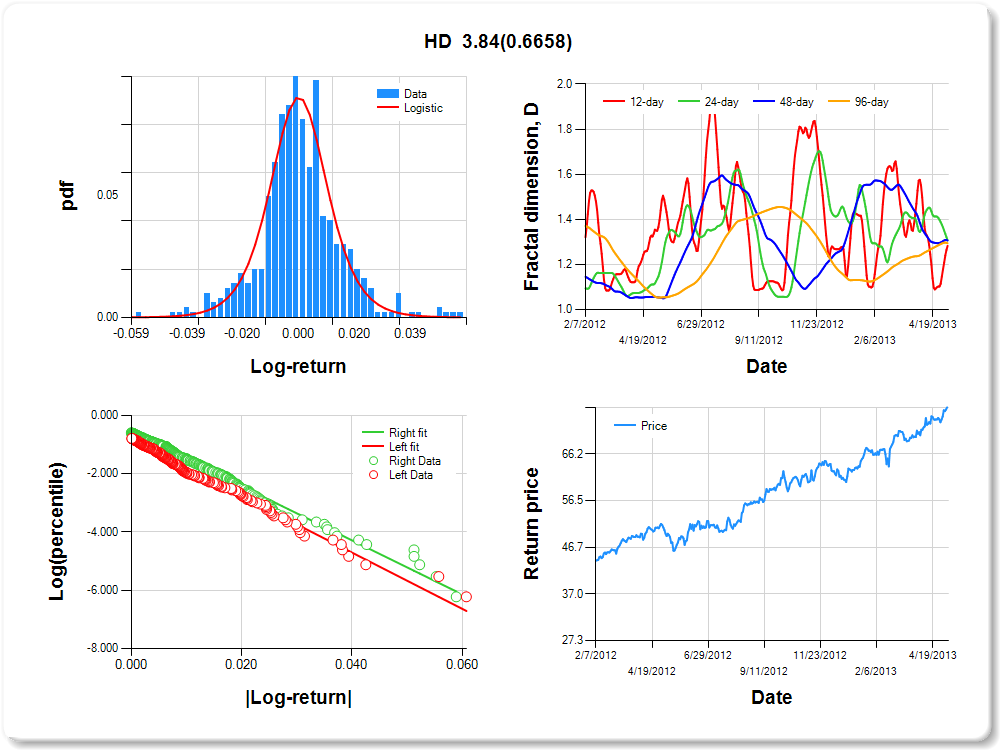

HD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

2.06 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.060 |

0.190 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.836 |

0.093 |

-8.950 |

0.0000 |

|log-return| |

-96.575 |

6.719 |

-14.373 |

0.0000 |

I(right-tail) |

0.264 |

0.128 |

2.060 |

0.0399 |

|log-return|*I(right-tail) |

3.844 |

8.896 |

0.432 |

0.6658 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.717 |

0.693 |

0.694 |

0.706 |

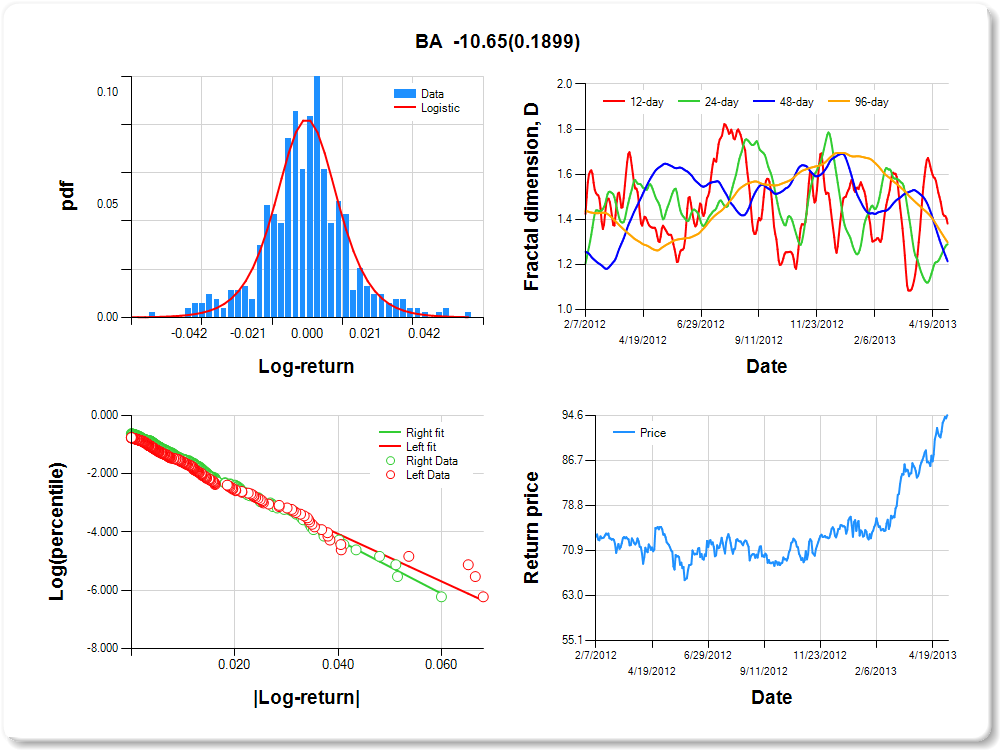

BA

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.05 |

2.21 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.137 |

0.195 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.804 |

0.092 |

-8.719 |

0.0000 |

|log-return| |

-81.535 |

5.601 |

-14.557 |

0.0000 |

I(right-tail) |

0.220 |

0.129 |

1.707 |

0.0884 |

|log-return|*I(right-tail) |

-10.647 |

8.112 |

-1.313 |

0.1899 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.619 |

0.710 |

0.786 |

0.702 |

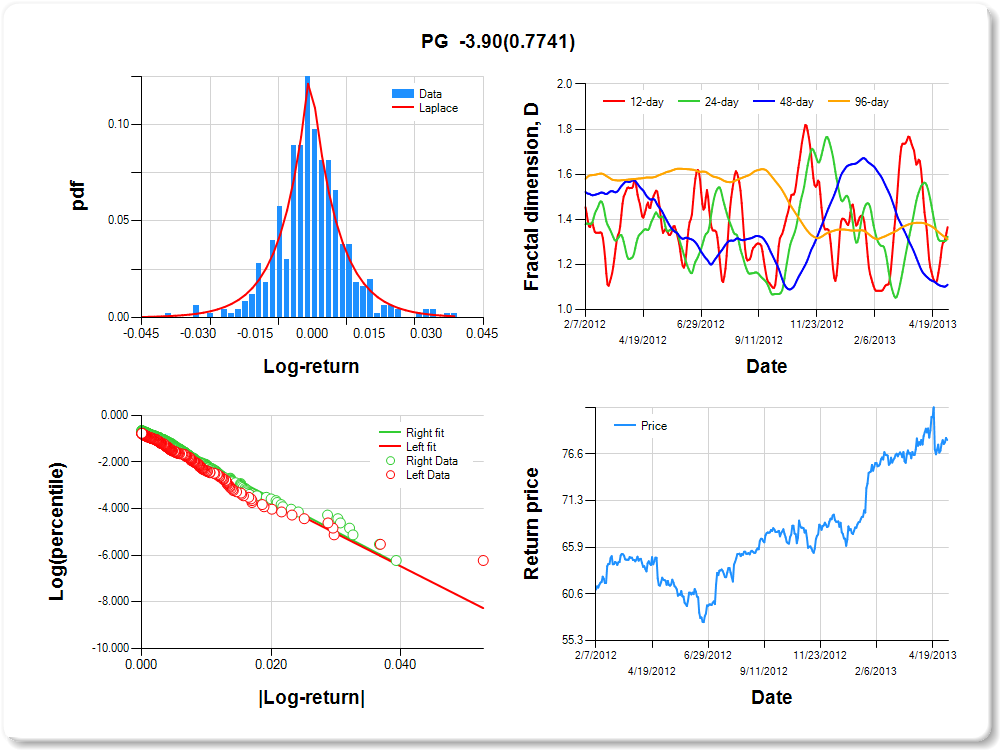

PG

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.03 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

1.59 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.260 |

0.264 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.827 |

0.092 |

-8.952 |

0.0000 |

|log-return| |

-140.852 |

9.832 |

-14.326 |

0.0000 |

I(right-tail) |

0.200 |

0.129 |

1.546 |

0.1226 |

|log-return|*I(right-tail) |

-3.900 |

13.582 |

-0.287 |

0.7741 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.634 |

0.677 |

0.890 |

0.687 |

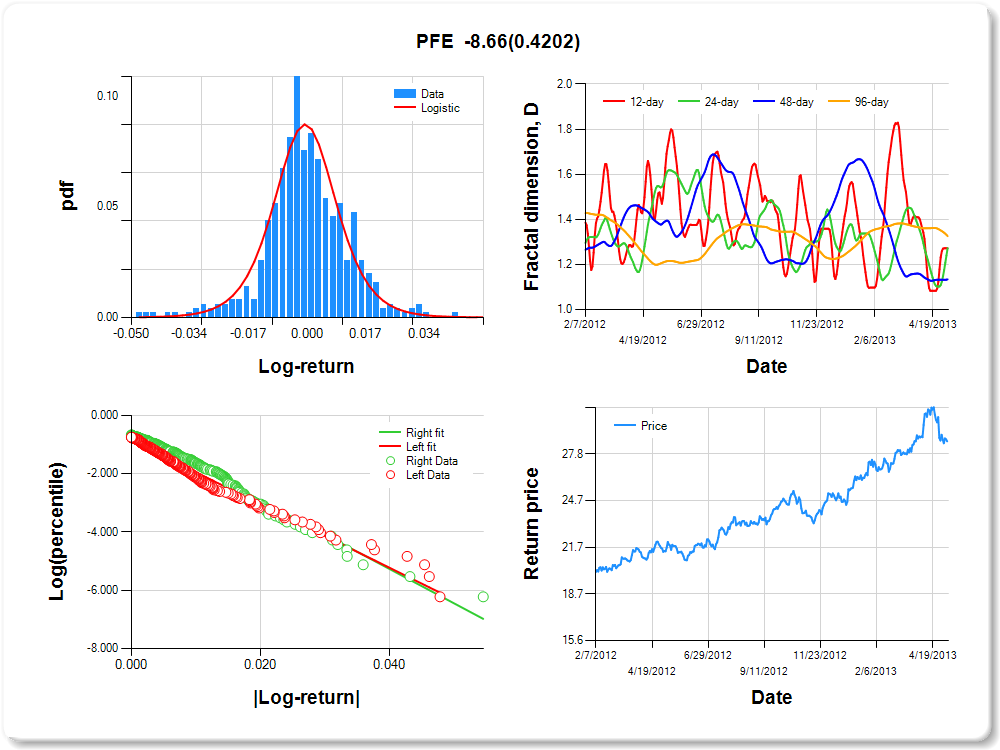

PFE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

2.26 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.098 |

0.197 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.825 |

0.090 |

-9.163 |

0.0000 |

|log-return| |

-109.227 |

7.472 |

-14.618 |

0.0000 |

I(right-tail) |

0.307 |

0.133 |

2.316 |

0.0210 |

|log-return|*I(right-tail) |

-8.665 |

10.741 |

-0.807 |

0.4202 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.728 |

0.727 |

0.866 |

0.674 |

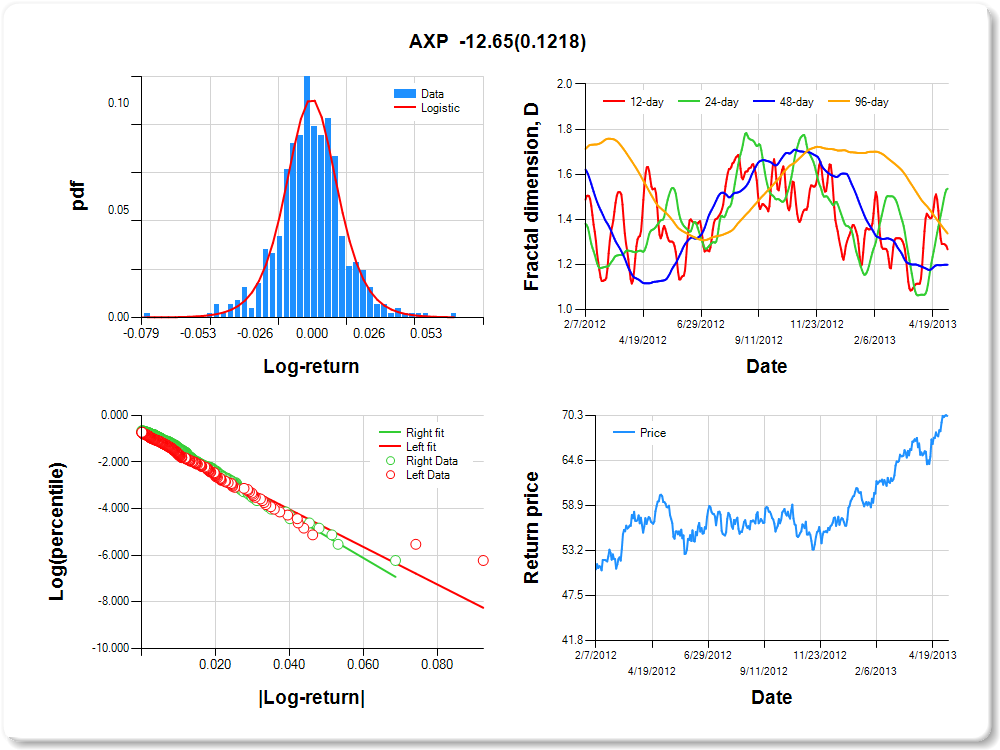

AXP

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.05 |

3.73 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.277 |

0.168 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.814 |

0.089 |

-9.183 |

0.0000 |

|log-return| |

-80.422 |

5.482 |

-14.669 |

0.0000 |

I(right-tail) |

0.285 |

0.131 |

2.183 |

0.0295 |

|log-return|*I(right-tail) |

-12.650 |

8.162 |

-1.550 |

0.1218 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.733 |

0.464 |

0.801 |

0.663 |

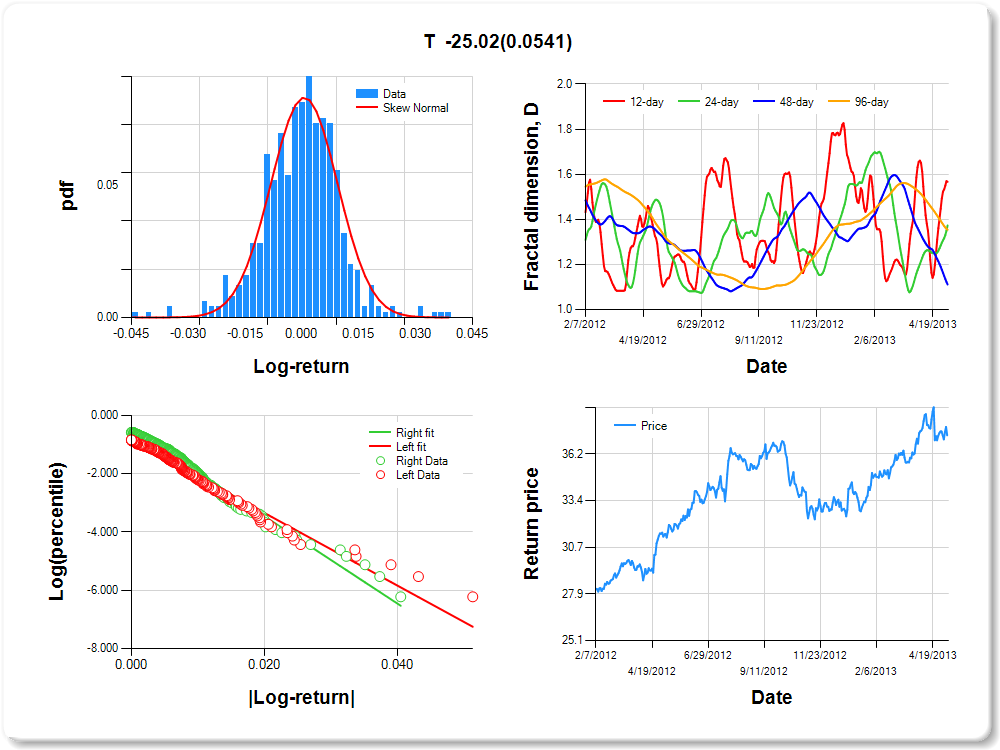

T

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

3.39 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Skew Normal |

0.382 |

0.353 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.826 |

0.099 |

-8.333 |

0.0000 |

|log-return| |

-124.652 |

8.969 |

-13.898 |

0.0000 |

I(right-tail) |

0.391 |

0.136 |

2.875 |

0.0042 |

|log-return|*I(right-tail) |

-25.024 |

12.963 |

-1.930 |

0.0541 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.433 |

0.627 |

0.889 |

0.646 |

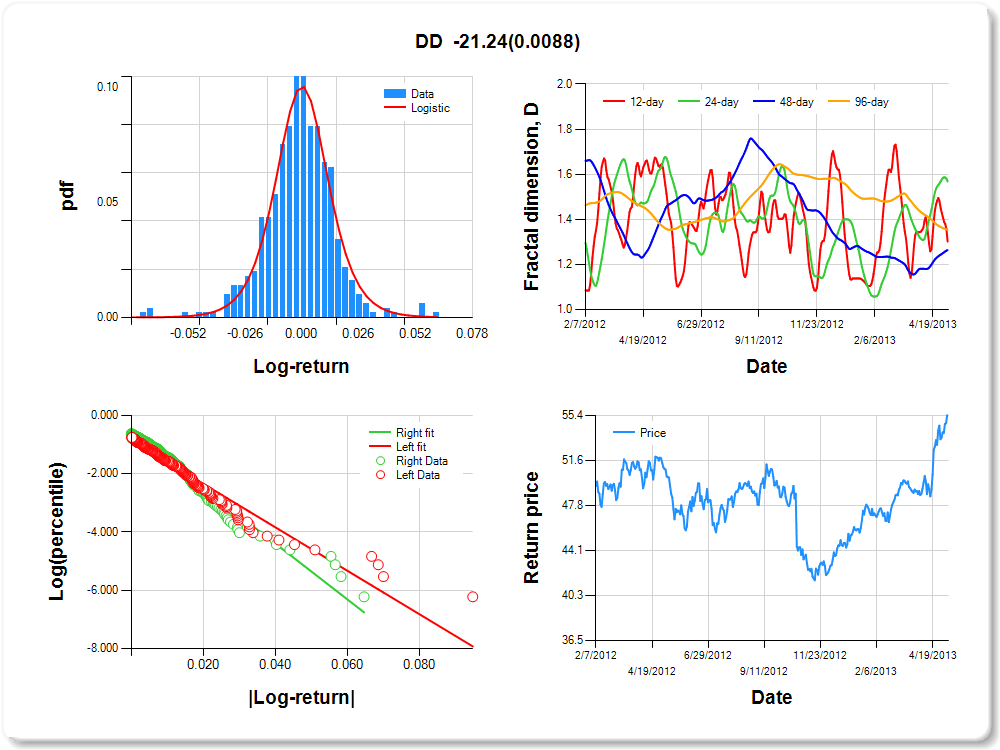

DD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.06 |

2.80 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.358 |

0.170 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.849 |

0.090 |

-9.410 |

0.0000 |

|log-return| |

-74.588 |

5.194 |

-14.360 |

0.0000 |

I(right-tail) |

0.295 |

0.129 |

2.287 |

0.0226 |

|log-return|*I(right-tail) |

-21.239 |

8.071 |

-2.632 |

0.0088 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.698 |

0.432 |

0.736 |

0.646 |

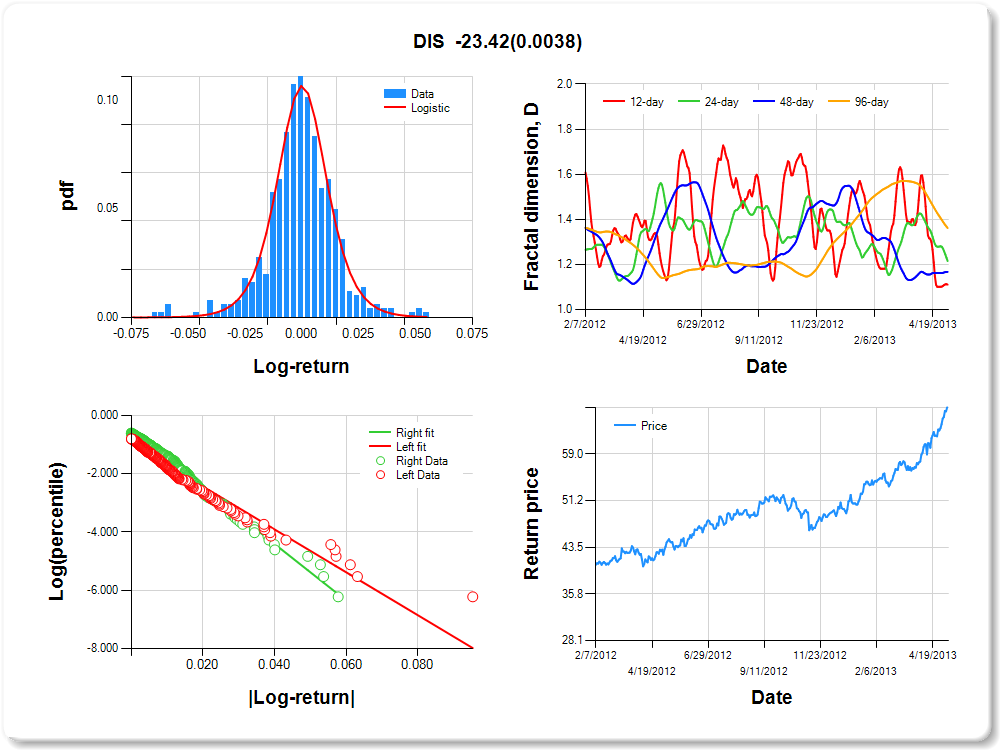

DIS

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.06 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.05 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.455 |

0.161 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.962 |

0.089 |

-10.777 |

0.0000 |

|log-return| |

-73.580 |

5.243 |

-14.034 |

0.0000 |

I(right-tail) |

0.441 |

0.127 |

3.458 |

0.0006 |

|log-return|*I(right-tail) |

-23.418 |

8.058 |

-2.906 |

0.0038 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.890 |

0.785 |

0.833 |

0.638 |

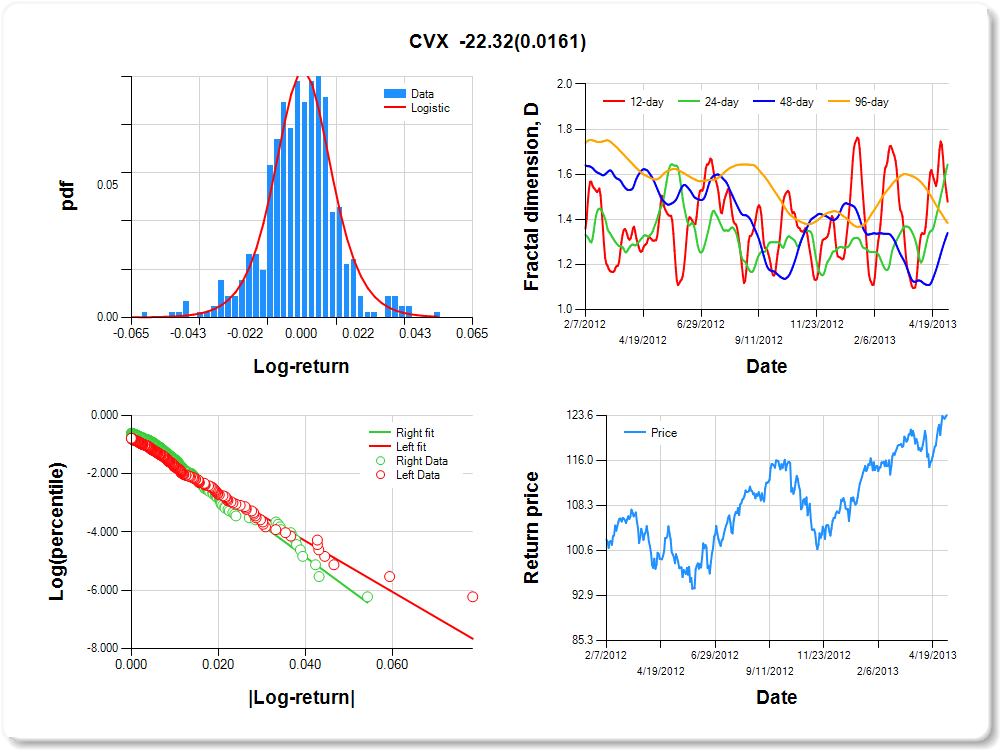

CVX

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.04 |

0.04 |

0.37 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.357 |

0.184 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.822 |

0.094 |

-8.753 |

0.0000 |

|log-return| |

-87.338 |

6.093 |

-14.334 |

0.0000 |

I(right-tail) |

0.343 |

0.133 |

2.588 |

0.0099 |

|log-return|*I(right-tail) |

-22.324 |

9.249 |

-2.414 |

0.0161 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.521 |

0.357 |

0.660 |

0.616 |

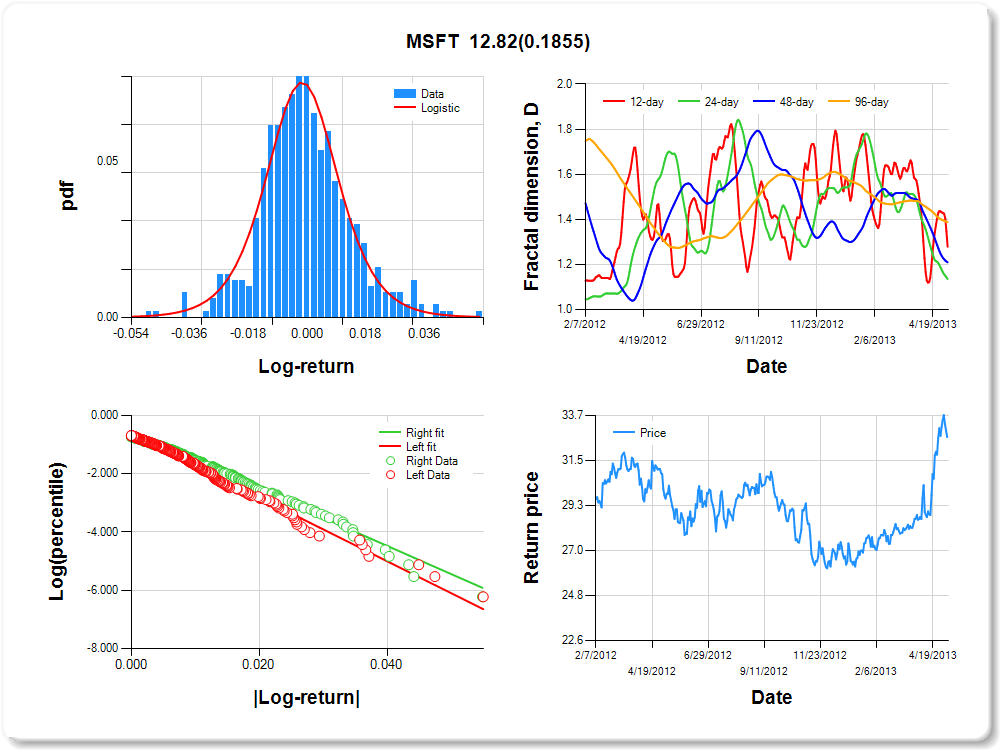

MSFT

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.04 |

2.80 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.014 |

0.228 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.599 |

0.095 |

-6.293 |

0.0000 |

|log-return| |

-109.336 |

7.211 |

-15.163 |

0.0000 |

I(right-tail) |

0.010 |

0.137 |

0.073 |

0.9420 |

|log-return|*I(right-tail) |

12.822 |

9.671 |

1.326 |

0.1855 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.721 |

0.864 |

0.790 |

0.612 |

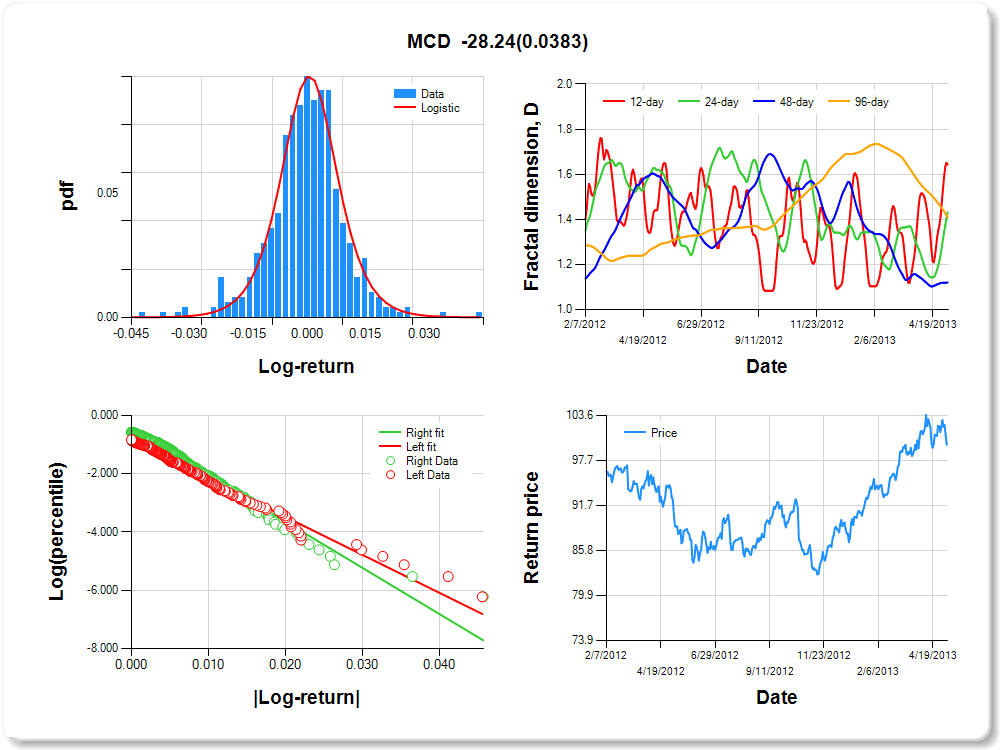

MCD

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.02 |

0.03 |

1.14 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.052 |

0.176 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.866 |

0.096 |

-8.983 |

0.0000 |

|log-return| |

-130.493 |

9.321 |

-14.000 |

0.0000 |

I(right-tail) |

0.404 |

0.133 |

3.046 |

0.0024 |

|log-return|*I(right-tail) |

-28.244 |

13.596 |

-2.077 |

0.0383 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.357 |

0.569 |

0.880 |

0.589 |

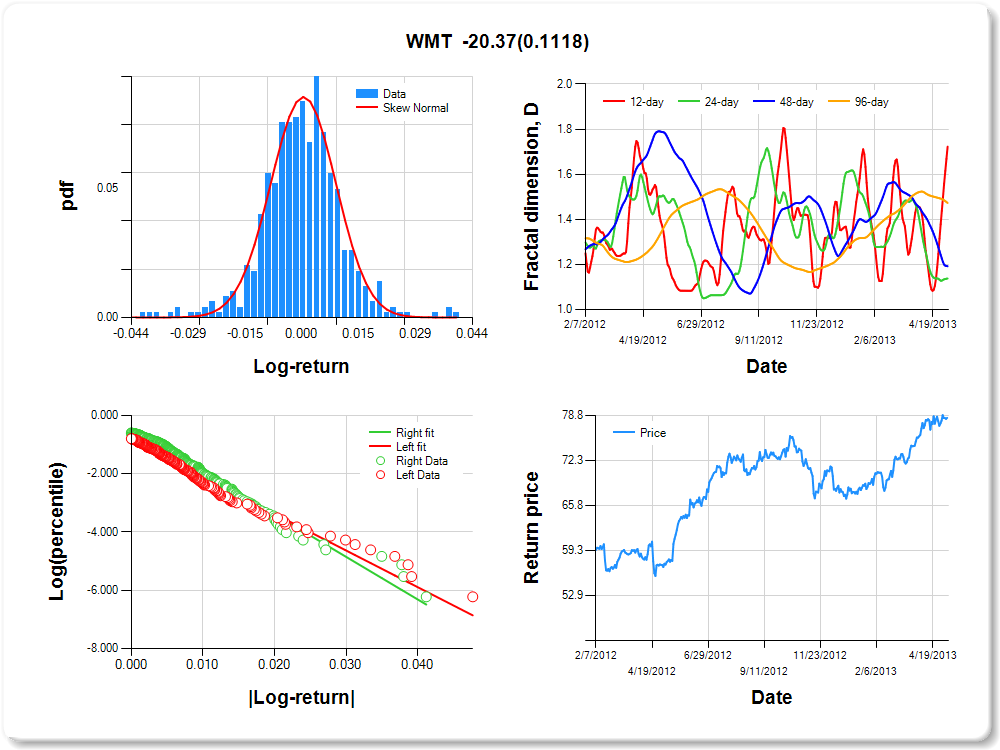

WMT

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.01 |

-0.01 |

0.00 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

2.24 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Skew Normal |

0.299 |

0.347 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.851 |

0.094 |

-9.072 |

0.0000 |

|log-return| |

-125.726 |

8.856 |

-14.197 |

0.0000 |

I(right-tail) |

0.396 |

0.133 |

2.985 |

0.0030 |

|log-return|*I(right-tail) |

-20.374 |

12.790 |

-1.593 |

0.1118 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.277 |

0.862 |

0.808 |

0.527 |

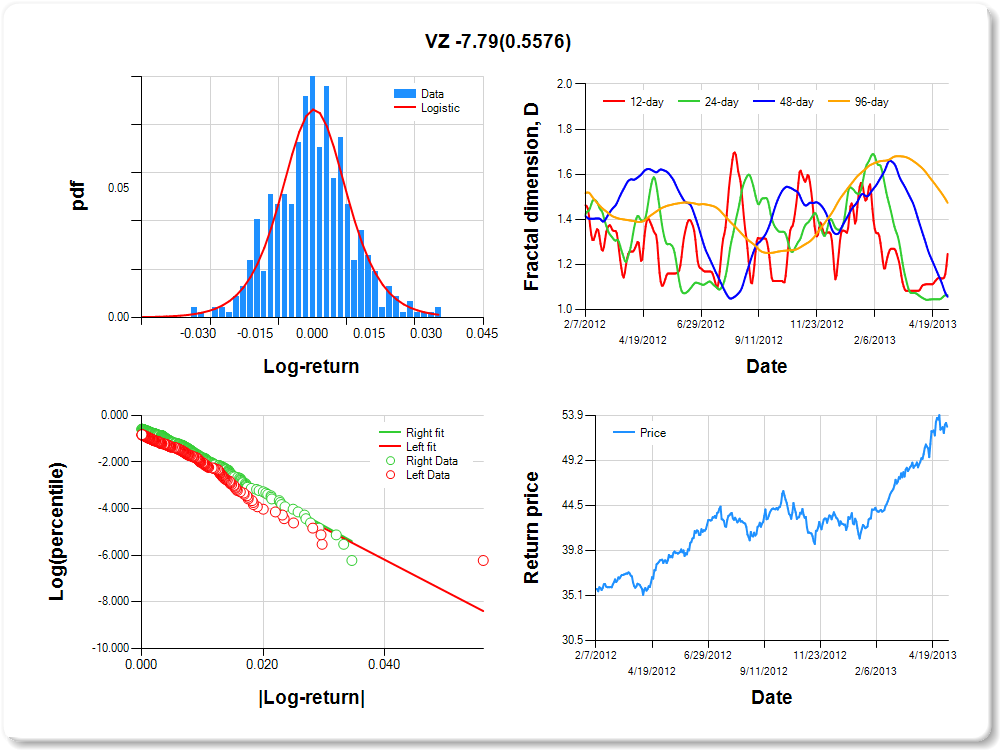

VZ

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.02 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

5.26 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.456 |

0.214 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.744 |

0.103 |

-7.227 |

0.0000 |

|log-return| |

-135.422 |

9.812 |

-13.802 |

0.0000 |

I(right-tail) |

0.335 |

0.140 |

2.393 |

0.0171 |

|log-return|*I(right-tail) |

-7.795 |

13.283 |

-0.587 |

0.5576 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.753 |

0.936 |

0.943 |

0.527 |

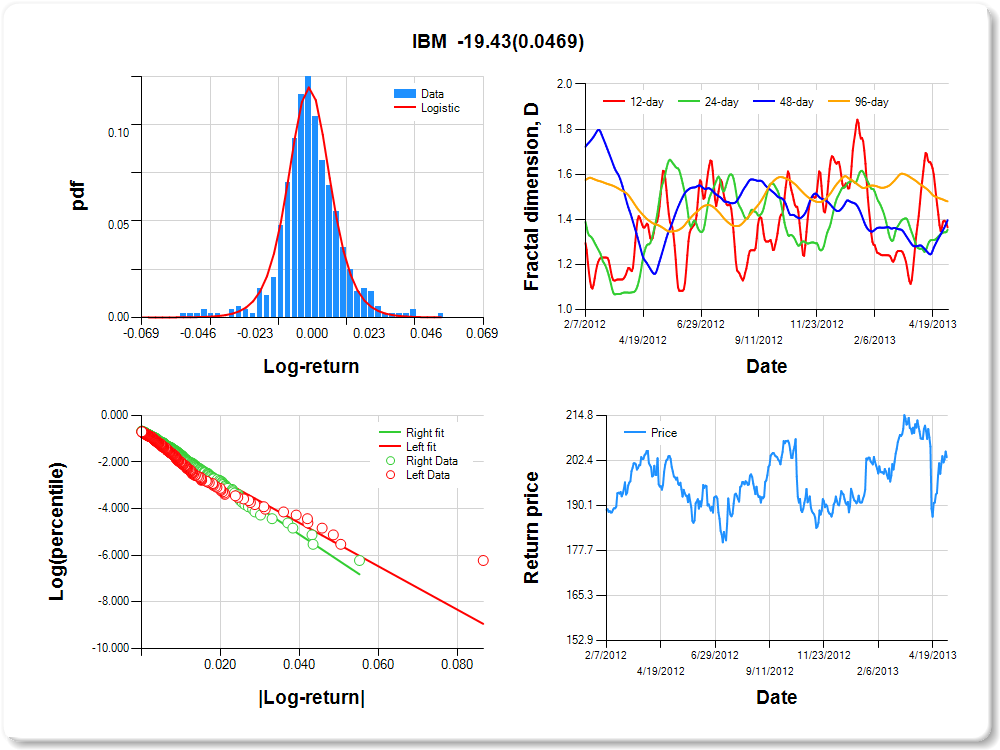

IBM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

2.17 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.380 |

0.138 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.904 |

0.084 |

-10.815 |

0.0000 |

|log-return| |

-93.032 |

6.414 |

-14.505 |

0.0000 |

I(right-tail) |

0.281 |

0.125 |

2.252 |

0.0248 |

|log-return|*I(right-tail) |

-19.426 |

9.751 |

-1.992 |

0.0469 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.636 |

0.646 |

0.604 |

0.520 |

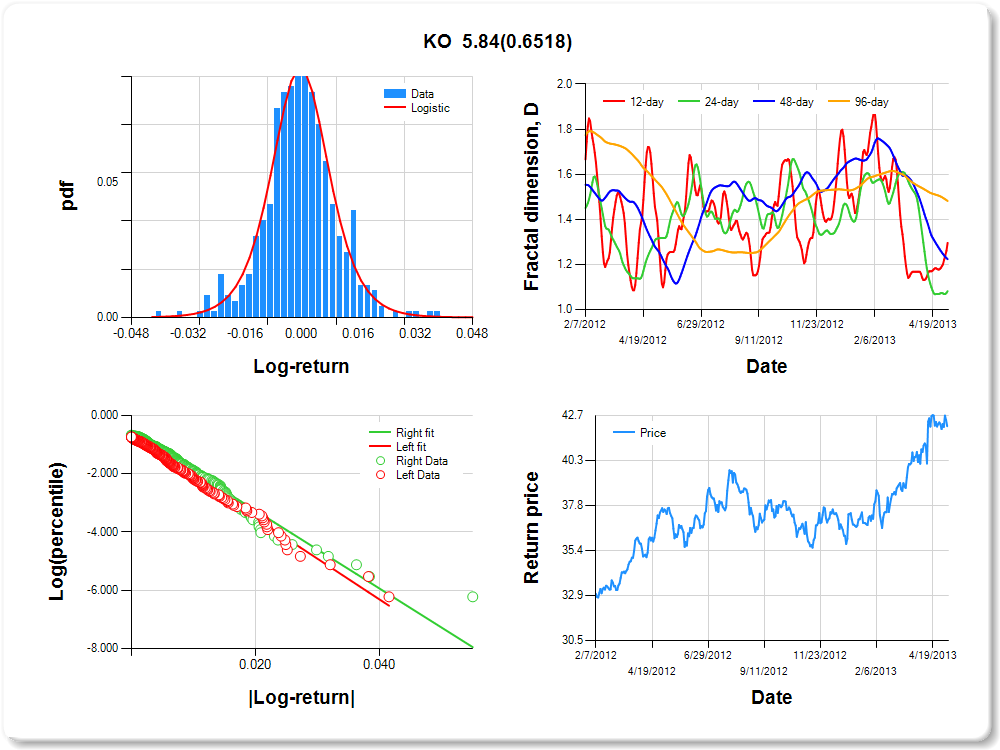

KO

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.03 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.03 |

2.29 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

-0.222 |

0.186 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.699 |

0.095 |

-7.350 |

0.0000 |

|log-return| |

-139.513 |

9.430 |

-14.794 |

0.0000 |

I(right-tail) |

0.139 |

0.135 |

1.023 |

0.3070 |

|log-return|*I(right-tail) |

5.838 |

12.931 |

0.451 |

0.6518 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.704 |

0.918 |

0.776 |

0.519 |

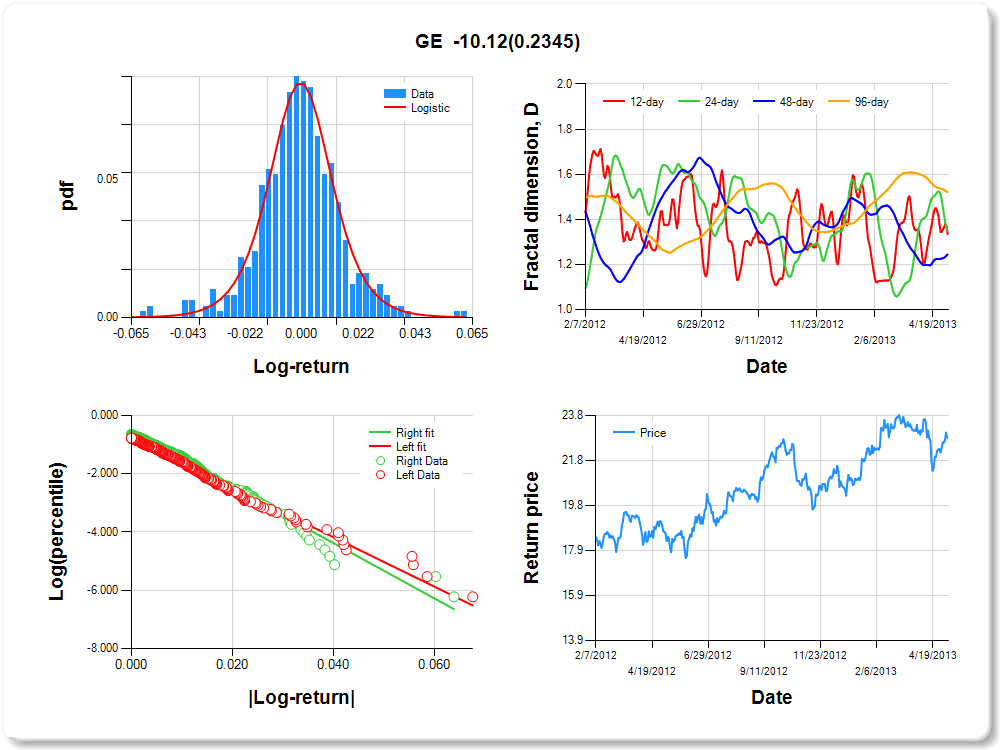

GE

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.05 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.04 |

0.04 |

2.52 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.068 |

0.202 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.755 |

0.096 |

-7.864 |

0.0000 |

|log-return| |

-84.901 |

5.865 |

-14.475 |

0.0000 |

I(right-tail) |

0.208 |

0.134 |

1.545 |

0.1229 |

|log-return|*I(right-tail) |

-10.116 |

8.499 |

-1.190 |

0.2345 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.665 |

0.650 |

0.756 |

0.479 |

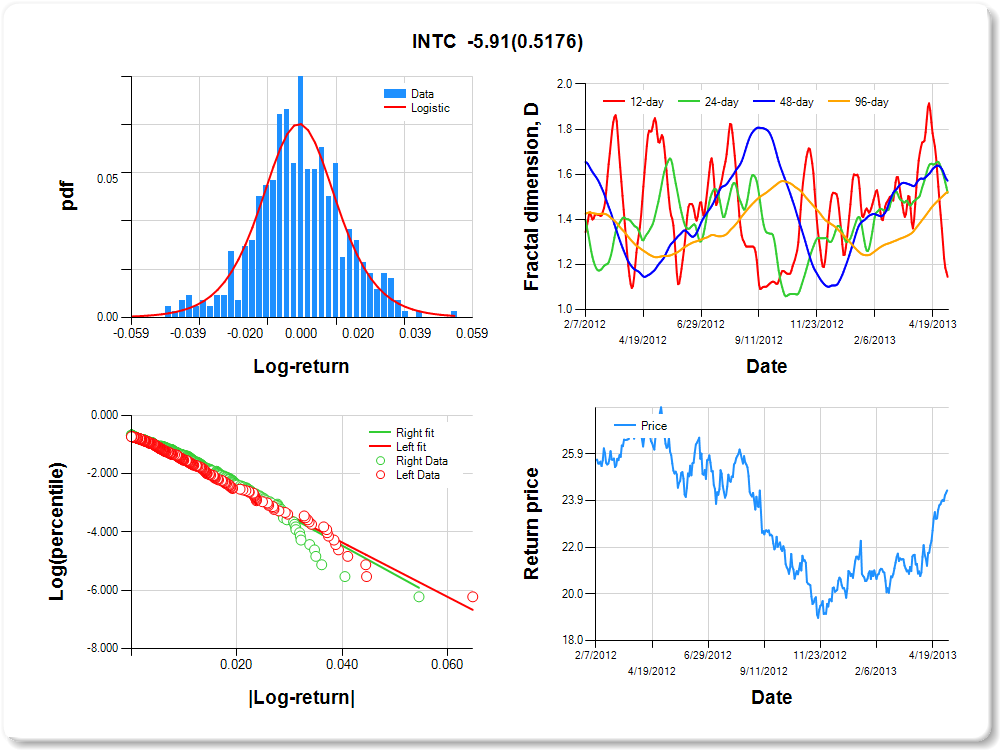

INTC

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.03 |

0.04 |

1.97 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.149 |

0.246 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.595 |

0.099 |

-5.986 |

0.0000 |

|log-return| |

-93.467 |

6.295 |

-14.847 |

0.0000 |

I(right-tail) |

0.131 |

0.142 |

0.923 |

0.3562 |

|log-return|*I(right-tail) |

-5.907 |

9.124 |

-0.647 |

0.5176 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.855 |

0.482 |

0.428 |

0.478 |

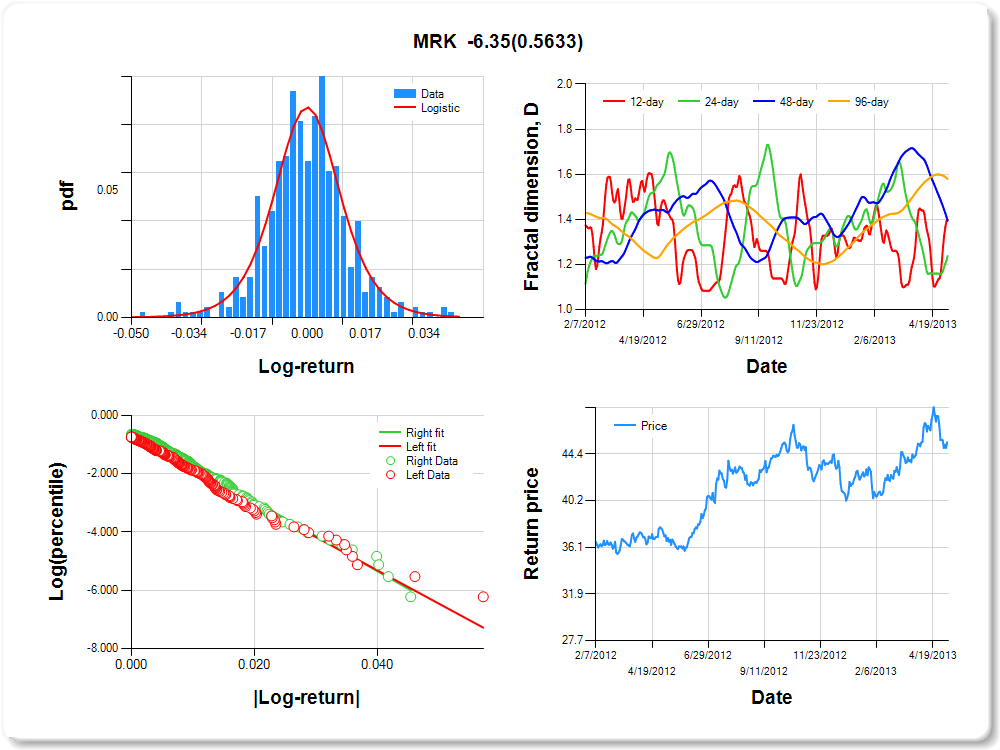

MRK

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.03 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

1.95 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.230 |

0.207 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.733 |

0.094 |

-7.837 |

0.0000 |

|log-return| |

-114.249 |

7.761 |

-14.721 |

0.0000 |

I(right-tail) |

0.228 |

0.134 |

1.707 |

0.0884 |

|log-return|*I(right-tail) |

-6.349 |

10.978 |

-0.578 |

0.5633 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.601 |

0.762 |

0.606 |

0.421 |

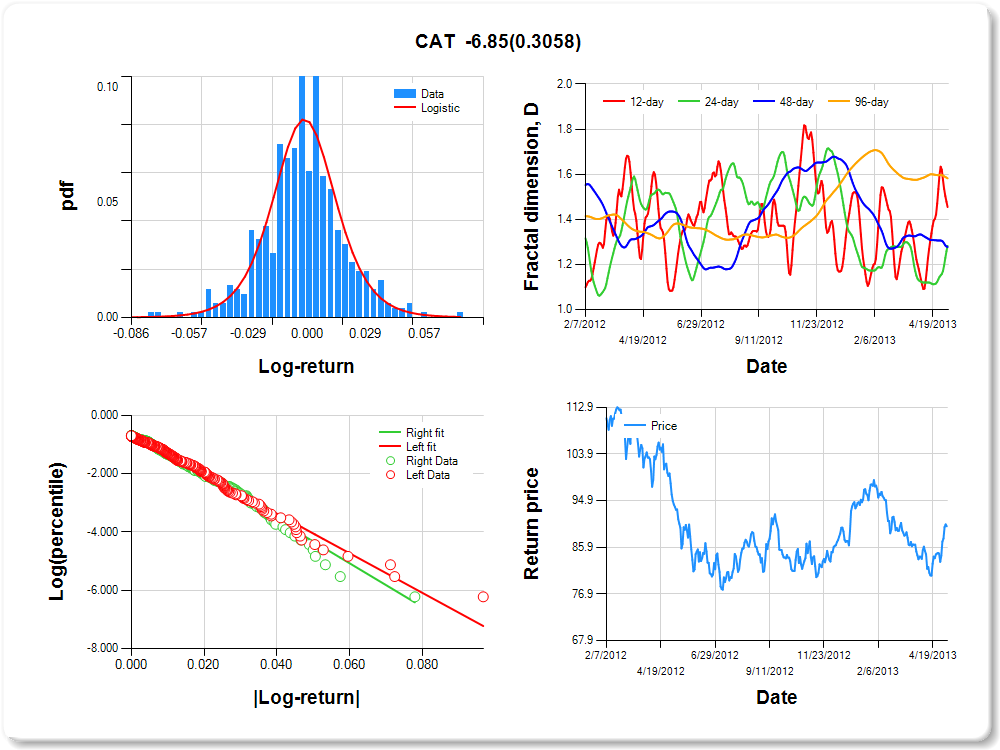

CAT

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.05 |

-0.03 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

1.78 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.191 |

0.199 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.655 |

0.093 |

-7.013 |

0.0000 |

|log-return| |

-67.961 |

4.507 |

-15.077 |

0.0000 |

I(right-tail) |

0.068 |

0.134 |

0.508 |

0.6119 |

|log-return|*I(right-tail) |

-6.845 |

6.678 |

-1.025 |

0.3058 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.545 |

0.718 |

0.722 |

0.418 |

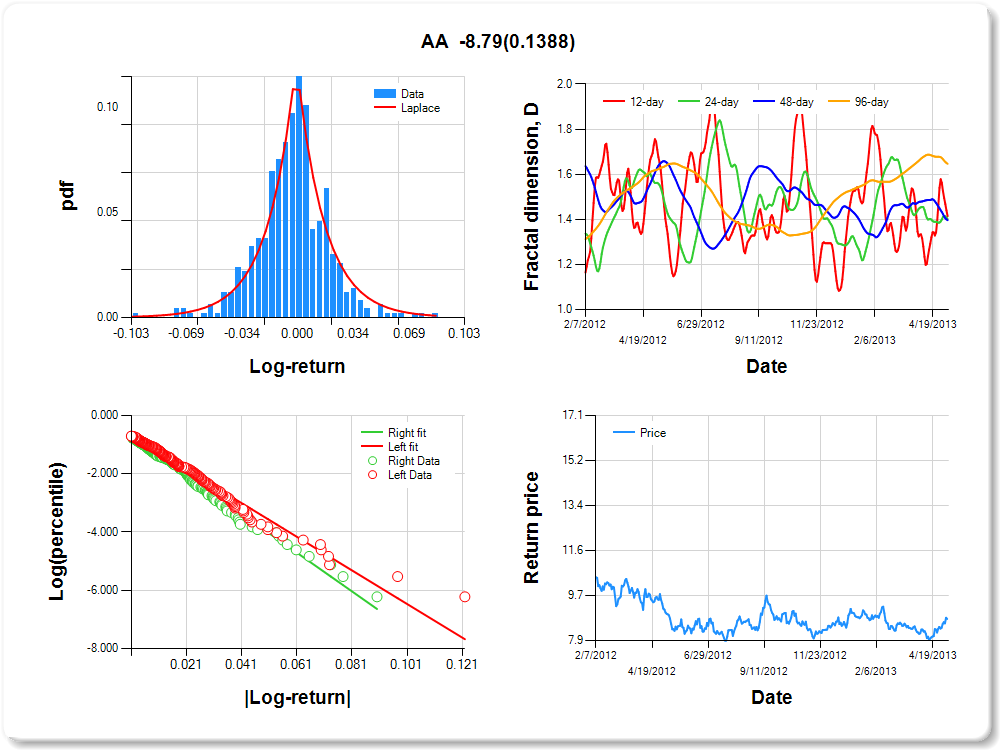

AA

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.07 |

-0.07 |

-0.04 |

-0.03 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.06 |

0.07 |

0.00 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Laplace |

0.274 |

0.281 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.676 |

0.094 |

-7.203 |

0.0000 |

|log-return| |

-57.670 |

3.870 |

-14.903 |

0.0000 |

I(right-tail) |

-0.012 |

0.134 |

-0.092 |

0.9265 |

|log-return|*I(right-tail) |

-8.788 |

5.927 |

-1.483 |

0.1388 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.586 |

0.598 |

0.603 |

0.354 |

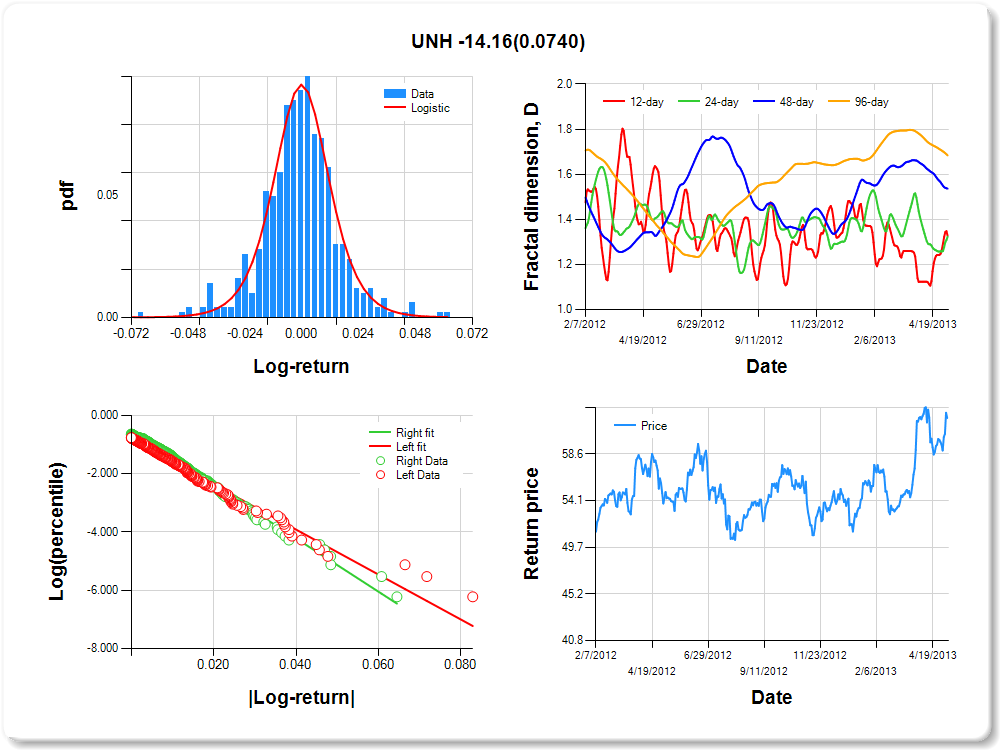

UNH

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.06 |

-0.04 |

-0.02 |

-0.02 |

-0.01 |

0.00 |

0.01 |

0.03 |

0.05 |

0.05 |

1.75 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.243 |

0.180 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.827 |

0.092 |

-9.025 |

0.0000 |

|log-return| |

-77.081 |

5.321 |

-14.486 |

0.0000 |

I(right-tail) |

0.265 |

0.130 |

2.037 |

0.0422 |

|log-return|*I(right-tail) |

-14.162 |

7.910 |

-1.791 |

0.0740 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.672 |

0.677 |

0.464 |

0.316 |

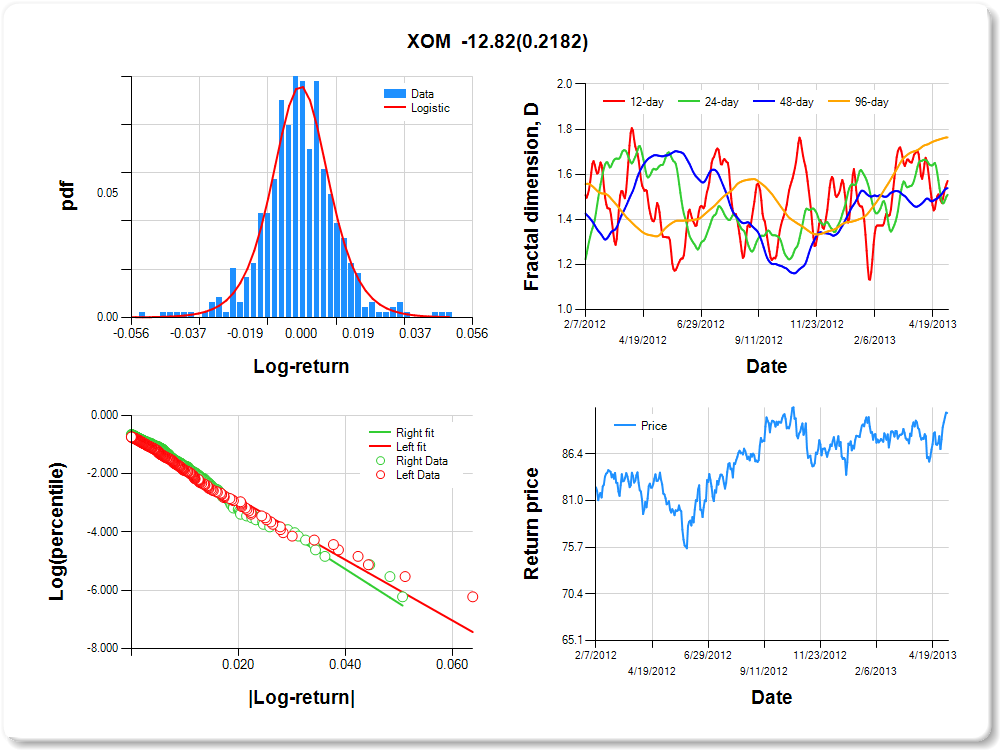

XOM

Percentile values of daily loss(gain) in per cent

| 0.5 | 1 | 5 | 10 | 25 | 50 | 75 | 90 | 95 | 99 | 99.5 |

| -0.04 |

-0.04 |

-0.02 |

-0.01 |

-0.01 |

0.00 |

0.01 |

0.02 |

0.03 |

0.04 |

3.87 |

Daily log-return distribution fitting results

| Distribution | Location, a | Scale, b |

| Logistic |

0.215 |

0.184 |

Linear regression results [Model: y=log(percentile of log-return), x=|log-return|]

| Variable | Coef(b) | s.e.(b) | t-value | P-value |

| Constant |

-0.781 |

0.091 |

-8.543 |

0.0000 |

|log-return| |

-104.207 |

7.093 |

-14.692 |

0.0000 |

I(right-tail) |

0.194 |

0.130 |

1.493 |

0.1361 |

|log-return|*I(right-tail) |

-12.816 |

10.394 |

-1.233 |

0.2182 |

Hurst exponent (of daily return price)

| 12-day | 24-day | 48-day | 96-day |

| 0.429 |

0.491 |

0.462 |

0.236 |